Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

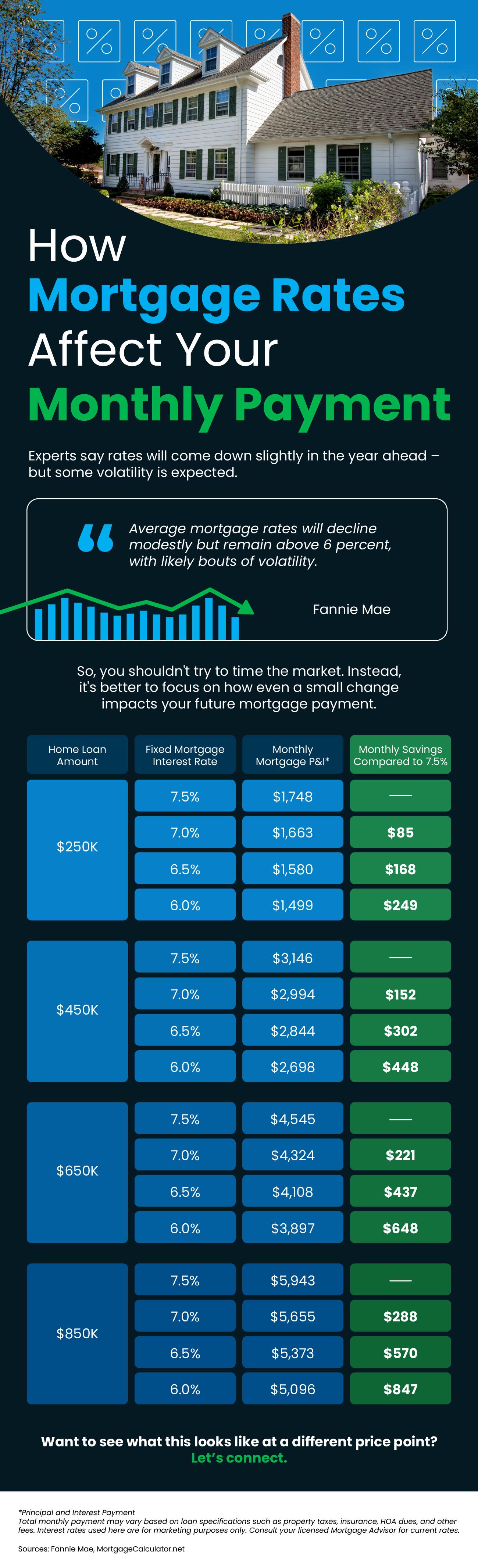

How Mortgage Rates Affect Your Monthly Payment

Some Highlights

- Experts say rates will come down slightly in the year ahead – but some volatility is expected. So, you shouldn’t try to time the market.

- Instead, it’s better to focus on how even a small change impacts your future mortgage payment. As rates come down, even a little bit, your monthly payment on your next home will too.

- Want to see what this looks like at a different price point? Let’s connect.

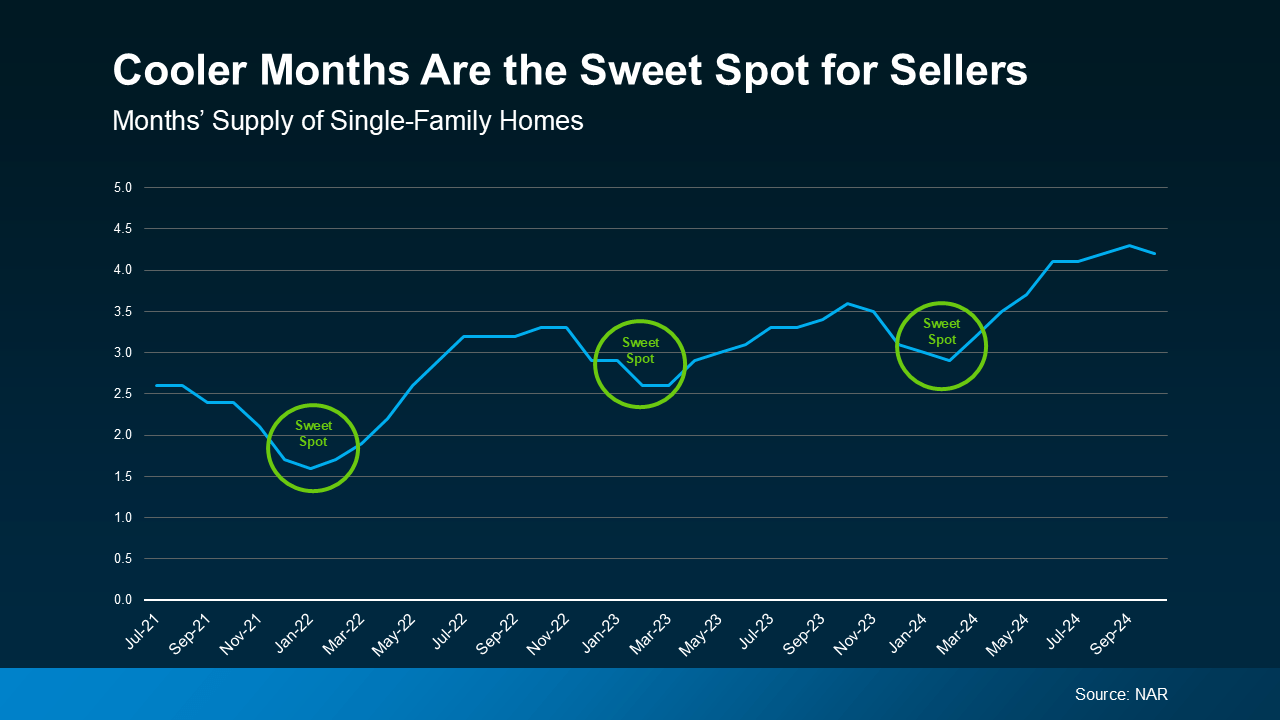

Sell Your House During the Winter Sweet Spot

A lot of people assume spring is the ideal time to sell a house. And sure, buyer demand usually picks up at that time of year. But here’s the catch: so does your competition because a lot of people put their homes on the market at the same time.

So, what’s the real advantage of selling your house before spring? It’ll stand out.

Historically, the number of homes for sale tends to drop during the cooler months – and that means buyers have fewer options to choose from.

You can see how that trend played out over the past few years in this data from the National Association of Realtors (NAR). Each time, the supply of homes for sale dipped during these cooler months. And then, after each winter lull, inventory started to climb as more sellers jumped into the market closer to spring (see graph below):

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Why wait until spring when you can get ahead of the curve now?

Fewer Listings Also Means More Eyes on Your Home

Another big perk of selling in the winter? The buyers who are looking right now are serious about making a move.

During this season, the window-shopper crowd tends to stay busy with other things, like holiday celebrations, and avoids looking for homes when the weather’s cooler. So, the buyers out looking aren’t casually browsing—they’re motivated, whether it’s because of a job relocation, a lease ending, or some other time-sensitive reason. And those are the types of buyers you want to work with. Investopedia explains:

“. . . if your house is up for sale in the winter and someone is looking at it, chances are that person is serious and ready to buy.”

Bottom Line

With less competition and serious buyers on the hunt, you’ll be in a great position to sell your house this winter. Let’s connect if you’re ready to get the process started.

What’s Behind Today’s Mortgage Rate Volatility?

If you’ve been keeping an eye on mortgage rates lately, you might feel like you’re on a roller coaster ride. One day rates are up; the next they dip down a bit. So, what’s driving this constant change? Let’s dive into just a few of the major reasons why we’re seeing so much volatility, and what it means for you.

The Market’s Reaction to the Election

A significant factor causing fluctuations in mortgage rates is the general reaction to the political landscape. Election seasons often bring uncertainty to financial markets, and this one is no different. Markets tend to respond not only to who won, but also to the economic policies they are expected to implement. And when it comes to what’s been happening with mortgage rates over the past couple of weeks, as the National Association of Home Builders (NAHB) says:

“. . . the primary reason interest rates have been on the rise pertains to the uncertainty surrounding the presidential election. Although the election is now complete, there continue to be growing concerns over budget deficits.”

In the short term, this anticipation has caused a slight uptick in mortgage rates as the markets adjust and react. Additionally, factors like international tensions, supply chain disruptions, and trade policies can drive investor sentiment, causing them to seek safer assets like bonds, which can indirectly impact mortgage rates. Essentially, the more global or domestic uncertainty, the greater the chance that mortgage rates may shift.

The Economy and the Federal Reserve

Inflation and unemployment are two other big drivers of mortgage rates. The Federal Reserve (the Fed) has been working to bring inflation under control, and has been closely monitoring the economy as they do. And as long as inflation continues to moderate and the job market shows signs of maximum employment, the Fed will continue its plans to cut the Federal Funds Rate.

Although the Fed doesn’t set mortgage rates, their decisions do have an impact, and typically a cut leads to a mortgage rates response. And in their November 6-7th meeting, the Fed had the data they needed to make another cut to the Federal Funds Rate. And while that decision was expected and much of the mortgage rate movement happened prior to that meeting, there was a slight dip in rates.

What To Expect in the Coming Months

As we look ahead, mortgage rates will respond to changes in the Fed’s policies and other economic indicators. The markets will likely remain in a wait-and-see mode, reacting to each new development. And, with the transition of a new administration comes an element of unpredictability. A recent article from The Mortgage Reports explains:

“Today’s economic indicators come with mixed pressures on mortgage rates and we’re likely to be in for a good amount of volatility as markets adjust and respond to the election . . .”

The best way to navigate this landscape is to have a team of real estate experts by your side. Professionals will help you understand what’s happening and can provide you with the guidance you need to make informed housing market decisions along the way.

Bottom Line

The takeaway? Today’s mortgage rate volatility is going to continue to be driven by economic factors and political changes.

Now is the time to lean on experienced professionals. A trusted real estate agent and mortgage lender can help you navigate through it. And with the right guidance, you can make informed decisions.

What To Look For From This Week’s Fed Meeting

You may be hearing a lot of talk about the Federal Reserve (the Fed) and how their actions will impact the housing market right now. Here’s why.

The Fed meets again this week to decide the next step with the Federal Funds Rate. That’s how much it costs banks to borrow from each other. Now, that’s not the same thing as setting mortgage rates, but mortgage rates can be influenced through this process. And if you’re thinking about buying or selling a home, you may be wondering about the downstream impact and when mortgage rates will come down.

Here’s a quick rundown of what you need to know to help you anticipate what’ll happen next. The Fed’s decisions are guided by these three key economic indicators:

- The Direction of Inflation

- How Many Jobs the Economy Is Adding

- The Unemployment Rate

Let’s take a look at each one.

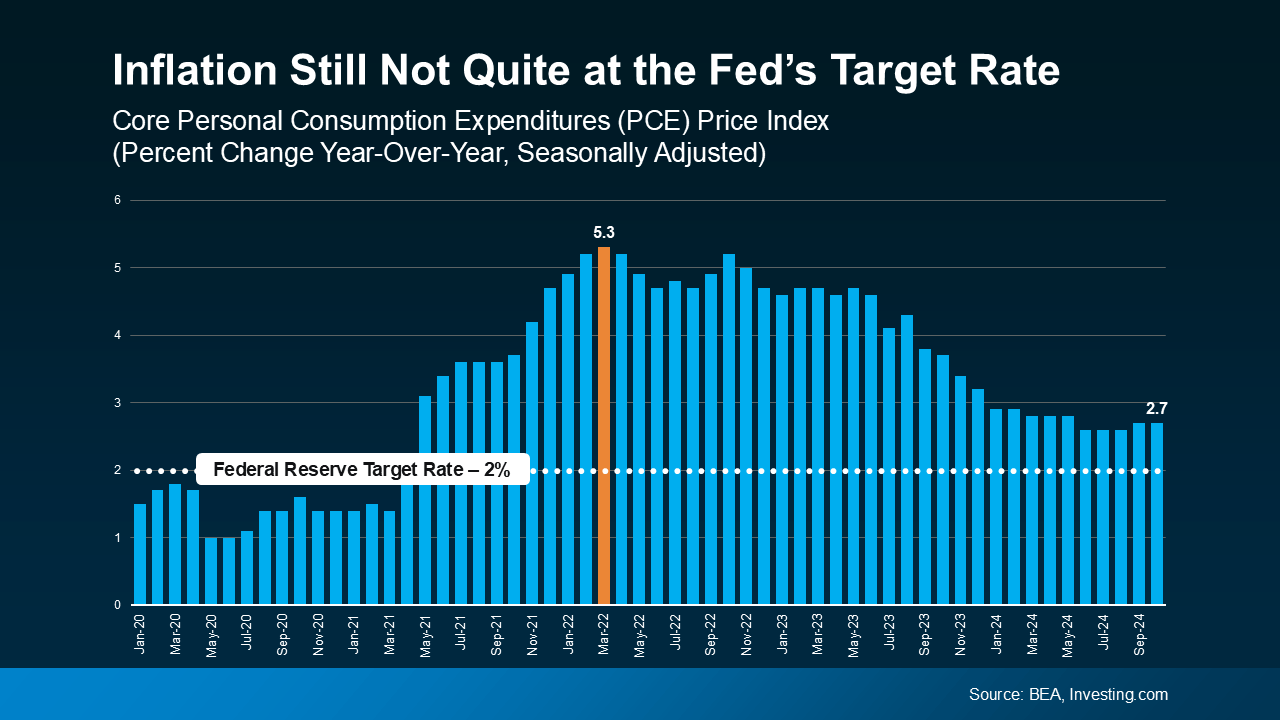

1. The Direction of Inflation

You’ve likely noticed prices for everyday goods and services seem to be higher each time you make a purchase at the store. That’s because of inflation – and the Fed wants to see that number come back down so it’s closer to their 2% target.

Right now, it’s still higher than that. But despite a little volatility, inflation has generally been moving in the right direction. It gradually came down over the past two years, and is holding fairly steady right now (see graph below):

The path of inflation – though still not at their target rate – is a big part of the reason why the Fed will likely lower the Fed Funds Rate again this week to make borrowing less expensive, while still ensuring the economy continues to grow.

The path of inflation – though still not at their target rate – is a big part of the reason why the Fed will likely lower the Fed Funds Rate again this week to make borrowing less expensive, while still ensuring the economy continues to grow.

2. How Many Jobs the Economy Is Adding

The Fed is also keeping an eye on how many new jobs are added to the economy each month. They want job growth to slow down a bit before they cut the Federal Funds Rate further. When fewer jobs are created, it shows the economy is still doing well, but gradually cooling off—exactly what they’re aiming for. And that’s what’s happening right now. Reuters says:

“Any doubts the Federal Reserve will go ahead with an interest-rate cut . . . fell away on Friday after a government report showed U.S. employers added fewer workers in October than in any month since December 2020.”

Employers are still hiring, but just not as many positions right now. This shows the job market is starting to slow down after running hot for a while, which is what the Fed wants to see.

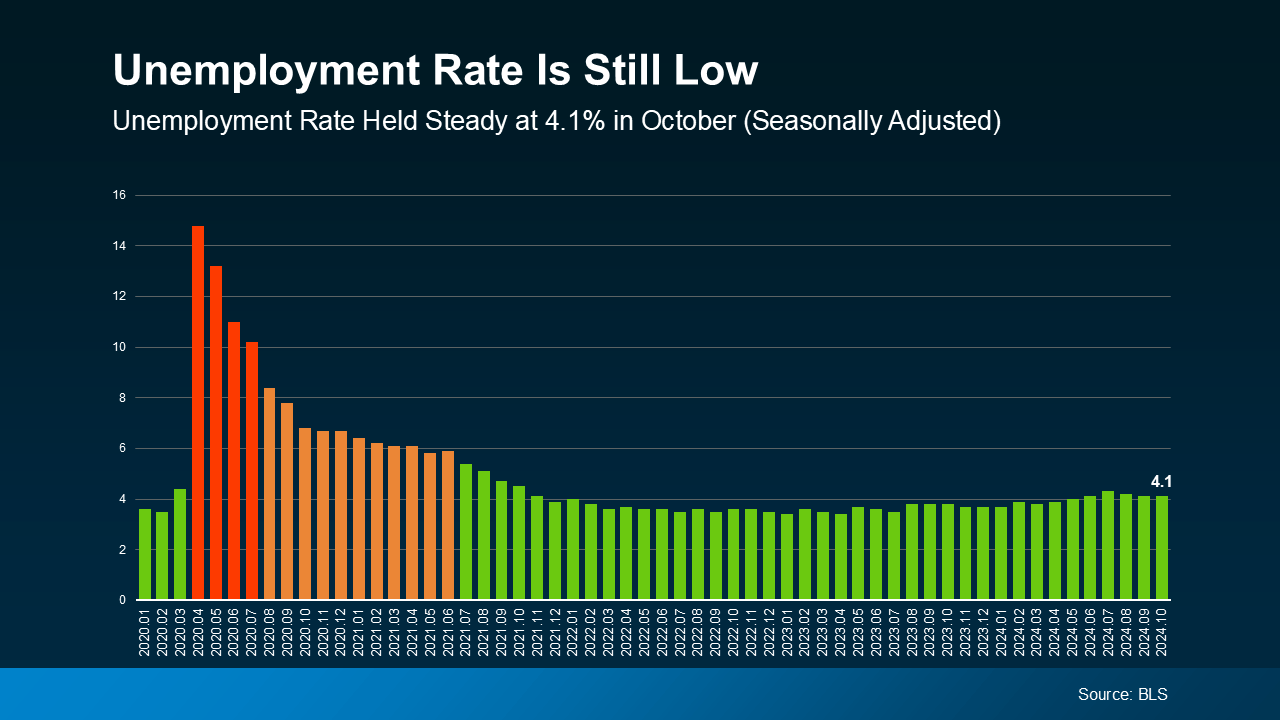

3. The Unemployment Rate

The unemployment rate shows the percentage of people who want jobs but can’t find them. A low unemployment rate means most people are working, which is great. However, it can push inflation higher because more people working means more spending—and that makes prices go up.

Many economists consider any unemployment rate below 5% to be as close to full employment as is realistically possible. In the most recent report, unemployment is sitting at 4.1% (see graph below):

Unemployment this low shows the labor market is still strong even as fewer jobs were added to the economy. That’s the balance the Fed is looking for.

Unemployment this low shows the labor market is still strong even as fewer jobs were added to the economy. That’s the balance the Fed is looking for.

What Does This Mean Going Forward?

Overall, the economy is headed in the direction the Fed wants to see – and that’s why experts say they will likely cut the Federal Funds Rate by a quarter of a percentage point this week, according to the CME FedWatch Tool.

If that expectation ends up being correct, that could pave the way for mortgage rates to come down too. But that doesn’t mean they’ll fall immediately. It will take some time. Remember, the Fed doesn’t determine mortgage rates. Forecasts show mortgage rates will ease more gradually over the course of the next year as long as these economic indicators continue to move in the right direction and the Fed can continue their Federal Funds rate cuts through 2025.

But a change in any one of the factors mentioned here could cause a shift in the market and in the Fed’s actions in the days and months ahead. So, brace for some volatility, and for mortgage rates to respond along the way. As Ralph McLaughlin, Senior Economist at Realtor.com, notes:

“The trajectory of rates over the coming months will be largely dependent on three key factors: (1) the performance of the labor market, (2) the outcome of the presidential election, and (3) any possible reemergence of inflationary pressure. While volatility has been the theme of mortgage rates over the past several months, we expect stability to reemerge towards the end of November and into early December.”

Bottom Line

While the Fed’s actions play a part, economic data and market conditions are what really drive mortgage rates. As we move through the rest of 2024 and 2025, expect rates to stabilize or decline gradually, offering more certainty in what has been a volatile market.

Expect the Unexpected: Anticipating Volatility in Today’s Housing Market

You’ve probably noticed one thing if you’re thinking about making a move: the housing market feels a bit unpredictable right now. The truth is, from home prices to mortgage rates, we’re seeing more volatility – and it’s important to understand why.

At a high-level, let’s break down what’s happening and the best way to navigate it.

What’s Driving Today’s Market Volatility?

Factors like economic data, unemployment numbers, decisions coming out of the Federal Reserve (The Fed), and even the presidential election, are creating uncertainty right now – and uncertainty leads to market volatility.

You can see that when you look at what’s happening with mortgage rates. New economic reports and other geopolitical events have an impact and can cause sudden shifts up or down, even though experts still forecast rates will come down overall. We’ve seen that effect play out recently, like when employment and inflation data get released each month.

And as the markets react, these types of updates will continue to have an impact on rates moving forward. As Greg McBride, CFA, Chief Financial Analyst at Bankrate, says:

“After steadily declining throughout the summer months, I expect more ups and downs to mortgage rates . . . Job market data will be closely watched as well as any clues from the Fed about the extent of upcoming interest rate cuts.”

This is exactly why the projected decline in mortgage rates isn’t going to be a straight line down over the next year. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, explains:

“Rates have shown considerable volatility lately, and may continue to do so . . . Overall, we still expect a downward long-term mortgage rate trend.”

Plus, home prices and the number of homes on the market vary dramatically depending on where you’re looking to buy or sell, which makes it even harder to get a clear picture. In some areas, home prices are rising and inventory is tight, while in others, there are more homes available and it’s leading to more moderate pricing shifts.

As all of this unfolds, understanding what’s happening will help you make the right decisions, whether that’s buying or selling. And there’s one easy way to get that information: from a professional.

The Importance of Partnering with a Pro

While the road ahead may have some bumps and unexpected turns, you don’t have to go it alone. A great agent will keep you up to date on the latest market developments, guide you through any shifts, and help you make smart decisions based on your goals.

For example, as mortgage rates change, professionals (like your agent and a trusted lender) will explain how the shifts impact what you can reasonably plan for in your monthly payment. This will help you see how even a small change in rates can impact your bottom line – that way you don’t lose sight of the big picture even as shifts happen here and there.

And since conditions can vary significantly from one neighborhood to another, your agent will also help you understand the specifics of your market—whether it’s how to navigate competition with other buyers, the number of homes available, or what’s happening with local home prices. Their insights and expertise will help you adapt to any movement in the market.

Bottom Line

The housing market may be experiencing some shifts, but don’t let it stop you from making your move. With the support of an experienced real estate agent and a trusted lender, you’ll be ready to navigate the changes and make the most of the opportunities that come your way.

Let’s turn any uncertainty into your advantage, helping you move forward with confidence.

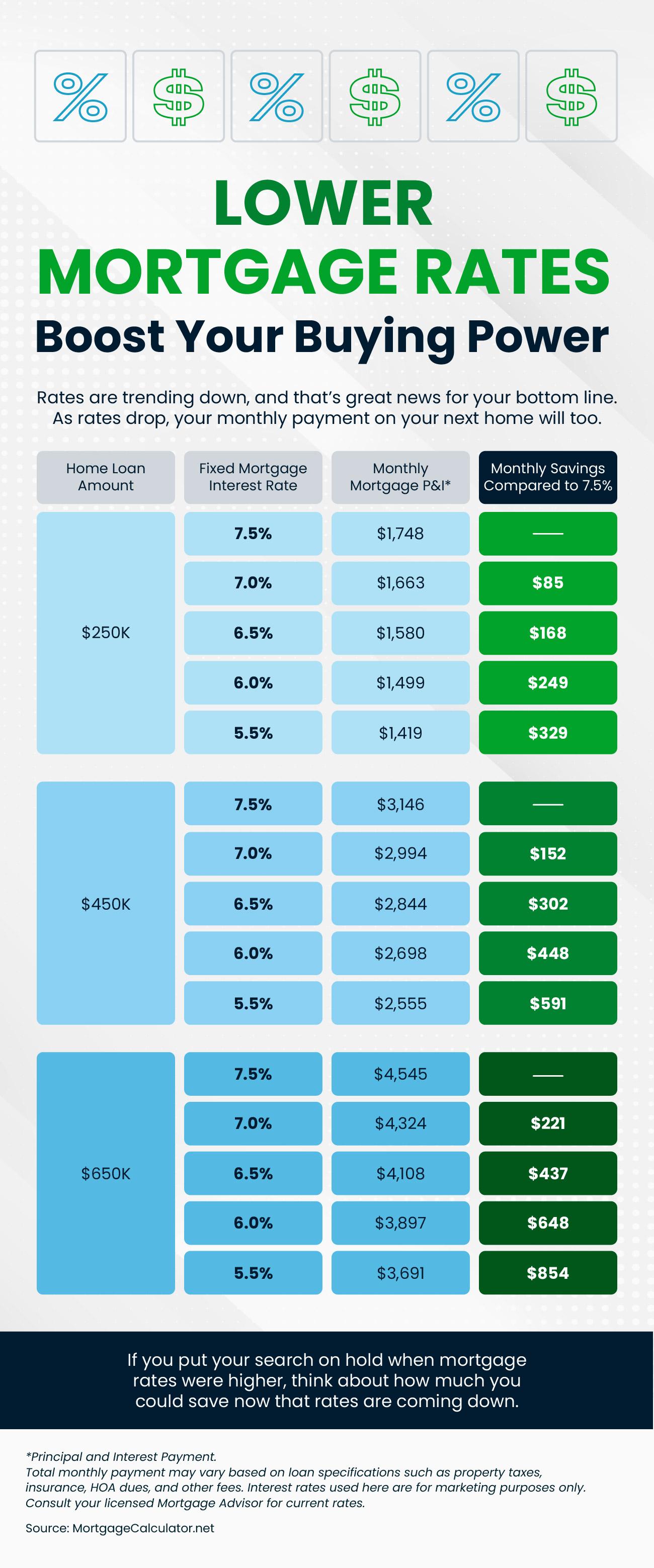

Lower Mortgage Rates Boost Your Buying Power

Some Highlights

- Mortgage rates are trending down and that’s great news for your bottom line.

- As rates drop, your monthly payment on your next home does too. Even a small change in mortgage rates can have a big impact on your purchasing power.

- If you put your search on hold when mortgage rates were higher, think about how much you could save now that rates are coming down.

Mortgage Rates Drop to Lowest Level in over a Year and a Half

Mortgage Rates Drop to Lowest Level in over a Year and a Half

Mortgage rates have hit their lowest point in over a year and a half. And that’s big news if you’ve been sitting on the homebuying sidelines waiting for this moment.

Even a small decline in rates could help you get a better monthly payment than you would expect on your next home. And the drop that’s happened recently isn’t small. As Sam Khater, Chief Economist at Freddie Mac, says:

“Mortgage rates have fallen more than half a percent . . . and are at their lowest level since February 2023.”

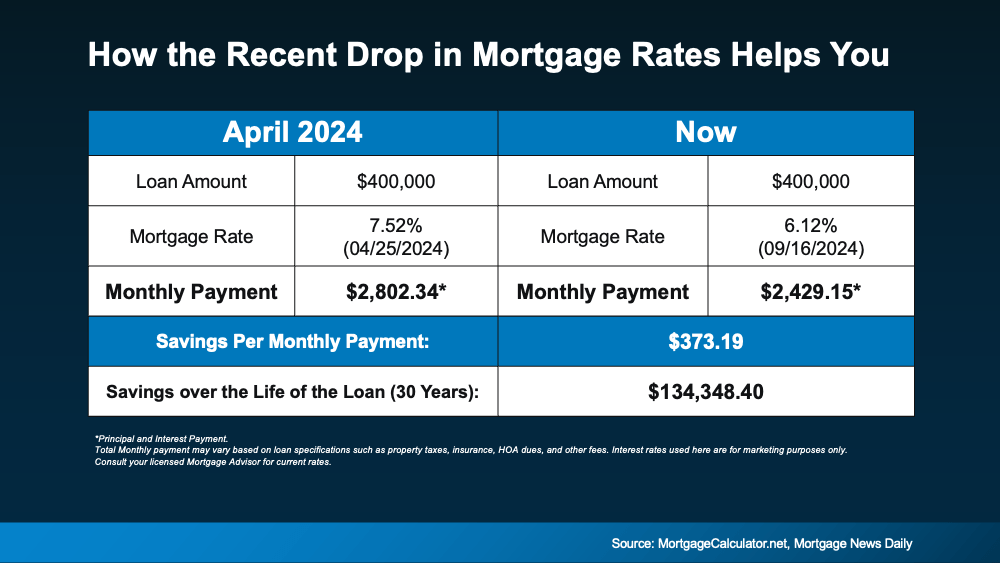

But if you want to see it to really believe it, here’s how the math shakes out. Take a closer look at the impact on your monthly payment.

The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a house back in April (this year’s mortgage rate high), versus what it could look like if you buy a home now (see below):

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

Bottom Line

With the recent drop in mortgage rates, the purchasing power you have right now is better than it’s been in almost two years. Let’s talk about your options and how you can make the most of this moment you’ve been waiting for.

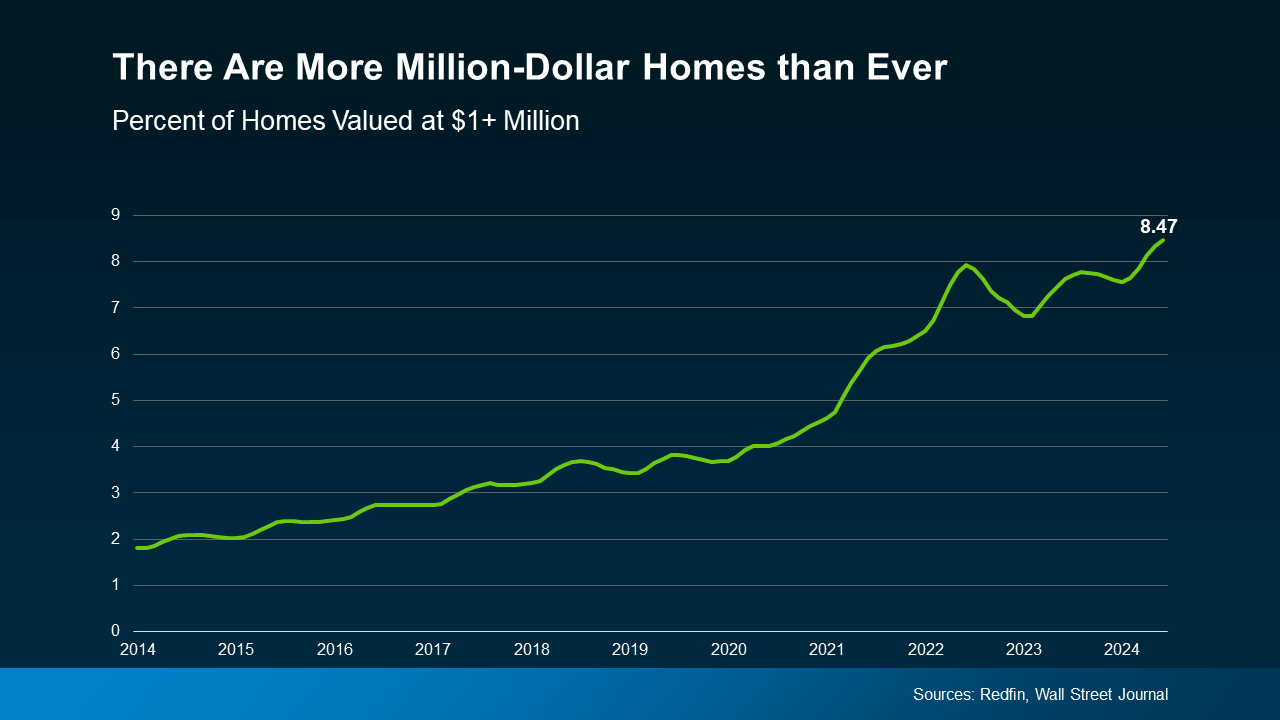

The Latest on the Luxury Home Market

Luxury living is about more than just stunning views and cutting-edge smart home technology—it’s about elevating your lifestyle. And if you’re in the market for a million-dollar home, now is an excellent time to explore the thriving luxury market. Here’s why.

The Number of Luxury Homes Is Growing

The top of the market, or luxury homes, can mean different things depending on where you live. But in general, these are homes that are in the top 5% price range in any area. According to a recent report from Redfin, the average value of those homes has risen to over one million dollars:

“The median sale price for U.S. luxury homes, defined as the top 5% of listings, rose 9% year-over-year to a record $1.18 million during the second quarter.”

That same report goes on to show the percentage of homes valued at a million dollars or more has risen to an all-time high (see graph below):

That means, if this is your desired price range, you have options to choose from, each with different features and styles.

That means, if this is your desired price range, you have options to choose from, each with different features and styles.

Whether you’re looking for the latest designs, like modern kitchens with high-end appliances, exclusive amenities, or enhanced privacy and security, the market that fits this lifestyle is growing.

Your Luxury Home Is an Investment

In addition, a luxury home could help you build significant long-term wealth. As the Redfin quote mentioned earlier says, luxury home prices are rising. That may be the reason there are a lot of people investing in luxury real estate right now. According to the August Luxury Market Report:

“By the end of July, the overall growth in the volume of sales in 2024 stood at 14.82% for single-family homes and 11.35% for attached homes compared to the same period in 2023.”

Bottom Line

With more million-dollar homes on the market and prices going up, you have luxury options to choose from and a chance to build significant long-term wealth. Want to see the best homes in our area? Let’s get in touch today.

How the Federal Reserve’s Next Move Could Impact the Housing Market

Now that it’s September, all eyes are on the Federal Reserve (the Fed). The overwhelming expectation is that they’ll cut the Federal Funds Rate at their upcoming meeting, driven primarily by recent signs that inflation is cooling, and the job market is slowing down. Mark Zandi, Chief Economist at Moody’s Analytics, said:

“They’re ready to cut, just as long as we don’t get an inflation surprise between now and September, which we won’t.”

But what does this mean for the housing market, and more importantly, for you as a potential homebuyer or seller?

Why a Federal Funds Rate Cut Matters

The Federal Funds Rate is one of the key factors that influences mortgage rates – things like the economy, geopolitical uncertainty, and more also have an impact.

When the Fed cuts the Federal Funds Rate, it signals what’s happening in the broader economy, and mortgage rates tend to respond. While a single rate cut might not lead to a dramatic drop in mortgage rates, it could contribute to the gradual decline that’s already happening.

As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), points out:

“Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.”

And any upcoming Federal Funds Rate cut likely won’t be a one-time event. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.”

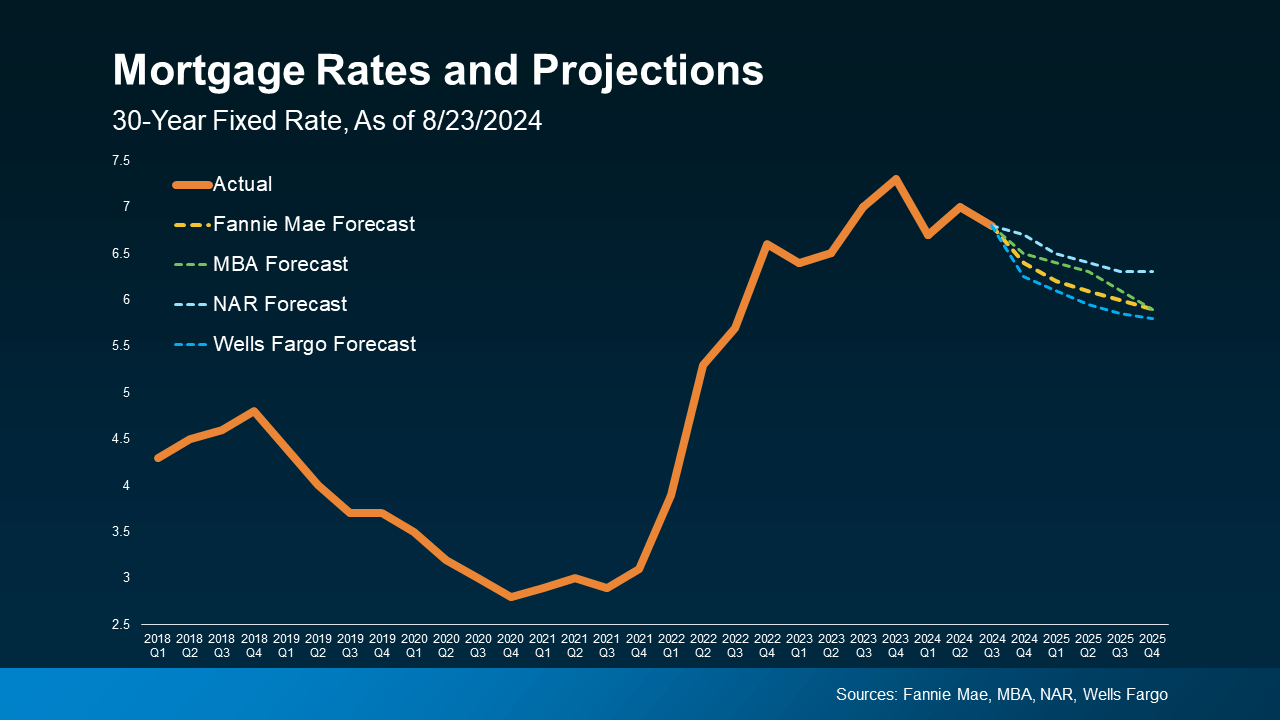

The Projected Impact on Mortgage Rates

Here’s what experts in the industry project for mortgage rates through 2025. One contributing factor to this ongoing gradual decline is the anticipated cuts from the Fed. The graph below shows the latest forecasts from Fannie Mae, MBA, NAR, and Wells Fargo (see graph below):

So, with recent improvements in inflation and signs of a cooling job market, a Federal Funds Rate cut is likely to lead to a moderate decline in mortgage rates (shown in the dotted lines). Here are two big reasons why that’s good news for both buyers and sellers:

So, with recent improvements in inflation and signs of a cooling job market, a Federal Funds Rate cut is likely to lead to a moderate decline in mortgage rates (shown in the dotted lines). Here are two big reasons why that’s good news for both buyers and sellers:

1. It Helps Alleviate the Lock-In Effect

For current homeowners, lower mortgage rates could help ease the lock-in effect. That’s where people feel stuck within their current home because today’s rates are higher than what they locked in when they bought their current house.

If the fear of losing your low-rate mortgage and facing higher costs has kept you out of the market, a slight reduction in rates could make selling a bit more attractive again. However, this isn’t expected to bring a flood of sellers to the market, as many homeowners may still be cautious about giving up their existing mortgage rate.

2. It Should Boost Buyer Activity

For potential homebuyers, any drop in mortgage rates will provide a more inviting housing market. Lower mortgage rates can reduce the overall cost of homeownership, making it more feasible for you if you’ve been waiting to make a move.

What Should You Do?

While a Federal Funds Rate cut is not expected to lead to drastically lower mortgage rates, it will likely contribute to the gradual decrease that’s already happening.

And while the anticipated rate cut represents a positive shift for the future of the housing market, it’s important to consider your options right now. Jacob Channel, Senior Economist at LendingTree, sums it up well:

“Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

Bottom Line

The expected Federal Funds Rate cut, driven by improving inflation and slower job growth, is likely to have a positive, though gradual, impact on mortgage rates. That could help unlock opportunities for you. When you’re ready, let’s connect. That way you’ll be prepared to take action when the time is right for you.

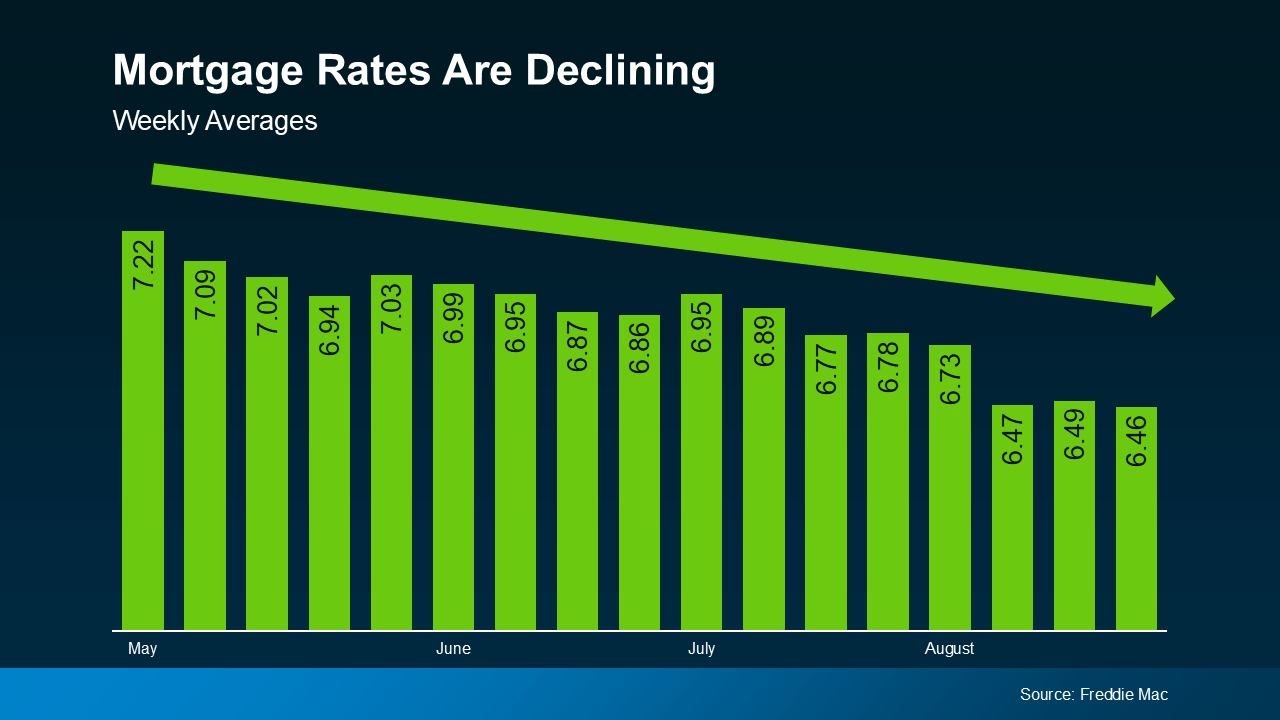

What Mortgage Rate Are You Waiting For?

You won’t find anyone who’s going to argue that mortgage rates have had a big impact on housing affordability over the past couple of years. But there is hope on the horizon. Rates have actually started to come down. And, recently they hit the lowest point we’ve seen in 2024, according to Freddie Mac (see graph below):

And if you’re thinking about buying a home, that may leave you wondering: how much lower are they going to go? Here’s some information that can help you know what to expect.

And if you’re thinking about buying a home, that may leave you wondering: how much lower are they going to go? Here’s some information that can help you know what to expect.

Expert Projections for Mortgage Rates

Experts say the overall downward trend should continue as long as inflation and the economy keeps cooling. But as new reports come out on those key indicators, there’s going to be some volatility here and there.

What you need to remember is it’s not wise to let those blips distract you from the larger trend. Rates are still down roughly a full percentage point from the recent peak compared to May.

And the general consensus is that rates in the low 6s are possible in the months ahead, it just depends on what happens with the economy and what the Federal Reserve decides to do moving forward.

Most experts are already starting to revise their 2024 mortgage rate forecasts to be more optimistic that lower rates are ahead. For example, Realtor.com says:

“Mortgage rates have been revised slightly lower as signals from the economy suggest that it will be appropriate for the Fed to begin to cut its Federal Funds rate in 2024. Our yearly mortgage rate average forecast is down to 6.7%, and we revised our year-end forecast to 6.3% from 6.5%.”

Know Your Number for Mortgage Rates

So, what does this mean for you and your plans to move? If you’ve been holding out and waiting for rates to come down, know that it’s already happening. You just have to decide, based on the expert projections and your own budget, when you’ll be willing to jump back in. As Sam Khater, Chief Economist at Freddie Mac, says:

“The decline in mortgage rates does increase prospective homebuyers’ purchasing power and should begin to pique their interest in making a move.”

As a next step, ask yourself this: what number do I want to see rates hit before I’m ready to move?

Maybe it’s 6.25%. Maybe it’s 6.0%. Or maybe it’s once they hit 5.99%. The exact percentage where you feel comfortable kicking off your search again is personal. Once you have that number in mind, you don’t need to follow rates yourself and wait for it to become a reality.

Instead, connect with a local real estate professional. They’ll help you stay up to date on what’s happening and have a conversation about when to make your move. And once rates hit your target, they’ll be the first to let you know.

Bottom Line

If you’ve put your moving plans on hold because of higher mortgage rates, think about the number you want to see rates hit that would make you re-enter the market.

Once you have that number in mind, let’s connect so you have someone on your side to let you know when we get there.