Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mortgage Rates Down a Full Percent from Recent High

Mortgage rates have been one of the hottest topics in the housing market lately because of their impact on affordability. And if you’re someone who’s looking to make a move, you’ve probably been waiting eagerly for rates to come down for that very reason. Well, if the past few weeks are any indication, you may be getting your wish.

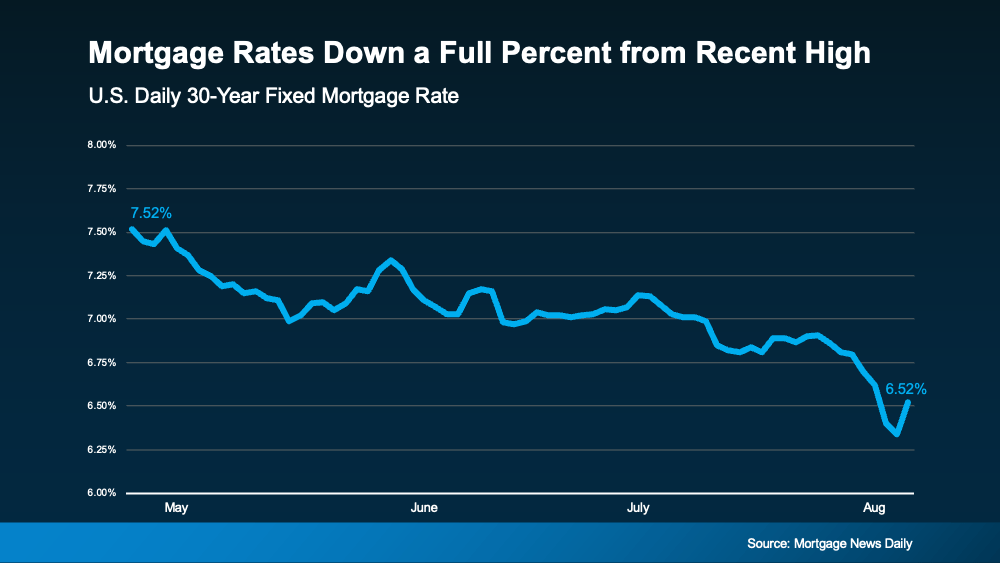

Mortgage Rates Trend Down in Recent Weeks

There’s big news for mortgage rates. After the latest reports on the economy, inflation, the unemployment rate, and the Federal Reserve’s recent comments, mortgage rates started dropping a bit. And according to Freddie Mac, they’re now at a level we haven’t seen since February. To help show the downward trend, check out the graph below:

Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says:

Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“The hopes for lower interest rates need the reality check that ‘lower’ doesn’t mean we’re going back to 3% mortgage rates. . . the best we may be able to hope for over the next year is 5.5 to 6%.”

And with the decrease in recent weeks, you’ve got a big opportunity in front of you right now. It may be enough for you to want to jump back in.

The Relationship Between Rates and Demand

If you wait for mortgage rates to drop further, you might find yourself dealing with more competition as other buyers re-ignite their home searches too.

In the housing market, there’s generally a relationship between mortgage rates and buyer demand. Typically, the higher rates are, the lower buyer demand is. But when rates start to come down, things change. Buyers who were on the fence over higher rates will resume their searches. Here’s what that means for you. As a recent article from Bankrate says:

“If you’re ready to buy, now might be the time to strike. Home prices have been rising primarily because of a longstanding shortage of homes for sale. That’s unlikely to change, and if mortgage rates do fall below 6%, it’s possible buyers would enter the market en masse, further pushing up prices and resurrecting bidding wars.”

Bottom Line

If you’ve been waiting to make your move, the recent downward trend in mortgage rates may be enough to get you off the sidelines. Rates have hit their lowest point in months, and that gives you the opportunity to jump back in before all the other buyers do too.

If you’re ready and able to start the process, reach out and let’s get started.

Are Home Prices Going To Come Down?

Today’s headlines and news stories about home prices are confusing and make it tough to know what’s really happening. Some say home prices are heading for a correction, but what do the facts say? Well, it helps to start by looking at what a correction means.

Today’s headlines and news stories about home prices are confusing and make it tough to know what’s really happening. Some say home prices are heading for a correction, but what do the facts say? Well, it helps to start by looking at what a correction means.

Here’s what Danielle Hale, Chief Economist at Realtor.com, says:

“In stock market terms, a correction is generally referred to as a 10 to 20% drop in prices . . . We don’t have the same established definitions in the housing market.”

In the context of today’s housing market, it doesn’t mean home prices are going to fall dramatically. It only means prices, which have been increasing rapidly over the last couple years, are normalizing a bit. In other words, they’re now growing at a slower pace. Prices vary a lot by local market, but rest assured, a big drop off isn’t what’s happening at a national level.

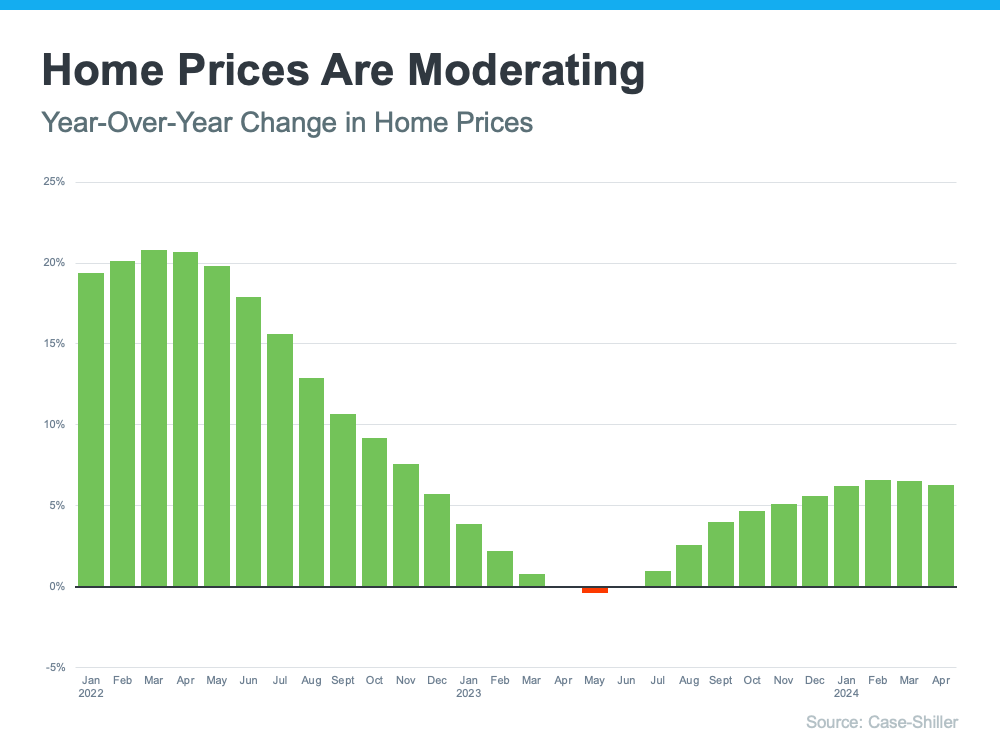

The Real Estate Market Is Normalizing

From 2020 to 2022, home prices skyrocketed. That rapid increase was due to high demand, low interest rates, and a shortage of homes for sale. But, that kind of aggressive growth couldn’t continue forever.

Today, price growth has started to slow down, which is a sign the market is beginning to normalize. The most recent data from Case-Shiller shows that after being basically flat for a couple of months last year, prices are going up at a national level – just not as quickly as before (see graph below):

The big takeaway? So far this year, there’s been a much healthier pace of price growth compared to the pandemic.

The big takeaway? So far this year, there’s been a much healthier pace of price growth compared to the pandemic.

Of course, that’s what’s happening now, but you may be wondering what’s next for prices. Marco Santarelli, the Founder of Norada Real Estate Investments, says:

“Expert forecasts lean towards a moderation in home price growth over the next five years. This translates to a slower and more sustainable pace of appreciation compared to the breakneck speed witnessed in recent years, rather than a freefall in prices.”

It’s all about supply and demand. Increasing inventory plus limited buyer demand, due to relatively high mortgage rates, will continue to ease some of the upward pressure on prices.

What This Means for You

If you’re thinking about buying a home, slowing price growth is welcome news. Skyrocketing home prices during the pandemic left many would-be homebuyers feeling priced-out.

While it’s still a good thing to know the value of the home you buy will likely continue to go up once you own it, slowing price gains are making things feel more manageable. Odeta Kushi, Deputy Chief Economist at First American, says:

“While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help — so the dream of homeownership isn’t boarded up just yet.”

Bottom Line

At the national level, home prices are not going down. And most experts forecast they’ll continue growing moderately moving forward. But prices vary a lot by local market. That’s where a trusted real estate agent comes into play. If you have questions about what’s happening with prices in our area, reach out.

How Affordability and Remote Work Are Changing Where People Live

There’s an interesting trend happening in the housing market. People are increasingly moving to more affordable areas, and remote or hybrid work is helping them do it.

Consider Moving to a More Affordable Area

Today’s high mortgage rates combined with continually rising home prices mean it’s tough for a lot of people to afford a home right now. That’s why many interested buyers are moving to places where homes are less expensive, and the cost of living is lower. As Orphe Divounguy, Senior Economist at Zillow, explains:

“Housing affordability has always mattered . . . and you’re seeing it across the country. Housing affordability is reshaping migration trends.”

If you’re hoping to buy a home soon, it might make sense to broaden your search area to include places where homes that fit your needs are more affordable. That’s what a lot of other people are doing right now to find a home within their budget. Extra Space Storage explains:

“55% of American adults are looking to relocate to a different state or city for more affordable homes and lower costs of living. . . Specifically, states with a strong economy, lower costs of living, and remote work options continue to be the ideal places to live in the U.S.”

Remote Work Opens Up More Home Options

If you work remotely or drive into the office only a few times each week, you have many more possibilities when looking for your next home. That’s because you can cast a broader net and include more suburban or rural areas nearby. As Market Place Homes says:

“People start to reconsider where they want to live when commute times are slashed in half or eliminated altogether. If they have a longer commute but don’t have to do it daily, they may feel like they can tolerate living farther away from their job. Or, if someone works entirely remotely, they can move to a cheaper area and get a lot of house for their dollar.”

How a Real Estate Agent Can Help

A real estate agent can help you find the perfect home for your budget. They’re especially valuable if you’re moving to a new, unfamiliar area. Bankrate says:

“If you’re moving far away, you may not have a good idea about which neighborhoods or towns will be the best fit. An experienced local agent can help you find the lifestyle you’re looking for in a home you can afford.”

So, if you’re thinking about relocating to somewhere with more affordable homes, what are you waiting for? With the added flexibility of remote work, you might have more options than before.

Bottom Line

Dreaming of a place where your money goes further? Let’s connect so you have someone to help you find your next home. Together, we’ll make your dream of homeownership a reality.

How To Determine if You’re Ready To Buy a Home

If you’re trying to decide if you’re ready to buy a home, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates and home prices, the limited supply of homes for sale, and more. And, you’re juggling how all of those things will impact the choice you’ll make.

While housing market conditions are definitely a factor in your decision, your own personal situation and your finances matter too. As an article from NerdWallet says:

“Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”

Instead of trying to time the market, focus on what you can control. Here are a few questions that can give you clarity on whether you’re ready to make your move.

1. Do You Have a Stable Job?

One thing to consider is how stable you feel your employment is. Buying a home is a big purchase, and you’re going to sign a home loan stating you’ll pay that loan back. That’s a big commitment. Knowing you have a reliable job and a steady stream of income coming in can help put your mind at ease when making such a large purchase.

2. Have You Figured Out What You Can Afford?

If you have reliable paychecks coming in, the next thing to figure out is what you can afford. That’ll depend on your spending habits, debt, and more. To be sure you have a good idea of what to expect from a number’s perspective, start by talking to a trusted lender.

They’ll be able to tell you about the pre-approval process and what you’re qualified to borrow, current mortgage rates and your approximate monthly payment, closing costs to anticipate, and other expenses you’ll want to budget for. That way you can make an informed decision about whether you’re ready to buy.

3. Do You Have an Emergency Fund?

Another key factor is whether you’ll have enough cash left over in case of an emergency. While that’s not fun to think about, it’s an important thing to consider. You don’t want to overextend on the house, and then not be able to weather a storm if one comes along. As CNET says:

“You’ll want to have a financial cushion that can cover several months of living expenses, including mortgage payments, in case of unforeseen circumstances, such as job loss or medical emergencies.”

4. How Long Do You Plan To Live There?

It was mentioned above, but buying a home involves some upfront expenses. And while you’ll get that money back (and more) as you gain equity, that process takes time. If you plan to move too soon, you may not recoup your investment. For example, if you’re looking to sell and move again in a year, it might not make sense to buy right now. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Five years is a good, comfortable mark. If the price of your home appreciates considerably, then even three years would be fine.”

So, think about your future. If you plan to transfer to a new city with the upcoming promotion you’re working toward or you anticipate your loved ones will need you to move closer to take care of them, that’s something to factor in.

5. Above all else, the most important question to answer is: do you have a team of real estate professionals in place?

If not, finding a trusted local agent and a lender is a good first step. The pros can talk you through your options and help you decide if you’re ready to take the plunge or if you have a few more things to get in order first.

Bottom Line

If you want to have a conversation about all the things you need to consider to determine if you’re ready to buy, let’s connect.

Why Your Asking Price Matters Even More Right Now

If you’re thinking about selling your house, here’s something you really need to know. Even though it’s still a seller’s market today, you can’t pick just any price for your listing.

While home prices are still appreciating in most areas, they’re climbing at a slower pace because higher mortgage rates are putting a squeeze on buyer demand. At the same time, the supply of homes for sale is growing. That means buyers have more options and your house may not stand out as much, if it’s not priced right.

Those two factors combined are why the asking price you set for your house is more important today than it has been in recent years.

And some sellers are finding that out the hard way. That’s leading to more price reductions. Mike Simonsen, Founder and President of ALTOS Research, explains:

“Looking at the price reductions data set . . . It all fits in the same pattern of increasing supply and homebuyer demand that is just exhausted by high mortgage rates. . . As home sellers are faced with less demand than they expected, more of them have to reduce their prices.”

That’s because they haven’t adjusted their expectations to today’s market. Maybe they’re not working with an agent, so they don’t know what’s happening around them. Or they’re not using an agent who prioritizes being a local market expert. Either way, they aren’t basing their pricing decision on the latest data available – and that’s a miss.

If you want to avoid making a pricing mistake that could turn away buyers and delay your sale, you need to work with an agent who really knows your local market. If you lean on the right agent, they’ll help you avoid making mistakes like:

- Setting a Price That’s Too High: Some sellers have unrealistic expectations about how much their house is worth. That’s because they base their price on their gut or their bottom line, not the data. An agent will help you base your price on facts, not opinion, so you have a better chance of hitting the mark.

- Not Considering What Houses Are Actually Selling for: Without an agent’s help, some sellers may use the wrong comparable sales (comps) in their area and misjudge the market value of their home. An agent has the expertise needed to find true comps. And they’ll use those to give you valuable insights into how to price your house in a way that’s competitive for you and your future buyer.

- Overestimating Home Improvements: Sellers who have invested a significant amount of money in home improvements may overestimate how much those upgrades affect their home’s value. While certain improvements can increase a home’s appeal, not all upgrades are going to get a great return on their investment. An agent factors in what you’ve done and what buyers in your area actually want as they set the price.

- Ignoring Feedback and Market Response: Some sellers may be resistant to lowering their asking price based on feedback they’re getting in open houses. An agent will remind the seller how important it is to be flexible and respond to market feedback in order to attract qualified buyers.

In the end, accurate pricing depends on current market conditions – and only an agent has all the data and information necessary to find the right price for your house. The right agent will use that expertise to develop a pricing strategy that’s based on current market conditions and designed to get your house sold. That way you don’t miss the mark.

Bottom Line

The right asking price is even more important today than it’s been over the last few years. To avoid making a costly mistake, let’s work together.

Homeowners Gained $28K in Equity over the Past Year

If you own a home, your net worth has probably gone up a lot over the past year. Home prices have been rising, which means you’re building equity much faster than you might think. Here’s how it works.

Equity is the current value of your home minus what you owe on the loan.

Over the past year, there have still been more people wanting to buy than there are homes available for sale, and that’s pushed prices up. That rise in prices has translated directly into increasing equity for homeowners.

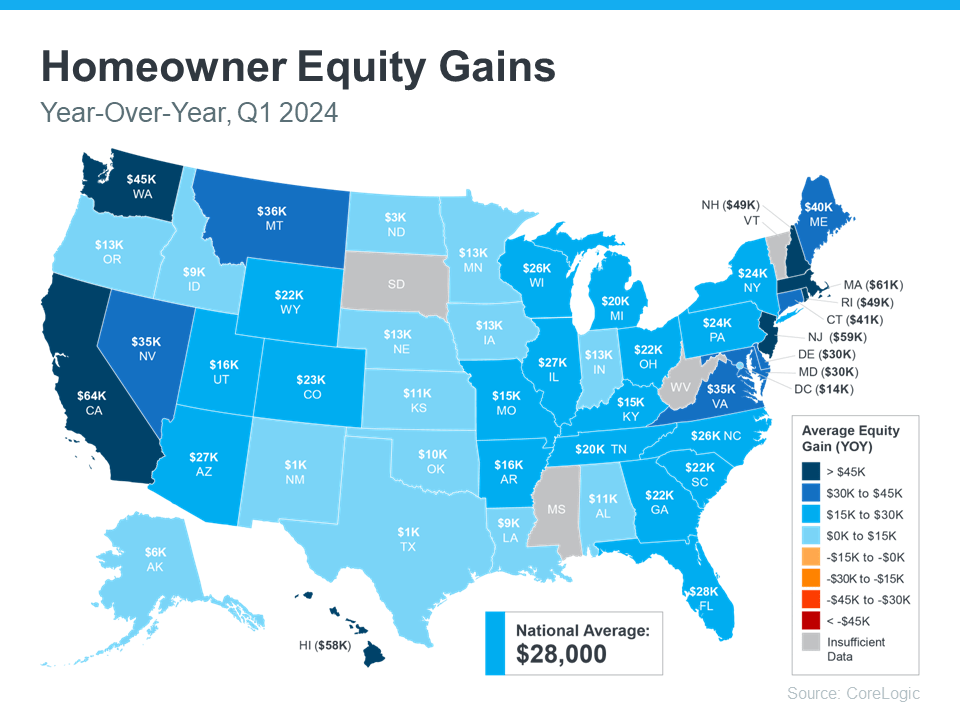

How Much Equity Have You Earned over the Past 12 Months?

According to the latest Homeowner Equity Insights from CoreLogic, the average homeowner’s equity has grown by $28,000 in the last year alone.

That’s the national average, so if you want to see what’s happening in your state, check out the map below. It uses data from CoreLogic to show how much equity has grown in each state over the past year. You’ll notice every single state with sufficient data saw annual equity gains:

What If You Bought Your House Before the Pandemic?

If you bought your house before the pandemic, the equity news is even better. According to data from Realtor.com, home prices shot up by 37.5% from May 2019 to May 2024, meaning your home’s value has likely increased significantly. Ralph McLaughlin, Senior Economist at Realtor.com, says:

“Homeowners have seen extraordinary gains in home equity over the past five years.”

To give context to how much equity can stack up over time, Selma Hepp, Chief Economist at CoreLogic, explains the total equity the typical homeowner has today:

“With home prices continuing to reach new highs, owners are also seeing their equity approach the historic peaks of 2023, close to a total of $305,000 per owner.”

How Your Rising Home Equity Can Help You

With how prices skyrocketed a few years ago, and the ongoing price growth today, homeowners clearly have substantial equity built up – and that has some serious benefits.

You could use it to start a business, fund an education, or even to help you afford your next home. When you sell, the equity you’ve built up comes back to you, and may be enough to cover a big part – or even all – of your next home’s down payment.

Bottom Line

If you’re planning to move, the equity you’ve gained can really help. Curious about how much you have and how you can use it to help pay for your next home? Let’s connect.

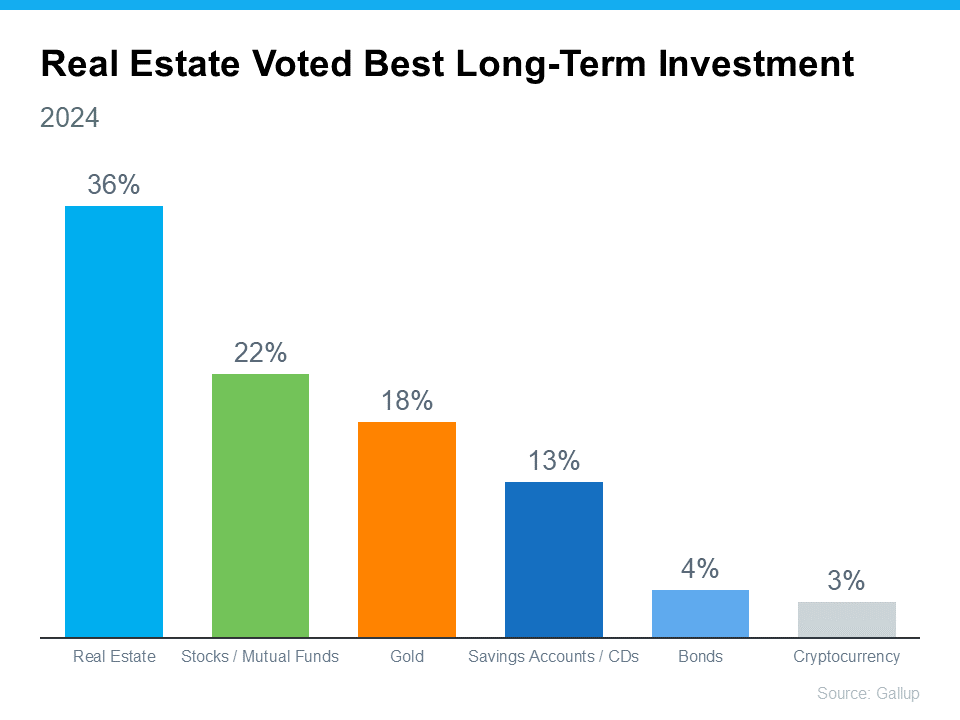

Real Estate Still Holds the Title of Best Long-Term Investment

With all the headlines circulating about home prices and mortgage rates, you may be asking yourself if it still makes sense to buy a home right now, or if it’s better to keep renting. Here’s some information that could help put your mind at ease by showing that investing in a home is still a powerful decision.

According to the experts at Gallup, real estate has been crowned the top long-term investment for a whopping 12 years in a row. It has consistently beat out other investment types like gold, stocks, and bonds. Just take a look at the graph below – it speaks volumes:

But why does real estate continue to reign supreme as a top-notch long-term investment? It’s because, even today, buying a home can be your golden ticket to building wealth over time.

Unlike other investments that can feel a bit like riding a rollercoaster with all the ups and downs and ongoing risk factors, real estate follows a more predictable and positive pattern.

History shows home values usually rise. And while prices may vary by market, that means as time goes by, your house is likely to appreciate in value. And that helps you grow your net worth in a big way. As an article from Realtor.com explains:

“Homeownership has long been tied to building wealth—and for good reason. Instead of throwing rent money out the window each month, owning a home allows you to build home equity. And over time, equity can turn your mortgage debt into a sizeable asset.”

So, if you’re on the fence about whether to rent or buy, remember that real estate was consistently voted the best long-term investment for a reason. And if you want to get in on that action, it may make sense to go ahead and buy (if you’re ready and able).

Bottom Line

When it comes to building wealth that stands the test of time, real estate is the name of the game. If you’re ready to start on your own journey toward homeownership, let’s connect today.

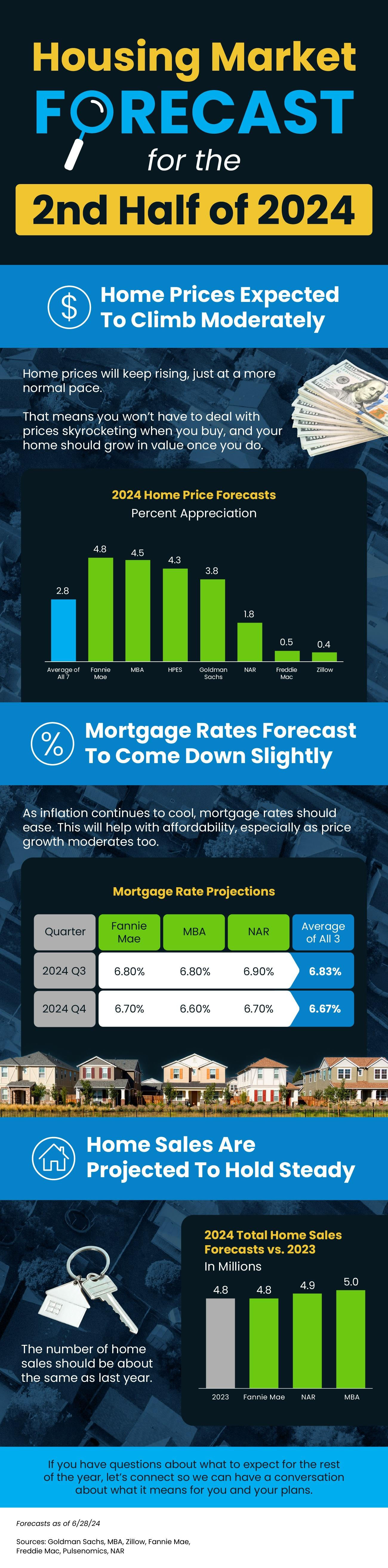

Housing Market Forecast for the 2nd Half of 2024

Wondering what the second half of the year holds for the housing market? Here’s what expert forecasts say. Home prices are expected to climb moderately. Mortgage rates are forecast to come down slightly. And, home sales are projected to hold steady. If you have questions about what to expect for the rest of the year, DM me so we can have a conversation about what it means for you and your plans.

Focus on Time in the Market, Not Timing the Market

Should you buy a home now or should you wait? That’s a big question on many people’s minds today. And while what timing is right for you will depend on a lot of other personal factors, here’s something you may not have considered.

If you’re able to buy at today’s rates and prices, it may be better to focus on time in the market, rather than timing the market.

The Downside of Trying To Time the Market

Trying to time the market isn’t a good strategy because things can change. Here’s an example. For the better part of this year, projections have said mortgage rates will come down. And while experts agree that’s still what’s ahead, shifts in various market and economic factors have pushed back the timing of when that’ll happen. Here’s how that’s impacted homebuyers who’ve been sitting on the sidelines. As U.S. News says:

“Those who put off buying a home during the past few years as they were holding out for lower mortgage rates have been left out of the market . . . mortgage rates have stayed higher for longer than previously expected, keeping monthly housing payments elevated. In other words, affordability didn’t improve for those who chose to wait.”

This is why timing the market may not pay off if you’re ready and able to buy now.

The Proof Is in the Pudding: How Homeowners Benefit from Rising Home Prices

Delaying your plans also means missing out on the equity you’d gain if you went ahead with your purchase today. And the potential equity gains that are at stake may surprise you.

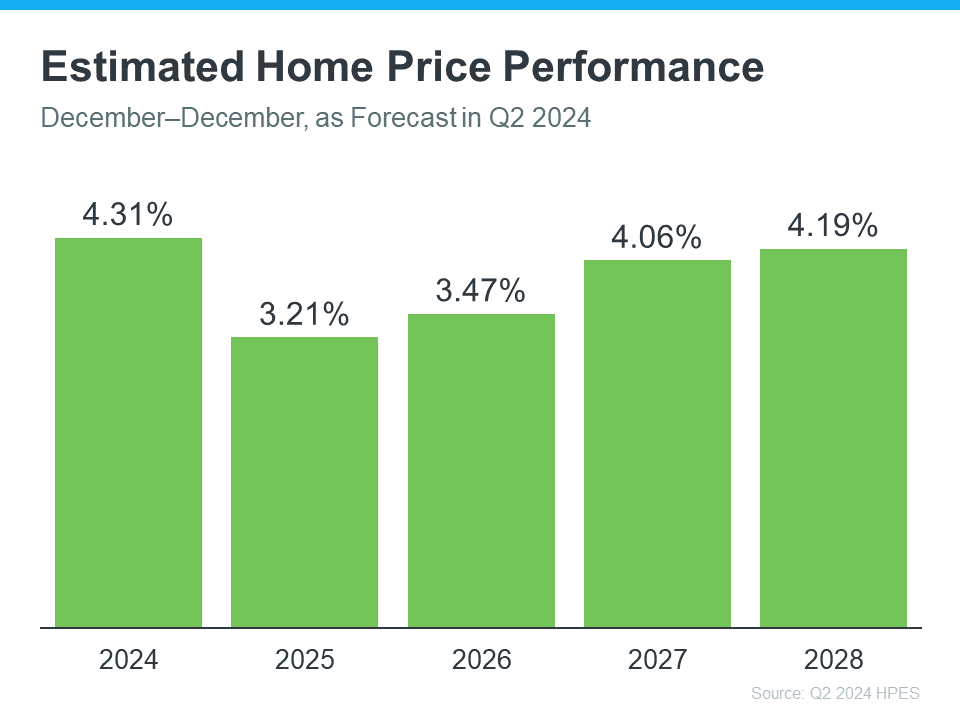

Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2028 (see the graph below):

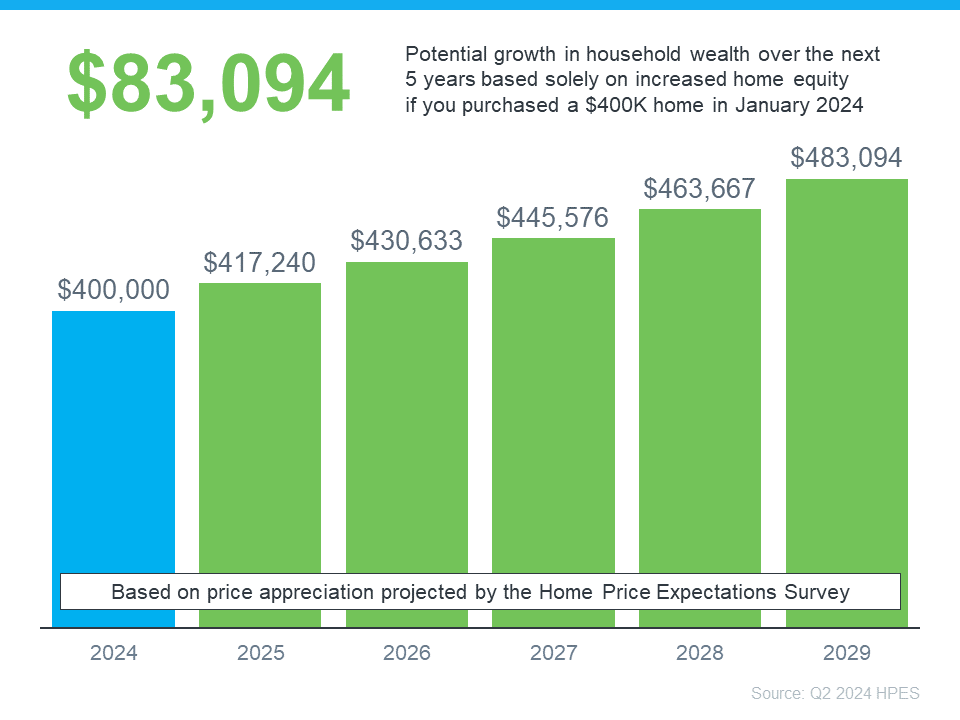

To give these numbers context, let’s take a look at a breakdown of what you stand to gain once you buy. The graph below uses a typical home’s value to show how a home could appreciate over the next few years using those HPES projections:

In this example, let’s say you went ahead and bought a $400,000 home at the beginning of this year. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number.

This data helps paint the picture of why time in the market really matters.

The Advice You Need To Hear If You’re Ready and Able To Buy Now

Right now, you may be focused on what’s happening with mortgage rates and how those impact your monthly payment, but don’t forget to factor in home prices.

Prices are expected to continue climbing, just at a more moderate pace. And while a moderate rise in prices may not be fun for you now, once you own a home, that growth will be a huge perk. That’s the time in the market piece.

Sure, you could try timing the market, but the equity you’ll be missing out on in the meantime is something to seriously consider. If you’re ready and able to buy now, you have to decide: is it really worth waiting?

Rather than focusing on timing the market. It’s better to have time in the market.

As U.S. News Real Estate sums up:

“There’s never a one-size-fits-all answer to whether now is the right time to buy a home. . . . There’s also no way to predict precisely what the market will do in the near future . . . Perfectly timing the market shouldn’t be the goal. This decision should be determined by your personal needs, financial means and the time you have to find the right home.”

Bottom Line

If you’re debating whether to buy now or wait, remember it’s time in the market, not timing the market. And if you want to get the ball rolling and set yourself up for those big equity gains, let’s connect to make it happen.

Housing Market Forecast: What’s Ahead for the 2nd Half of 2024

As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home sales.

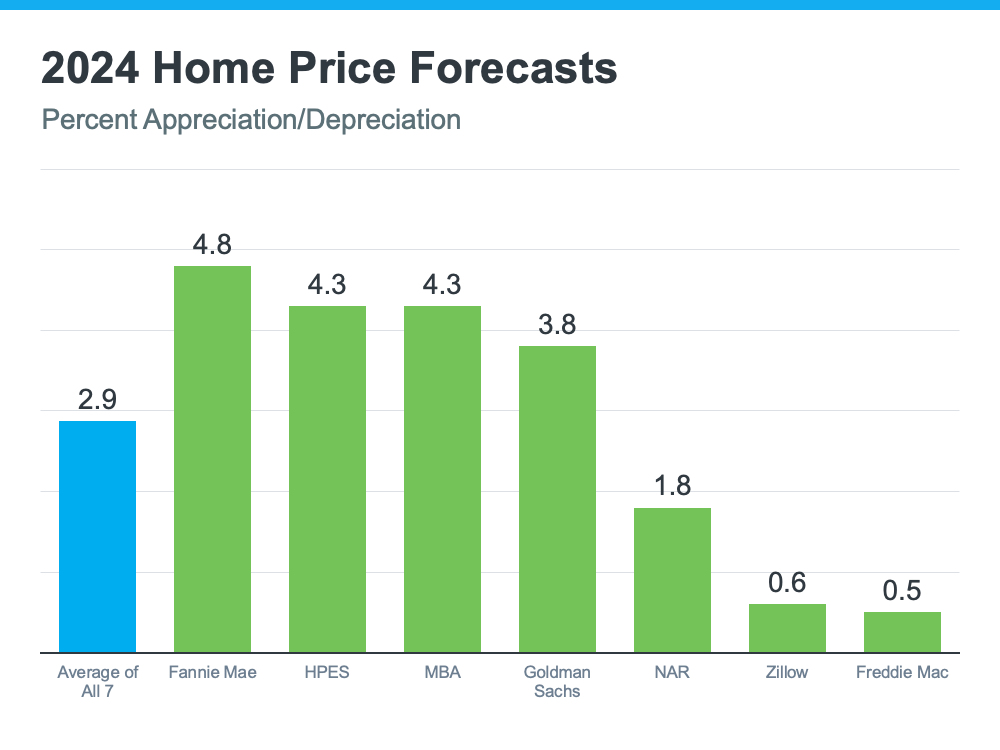

Home Prices Are Expected To Climb Moderately

Home prices are forecasted to rise at a more normal pace. The graph below shows the latest forecasts from seven of the most trusted sources in the industry:

The reason for continued appreciation? The supply of homes for sale. Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), explains:

“One thing that seems to be pretty solid is that home prices are going to continue to go up, and the reason is that we don’t have housing inventory.”

While inventory is up compared to the last couple of years, it’s still low overall. And because there still aren’t enough homes to go around, that’ll keep upward pressure on prices.

If you’re thinking of buying, the good news is you won’t have to deal with prices skyrocketing like they did during the pandemic. Just remember, prices aren’t expected to drop. They’ll continue climbing, just at a slower pace.

So, getting into the market sooner rather than later could still save you money in the long run. Plus, you can feel confident experts say your home will grow in value after you buy it.

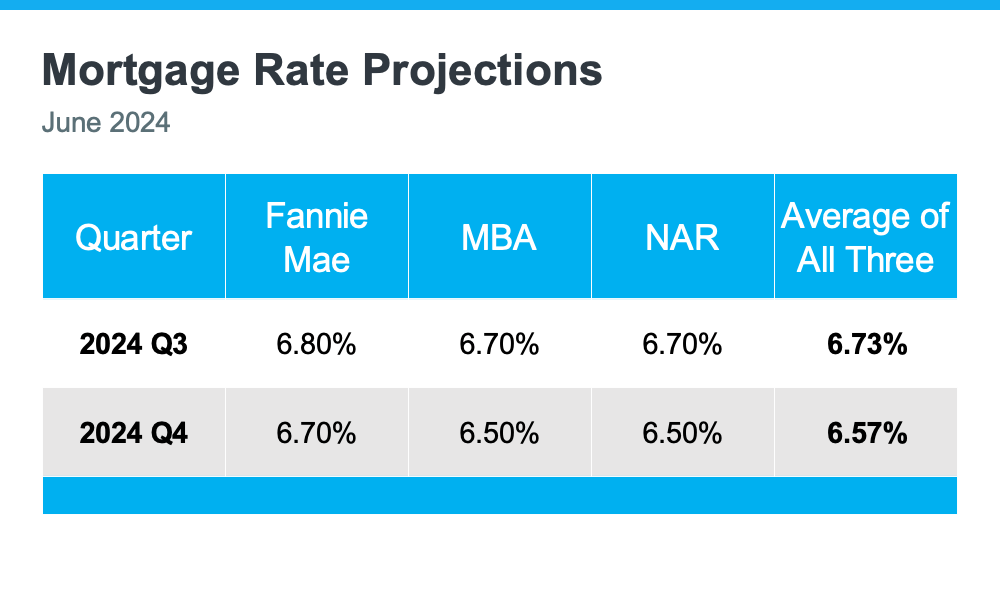

Mortgage Rates Are Forecast To Come Down Slightly

One of the best pieces of news for both buyers and sellers is that mortgage rates are expected to come down a bit, according to Fannie Mae, the Mortgage Bankers Association (MBA), and NAR (see chart below):

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

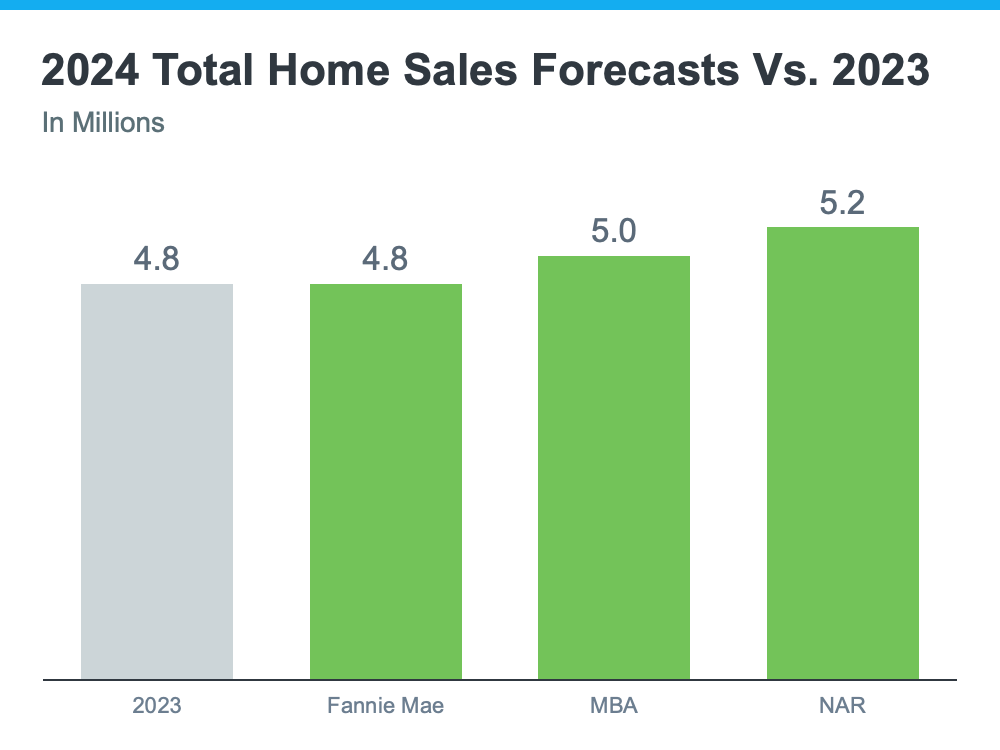

Home Sales Are Projected To Hold Steady

For 2024, the number of home sales will be about the same as last year and may even rise slightly. The graph below compares the 2024 home sales forecasts from Fannie Mae, MBA, and NAR to the 4.8 million homes that sold last year:

The average of the three forecasts is about 5 million sales in 2024 – a small increase from 2023. Lawrence Yun, Chief Economist at NAR, explains why:

“Job gains, steady mortgage rates and the release of inventory from pent-up home sellers will lead to more sales.”

With more inventory available and mortgage rates expected to go down, a few more homes are expected to be sold this year compared to last year. This means more people will be able to move. Let’s work together to make sure you’re one of them.

Bottom Line

If you have any questions or need help navigating the market, reach out.