Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Do Elections Impact the Housing Market?

The 2024 Presidential election is just months away. As someone who’s thinking about potentially buying or selling a home, you’re probably curious about what effect, if any, elections have on the housing market.

It’s a great question because buying or selling a home is a major decision, and it’s natural to wonder how such a major event might impact your plans.

Historically, Presidential elections have only had a small, temporary impact on the housing market. Here’s the latest on exactly what’s happened to home sales, prices, and mortgage rates throughout those time periods.

Home Sales

During the month of November, in years when the Presidential election takes place, there’s typically a slight slowdown in home sales. As Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mostly because some people feel uncertain and hesitant about making big decisions during such a pivotal time. However, it’s important to know this slowdown is temporary. Historically, home sales bounce back in December and continue to rise the following year.

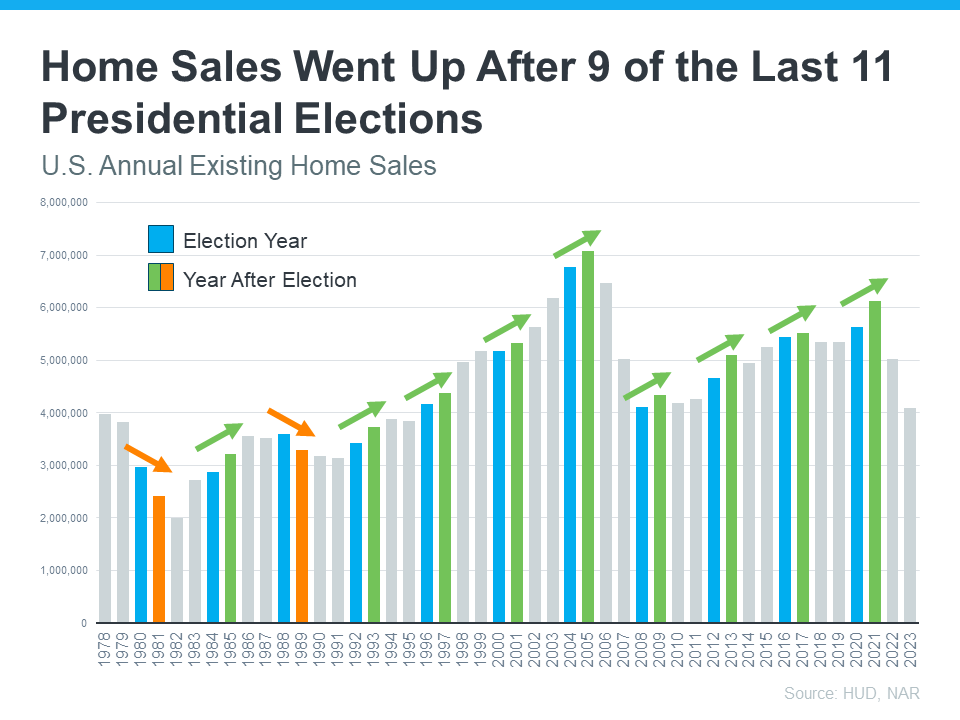

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after nine of the last 11 Presidential elections, home sales went up the next year (see graph below):

The graph shows annual home sales going back to 1978. Each year with a Presidential election is noted in blue. The year immediately after each election is green if existing home sales rose that year. The two orange bars represent the only years when home sales decreased after an election.

Home Prices

What about home prices? Do they drop during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist puts it:

“An election year doesn’t alter the price trend that is already happening in the market.”

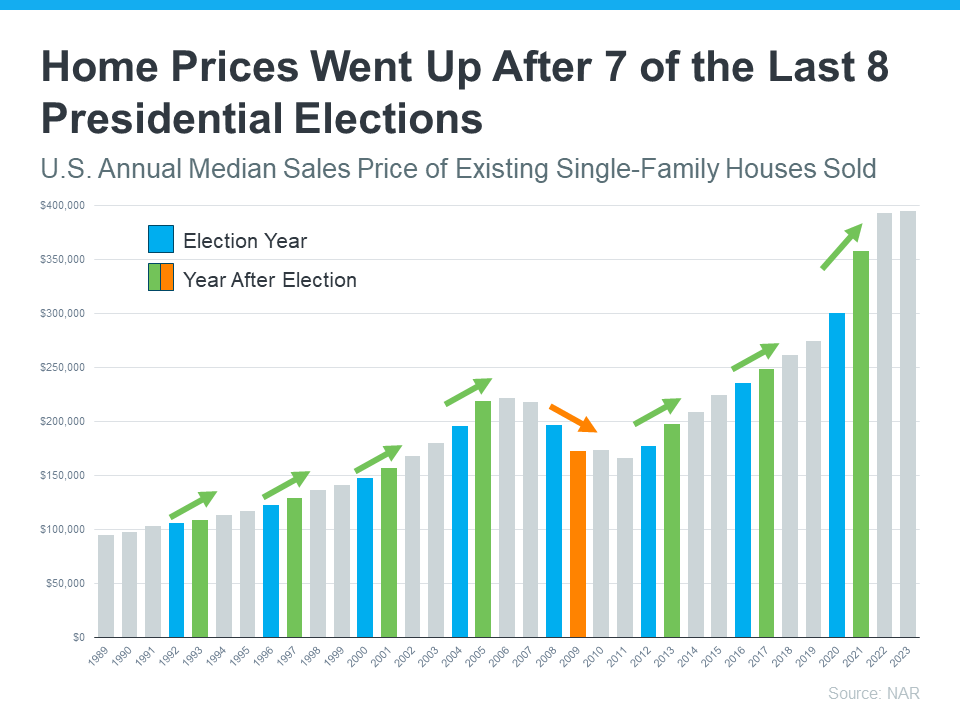

Home prices are pretty resilient. They generally rise year-over-year, regardless of elections. The latest data from NAR shows after seven of the last eight Presidential elections, home prices increased the following year (see graph below):

Just like the previous graph, this shows election years in blue. The only year when prices declined after an election is in orange. That was during the housing market crash, which was far from a typical year. Today’s market is different than it was back then.

All the green bars represent when prices rose the following year. So, if you’re worried about your home losing value because of an election, you can rest easy knowing prices rise after most Presidential elections.

Mortgage Rates

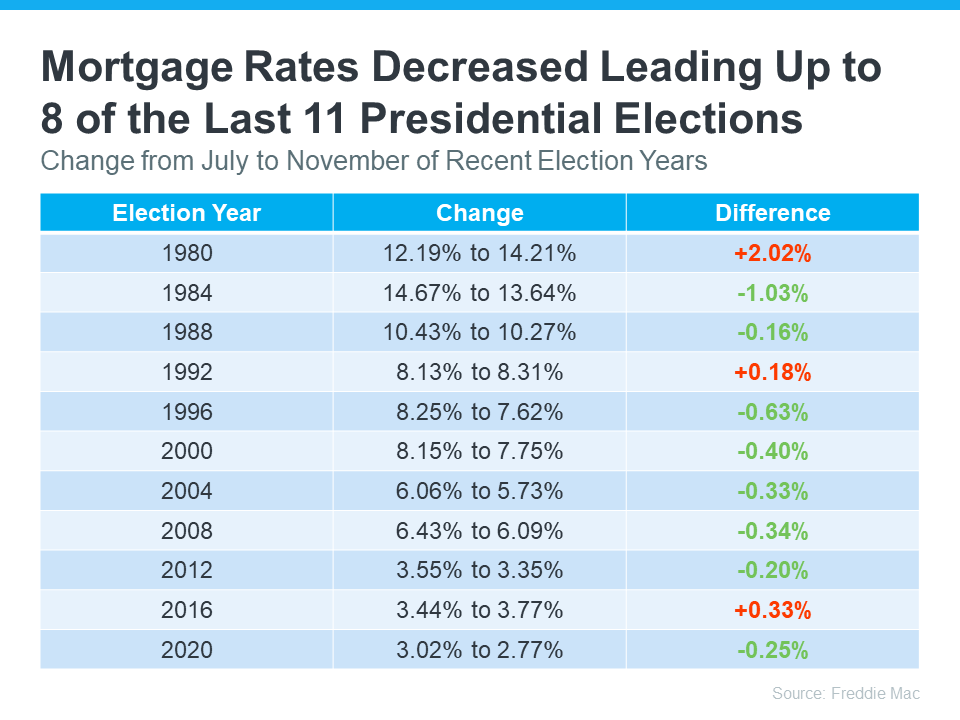

Mortgage rates are important because they affect how much your monthly payment will be when you buy a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in eight of them (see chart below):

Most forecasts expect mortgage rates to ease slightly throughout the remainder of the year. If they’re right, this year will follow the trend of declining rates leading up to most previous elections. And if you’re looking to buy a home in the coming months, this could be good news, as lower rates could mean a lower monthly payment.

What This Means for You

So, what’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually small and temporary. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. For help navigating the market, election year or not, let’s connect.

Home Prices Aren’t Declining, But Headlines Might Make You Think They Are

If you’ve seen the news lately about home sellers slashing prices, it’s a great example of how headlines do more to terrify than clarify. Here’s what’s really happening with prices.

The bottom line is home prices are higher than they were a year ago at this time, and they’re expected to keep rising, just at a slower pace.

But a recent article from Redfin notes,

“Price Drops Hit Highest Level in 18 Months As High Rates Dampen Buyer Demand.”

And that might make you think prices are declining.

Now, while it’s true the latest report from Realtor.com also shows 16.6% of homes on the market had price reductions in May, which is up from 12.7% last May, that doesn’t mean overall home prices are falling.

The key is knowing the difference between the asking price and the sold price.

Understanding Asking Price vs. Sold Price

In essence, the asking price, also known as a listing price, is the amount a seller hopes to get for their home when they list it. In reality, sellers can’t just put any price tag on their house and expect it to sell for top dollar. Today’s buyers are savvy customers, and when they aren’t willing to pay a premium for a home because their budgets are strained by higher mortgage rates, sellers need to adjust. And that’s what’s happening right now.

Based on market factors and what offers that seller receives, that asking price can change. If a seller isn’t getting much foot traffic, you may see them revise the price and make an adjustment to reignite interest in the home – and sometimes that’s because they’ve overpriced it from the start. That’s where price reductions come in, and when you see “price drops” in a headline, it sounds like declining home prices.

Mike Simonsen, CEO and Founder of Altos Research, says:

“Not only is the share of homes with price cuts elevated compared to one year ago, but more price cuts are happening each week than last year.”

On the other hand, the final sold price is the amount a buyer actually pays when the transaction is complete.

Here’s the most important thing to note: Actual sold prices are still rising, and they’re expected to continue to do so at least over the next 5 years.

What Does This Mean for Home Prices?

So, while there’s been an increase in price reductions recently, this doesn’t mean overall home values are declining. Instead, it’s a sign that demand is moderating. And, as a result, sellers are adjusting their expectations to align with today’s market reality.

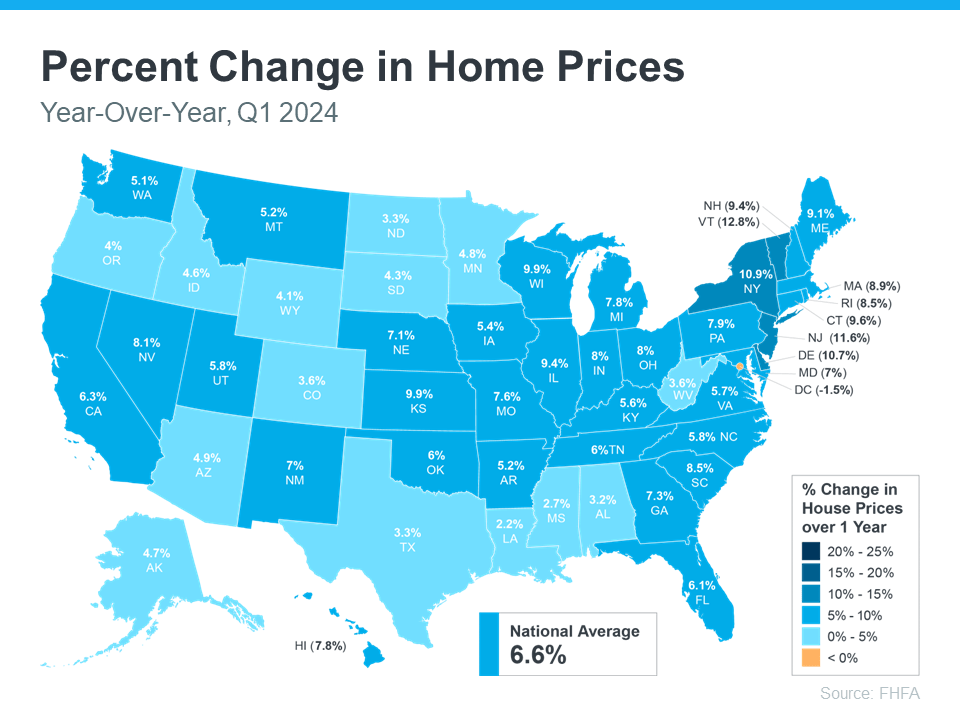

Even with more price reductions, home values are still growing on an annual basis, as they do nearly every year in the housing market. According to the Federal Housing Finance Agency (FHFA), home prices went up 6.6% over the last year (see below):

This map shows how prices rose just about everywhere in the country, indicating the market is not in decline.

So, while seller price reductions are often a leading indicator that prices may moderate in the months ahead, which experts have been saying for a while is expected to happen, they aren’t necessarily reason for alarm. The same article from Redfin also states:

“. . .those metrics suggest sale-price growth could soften in the coming months as persistently high mortgage rates turn off homebuyers. For now, the median-home sale price is up 4.3% year over year to another record high. . .”

And with inventory as tight as it is today, price moderation is much more likely in upcoming months than price declines.

Why This Is Good News for Buyers and Sellers

For buyers, more realistic asking prices mean a better chance of securing a home at a fair price. It also means you can enter the market with more confidence, knowing prices are stabilizing rather than continuing to skyrocket.

For sellers, understanding the need to adjust your asking price can lead to faster sales and fewer price negotiations. Setting a realistic price from the start can attract more serious buyers and lead to smoother transactions.

Bottom Line

While the uptick in price reductions might seem troubling, it’s not a cause for concern. It reflects a market adjusting to new conditions. Home prices are continuing to grow, just at a more moderate pace.

Your Equity Could Make a Move Possible

Many homeowners looking to sell feel like they’re stuck between a rock and a hard place right now. Today’s mortgage rates are higher than the one they currently have on their home, and that’s making it harder to want to sell and make a move. Maybe you’re in the same boat.

But what if there was a way to offset these higher borrowing costs? There is. And the money you need probably already exists in your current home in the form of equity.

What Is Equity?

Think of equity as a simple math equation. Freddie Mac explains:

“. . . your home’s equity is the difference between how much your home is worth and how much you owe on your mortgage.”

Your equity grows as you pay down your loan over time and as home prices climb. And thanks to the rapid home price appreciation we saw in recent years, you probably have a whole lot more of it than you realize.

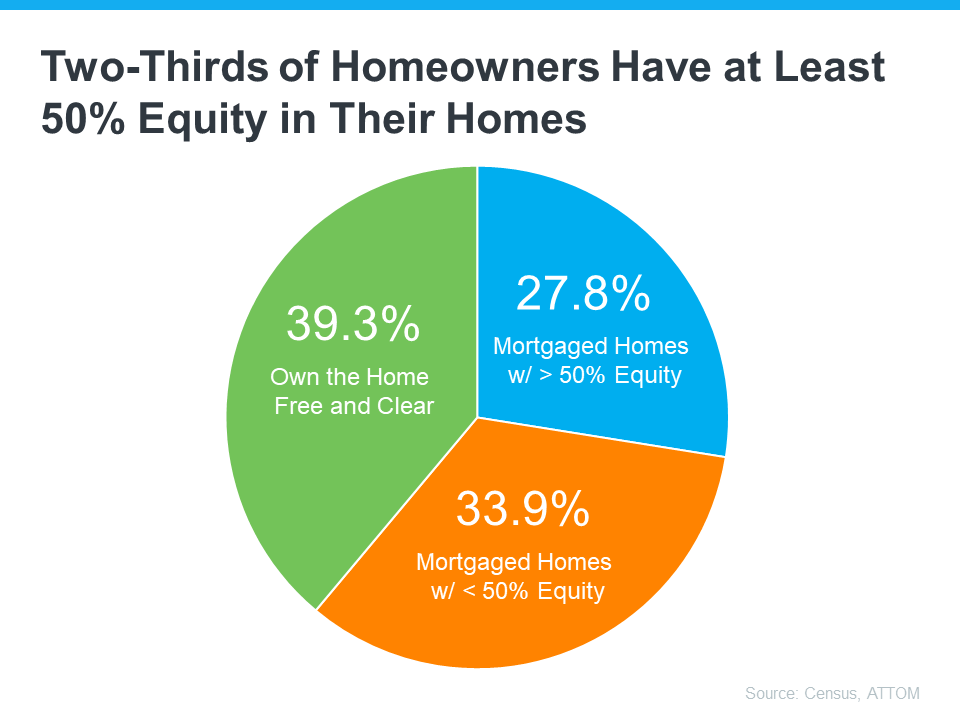

The latest from the Census and ATTOM shows more than two out of three homeowners have either completely paid off their mortgages (shown in green in the chart below) or have at least 50% equity (shown in blue in the chart below):

That means the majority of homeowners have a game-changing amount of equity right now.

How Your Equity Can Help Fuel Your Move

After you sell your house, that equity can help you move without worrying as much about today’s mortgage rates. As Danielle Hale, Chief Economist for Realtor.com says:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

To give you some examples, here are a few ways you can use equity to buy your next home:

- Be an all-cash buyer: If you’ve been living in your current home for a long time, you might have enough equity to buy your next home without having to take out a loan. If that’s the case, you won’t need to borrow any money or worry about mortgage rates.

- Make a larger down payment: Your equity could also be used toward your next down payment. It might even be enough to let you put a larger amount down, so you won’t have to borrow as much at today’s rates.

The First Step: Determine How Much Equity You Have in Your Home

Want to find out how much equity you have? To do that, you’ll need two things:

- The current mortgage balance on your home

- The current value of your home

You can probably find the mortgage balance on your monthly mortgage statement. To understand the current market value of your house, you can pay hundreds of dollars for an appraisal, or you can contact a local real estate agent who will be able to present to you, at no charge, a professional equity assessment report (PEAR).

Once you’ve connected with a trusted local agent and run the numbers, you’re one step closer to making a move you may not have thought was realistic – all thanks to your equity.

Bottom Line

If you want to find out how much equity you have and talk more about how it can make your next move possible, let’s connect.

What’s Next for Home Prices and Mortgage Rates?

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.

The only thing you can really do is make the best decision you can based on the latest information available. So, here’s what experts are saying about both prices and rates.

1. What’s Next for Home Prices?

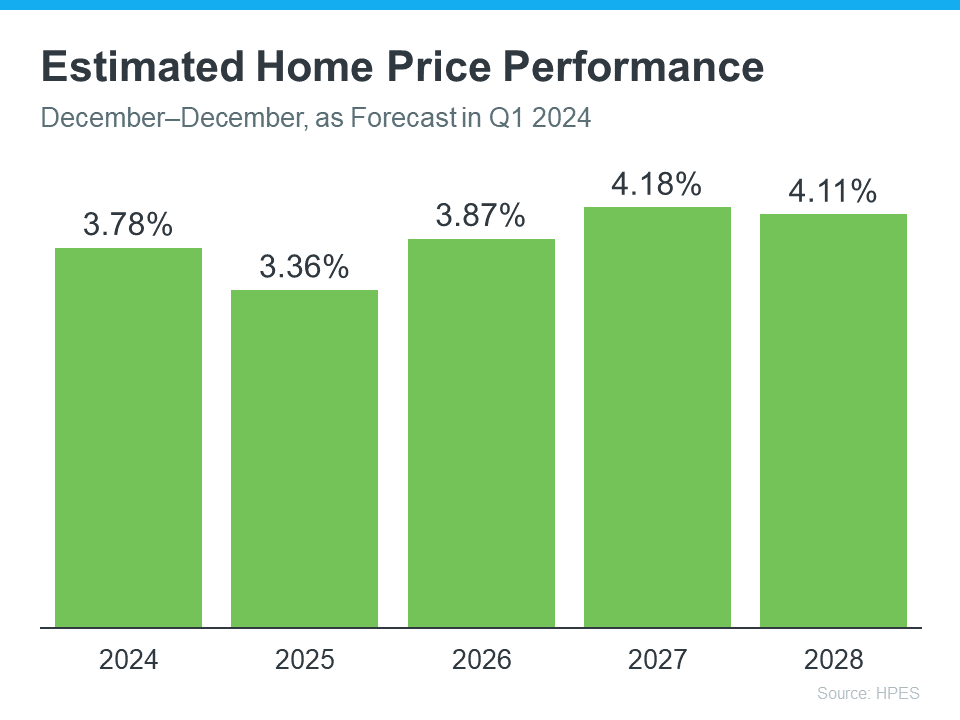

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

According to the most recent release, experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

While the percent of appreciation varies year-to-year, this survey says we’ll see prices rise (not fall) for at least the next 5 years, and at a much more normal pace.

What does that mean for your move? If you buy now, your home will likely grow in value and you should gain equity in the years ahead. But, based on these forecasts, if you wait and prices continue to climb, the price of a home will only be higher later on.

2. When Will Mortgage Rates Come Down?

This is the million-dollar question in the industry. And there’s no easy way to answer it. That’s because there are a number of factors that are contributing to the volatile mortgage rate environment we’re in. Odeta Kushi, Deputy Chief Economist at First American, explains:

“Every month brings a new set of inflation and labor data that can influence the direction of mortgage rates. Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

What happens next will depend on where each of those factors goes from here. Experts are optimistic rates should still come down later this year, but acknowledge changing economic indicators will continue to have an impact. As a CNET article says:

“Though mortgage rates could still go down later in the year, housing market predictions change regularly in response to economic data, geopolitical events and more.”

So, if you’re ready, willing, and able to afford a home right now, partner with a trusted real estate advisor to weigh your options and decide what’s right for you.

Bottom Line

Let’s connect to make sure you have the latest information available on home prices and mortgage rate expectations. Together we’ll go over what the experts are saying so you can make an informed decision on your move.

What’s Motivating Your Move?

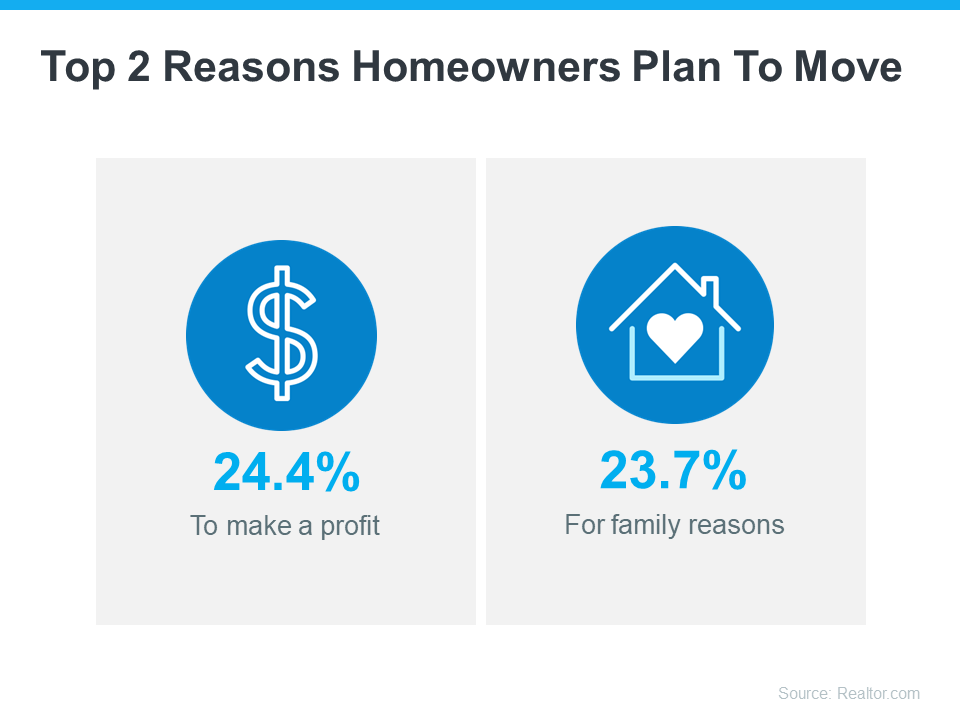

Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving. A recent survey from Realtor.com looked into why people want to sell their homes this year. Here are the top two reasons (see graphic below):

Let’s take a closer look and see if they’re motivating you to make a change too.

1. To Make a Profit

If you’re thinking about selling your house, you probably have a lot of questions on your mind. Well, here’s some good news – the latest data shows most sellers get a great return on their investment when they sell. ATTOM, a property data provider, explains:

“. . . home sellers made a $121,000 profit on the typical sale in 2023, generating a 56.5 percent return on investment.”

That’s significant. And here’s one contributing factor. During the pandemic, home prices skyrocketed. There was way more buyer demand than homes available for sale and that combination pushed prices up.

Now, home prices are still rising, just not as fast. That ongoing appreciation is good news for your bottom line. Any profit you make can help offset some of today’s affordability challenges when you buy your next home.

If you want to know how much your house is worth now and what’s going on with prices in your area, talk to a local real estate agent.

2. For Family Reasons

Maybe you want to be near relatives to help take care of older family members or to have more support nearby. Or maybe you’re just eager to spend time together on special occasions like birthdays and holidays.

Selling a house and moving closer to the people who matter the most to you helps keep you connected. If the distance is making you miss out on some big milestones in their lives, it might be time to talk to a local real estate agent to find a place close by. The National Association of Realtors (NAR) says:

“A great real estate agent will guide you through the home search with an unbiased eye, helping you meet your buying objectives while staying within your budget.”

Bottom Line

If you’re thinking about selling your house, there’s probably a good reason for it. Let’s talk so you have help making the right move to reach your goals this year.

Is It Getting More Affordable To Buy a Home?

Over the past year or so, a lot of people have been talking about how tough it is to buy a home. And while there’s no arguing affordability is still tight, there are signs it’s starting to get a bit better and may improve even more throughout the year. Elijah de la Campa, Senior Economist at Redfin, says:

“We’re slowly climbing our way out of an affordability hole, but we have a long way to go. Rates have come down from their peak and are expected to fall again by the end of the year, which should make homebuying a little more affordable and incentivize buyers to come off the sidelines.”

Here’s a look at the latest data for the three biggest factors that affect home affordability: mortgage rates, home prices, and wages.

1. Mortgage Rates

Mortgage rates have been volatile this year – bouncing around in the upper 6% to low 7% range. That’s still quite a bit higher than where they were a couple of years ago. But there is a sliver of good news.

Despite the recent volatility, rates are still lower than they were last fall when they reached nearly 8%. On top of that, most experts still think they’ll come down some over the course of the year. A recent article from Bright MLS explains:

“Expect rates to come down in the second half of 2024 but remain above 6% this year. Even a modest drop in rates will bring both more buyers and more sellers into the market.”

Any drop in rates can make a difference for you. When rates go down, you can afford the home you really want more easily because your monthly payment would be lower.

2. Home Prices

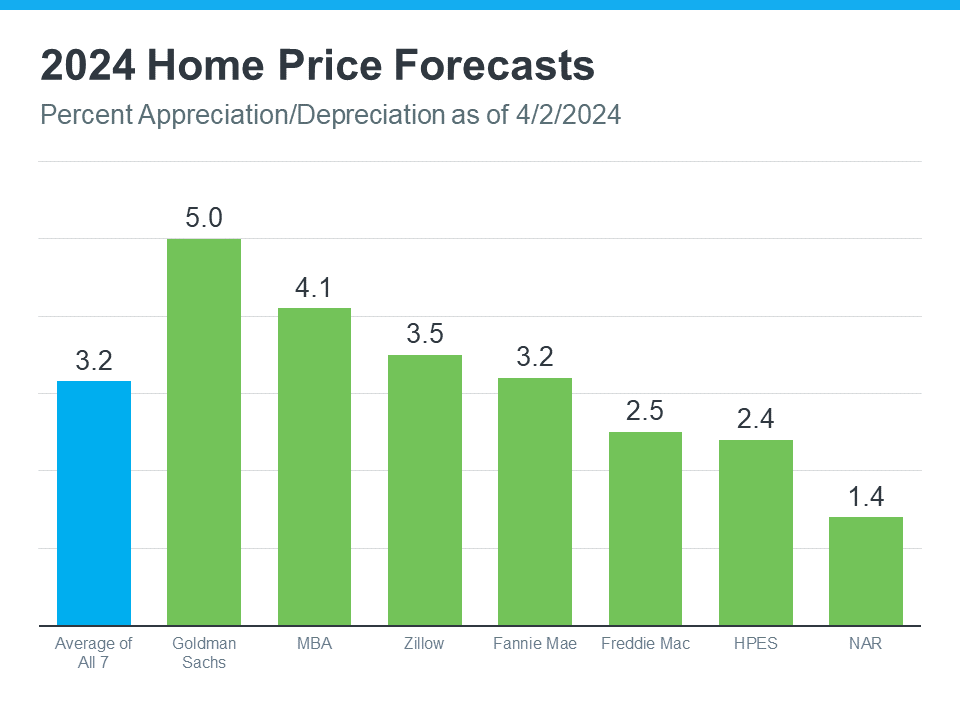

The second big factor to think about is home prices. Most experts project they’ll keep going up this year, but at a more normal pace. That’s because there are more homes on the market this year, but still not enough for everyone who wants to buy one. The graph below shows the latest 2024 home price forecasts from seven different organizations:

These forecasts are actually good news for you because it means the prices aren’t likely to shoot up sky high like they did during the pandemic. That doesn’t mean they’re going to fall – they’ll just rise at a slower pace.

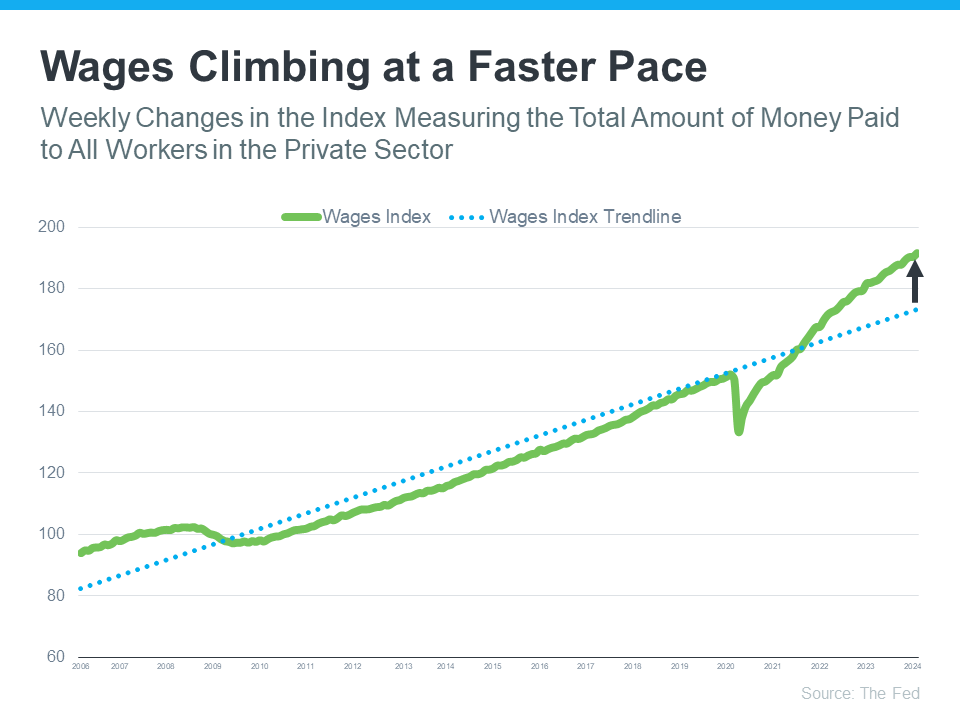

3. Wages

One factor helping affordability right now is the fact that wages are rising. The graph below uses data from the Federal Reserve to show how wages have been growing over time:

Check out the blue dotted line. That shows how wages typically rise. If you look at the right side of the graph, you’ll see wages are climbing even faster than normal right now.

Here’s how this helps you. If your income has increased, it’s easier to afford a home because you don’t have to spend as big of a percentage of your paycheck on your monthly mortgage payment.

Bottom Line

If you stack these factors up, you’ll see mortgage rates are still projected to come down a bit later this year, home prices are going up at a more moderate pace, and wages are growing quicker than normal. Those trends are a good sign for your ability to afford a home.

Is It Better To Rent Than Buy a Home Right Now?

You may have seen reports in the news recently saying it’s more affordable to rent right now than it is to buy a home. And while that may be true in some markets if you just look at typical monthly payments, there’s one thing that the numbers aren’t factoring in: and that’s home equity. Here’s a look at how big of an impact equity can have and why it’s worth considering as you make your decision.

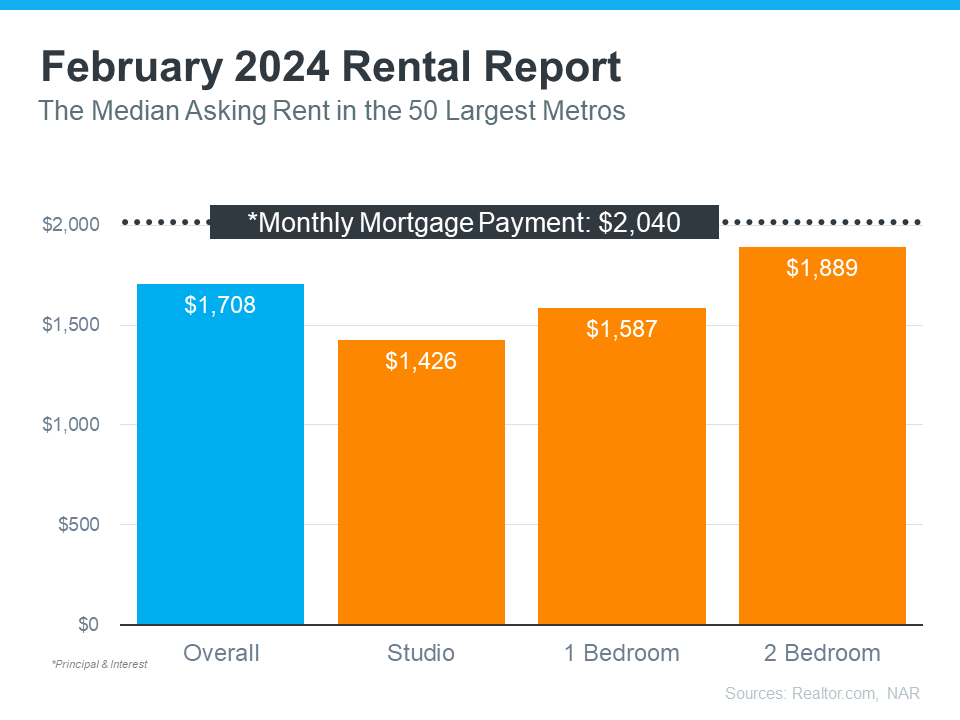

What the Headlines Are Based on

The graph below uses national data on the median rental payment from Realtor.com and median mortgage payment from the National Association of Realtors (NAR) to compare the two options. As the graph shows, especially if you’re not looking for a lot of space, it can be more affordable on a monthly basis to rent:

But if you’re looking for something with 2 bedrooms, the gap between the median rent and the median mortgage payment starts to shrink to a difference that may be more doable. The median monthly mortgage payment is $2,040. The median monthly rent for 2 bedrooms is $1,889. That’s a difference of about $151 a month. But here’s what happens when you factor in equity too.

How Equity Changes the Game

If you rent, your monthly rental payments only go toward covering your housing costs and your landlord’s expenses. So other than saving a bit more per month and maybe getting your rental deposit back when you move, the money you spent on housing each month is gone – forever.

When you buy, your monthly mortgage payment pays for your shelter, but it also acts as an investment. That investment grows in the form of equity as you make your mortgage payment each month and chip away at what you owe on your home loan. Your equity gets an extra boost as home values climb – which they typically do.

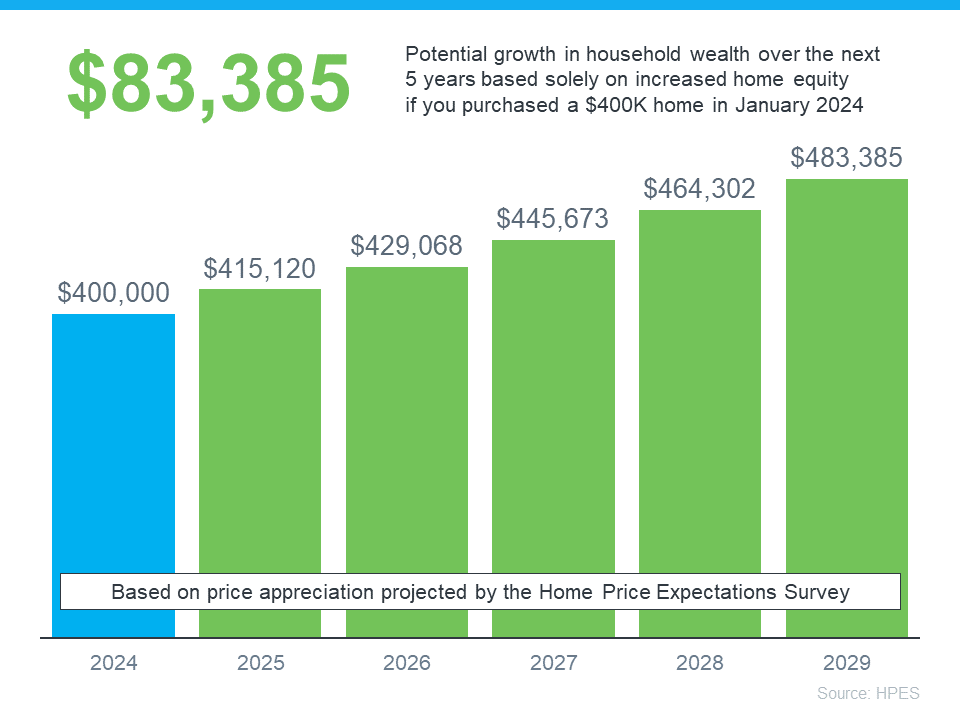

To give you a clearer idea of how equity can really stack up fast, here’s some data for you. Each quarter, Fannie Mae and Pulsenomics publish the results of the Home Price Expectations Survey (HPES). It asks more than 100 economists, real estate professionals, and investment and market strategists what they think will happen with home prices. In the latest release, those experts say home prices are going to keep going up over the next five years.

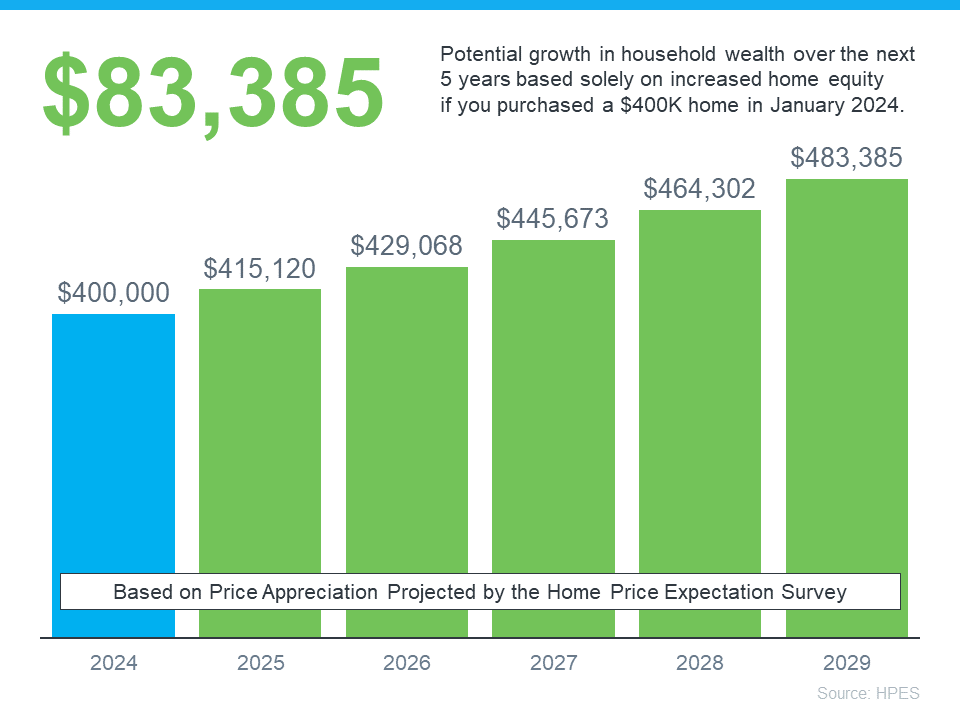

Here’s an example of how equity builds based on the projections from the HPES (see graph below):

Imagine you purchased a home for $400,000 at the start of this year. Chances are, since you bought, you plan to stay put for a while. Based on the HPES projections, if you live there for 5 years, you could end up gaining over $83,000 in household wealth as your home grows in value.

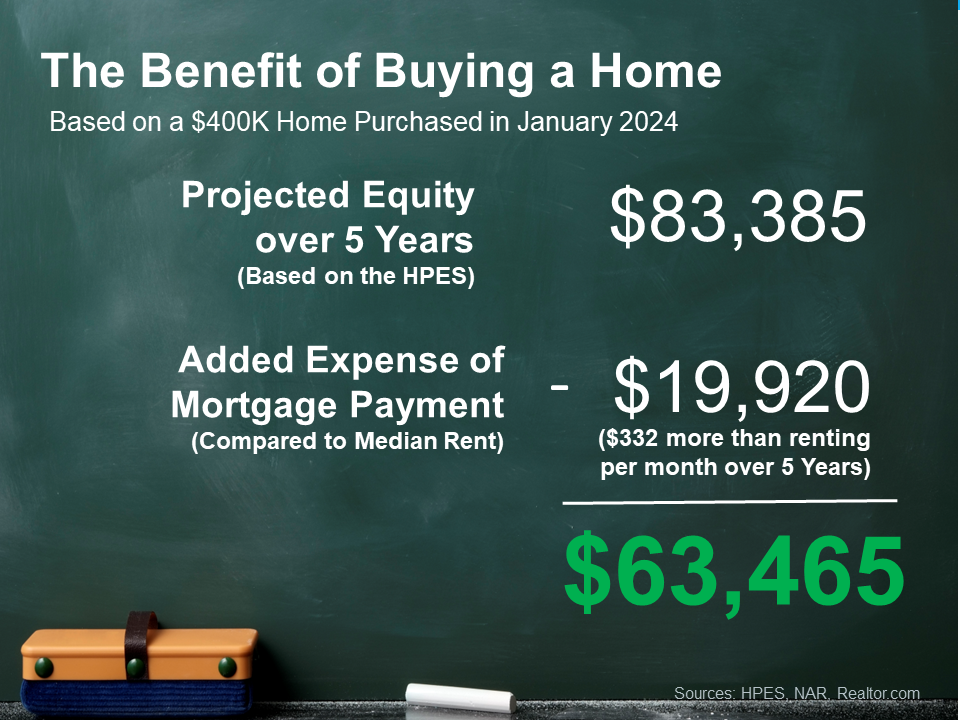

Here’s how that stacks up compared to renting, using the overall median rent from above:

While you may save a bit on your monthly payments if you rent right now, you’ll also miss out on gaining equity.

So, what’s the big takeaway? Whether it makes more sense to rent or buy is going to vary based on your personal finances. It’s not a good idea to buy if the numbers truly don’t work for you. But, if you’re ready and able, adding equity as the final puzzle piece may be enough to help you realize buying is a better move in the long run.

Bottom Line

When it comes down to it, buying a home gives you a benefit renting just can’t provide – and that’s the chance to gain equity. If you want to take advantage of long-term home price appreciation, let’s go over your options.

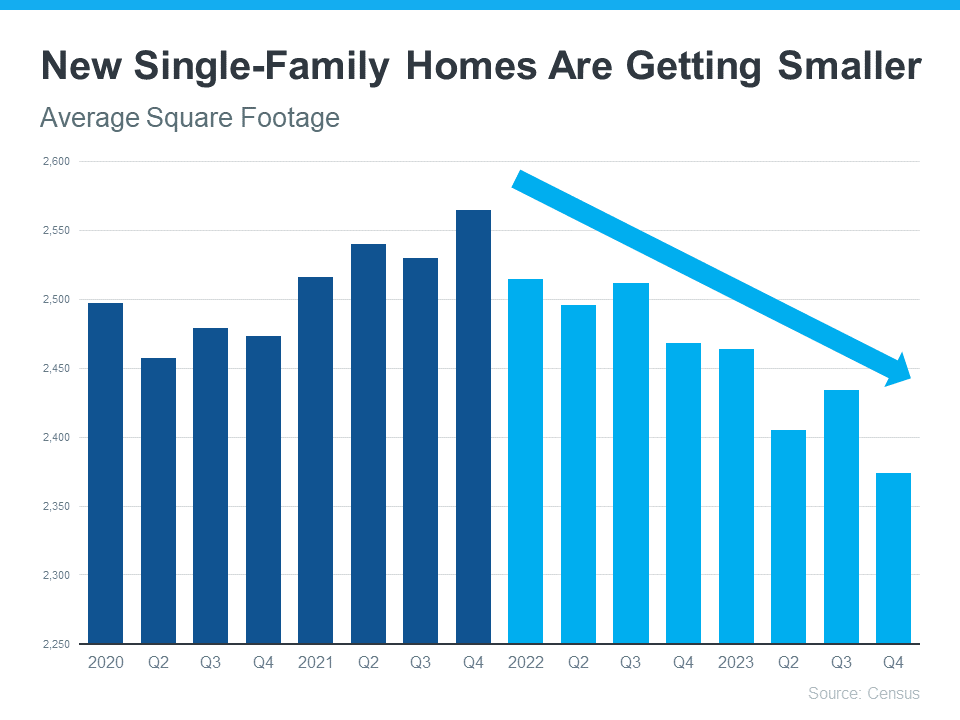

Builders Are Building Smaller Homes

There’s no arguing it, affordability is still tight. And if you’re trying to buy a home, that may mean you need to look at smaller houses to find one that’s still in your budget. But there is a silver lining: builders are focused on building these smaller homes right now and they’re offering incentives. And that can help give you more options that fit the bill.

Newly Built Homes Are Trending Smaller

During the pandemic, homebuyers wanted (and could afford) larger homes – and builders delivered. They focused on homes that were bigger, so people had more space for things like working from home, having a home gym, bonus rooms for virtual school, and more.

But with the affordability challenges buyers are facing today, builders are increasingly shifting their attention to bringing smaller single-family homes to the market. The graph below uses data from the Census to show how this trend has evolved over the last few years:

So, why the shift to less square footage? It’s simple. Builders want to build what they know will sell. Basically, they focus on where the demand is strongest. And once mortgage rates started climbing and consumers felt the challenges of affordability creeping in, it became clear there was (and is) a very real need for smaller homes. As the National Association of Home Builders (NAHB) explains:

“After a brief increase during the post-covid building boom, home size is trending lower and will likely continue to do so as housing affordability remains constrained.”

A recent article in the Real Deal says this about how this helps buyers:

“Even a slightly smaller home can be thousands of dollars cheaper — for both builders and buyers. . . In response to affordability challenges, major homebuilders are shifting priorities away from the big ticket homes and towards the cheaper set.”

What This Means for You

If you’re having a hard time finding something in your budget, it may help to look at smaller homes. And, if you consider new builds specifically, you may find a few other fringe benefits that can help on the affordability front – like price reductions or mortgage rate buy-downs. As NAHB says:

“More than one-third of builders cut home prices in 2023. NAHB expects builders to continue offering smaller homes and more affordable designs as housing affordability remains a barrier to homeownership.”

As Charlie Bilello, Chief Market Strategist, at Creative Planning, explains:

“Homebuilders are adapting to the lowest affordability on record by building smaller homes and offering more incentives/price cuts. The median square footage of a new single-family home in the US has moved down to its lowest level since 2010.”

If you explore these options, you’ll also get brand new everything, enjoy a house with fewer maintenance needs, and some of the latest features available. That’s worth looking into, right?

Bottom Line

Builders building smaller homes can give you more affordable options at a time when you may really need it. If you’re hoping to buy a home soon, let’s connect to look at what’s available in our area.

Newly Built Homes Could Be a Game Changer This Spring

Buying a home this spring? You’re probably navigating today’s affordability challenges and dealing with the limited number of homes for sale. But, what if there was a solution that could help with both?

If you’re having a hard time finding a home you love, and mortgage rates are putting pressure on your budget, it may be time to look at newly built homes. Here’s why.

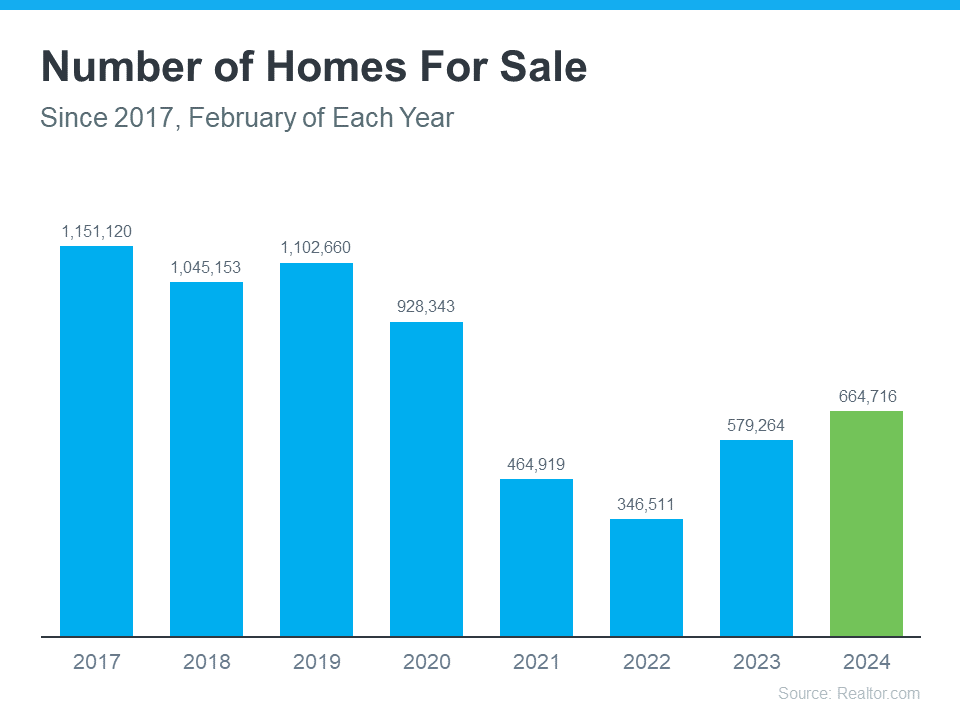

New Home Construction Is an Inventory Bright Spot

When looking for a home, you can choose between existing homes (those that are already built and previously owned) and newly constructed ones. While the number of existing homes for sale has increased this year, there are still fewer available than there were in more typical years in the housing market, like back in 2018 or 2019.

So, if you’re looking to expand your pool of options even more, turning to newly built homes can help. As Danielle Hale, Chief Economist at Realtor.com, explains:

“The shortage of existing homes For Sale has opened up the possibility of new-home construction to more buyers who may not have once considered it.”

And the good news is, there are more newly built homes to pick from right now. The graphs below use data from the Census to show how new home construction is ramping up in two key areas (see most recent spike in green):

Starts, or homes where builders just broke ground, have seen a big increase lately. And completions, homes that builders just finished, are also up significantly. So, if you want a new, move-in ready home or you want to get in early and customize your build along the way, you have more options right now.

Builders Are Offering Incentives To Help with Affordability

And to sweeten the pot, builders are offering things like mortgage rate buy-downs and other perks for homebuyers right now. This can help offset today’s affordability challenges while also getting you into your dream home. Mark Fleming, Chief Economist at First American, explains why you may find builders have more wiggle room to offer more for you than the typical homeowner:

“Builders aren’t rate locked-in. They would love to sell you the home because they’re not living in it. It costs money not to sell the home. And many of the public home builders have said in their earnings calls that they are not going to be pulling back on incentives, especially the mortgage rate buydown, so that will help the new-home market continue to perform well in the spring home-buying season.”

An article from HousingWire also says this about what builders are offering right now:

“. . . the use of sales incentives still shows some momentum as 60% of respondents reported using them, up from 58% in February. “

Just remember, buying from a builder is different from buying from a home seller, so it’s important to partner with a local real estate agent. Builder contracts can be complex. A trusted agent will be your advocate throughout the process.

They’ll be your go-to resource for advice on construction quality and builder reputation, reviewing and negotiating contracts to get you the best deal, helping you decide on which customizations and upgrades are most worthwhile, and a whole lot more.

Bottom Line

If you’re struggling to find a home to buy, or with today’s affordability challenges, let’s connect to see if newly built homes could be the solution you’re looking for.

Does It Make Sense To Buy a Home Right Now?

Thinking about buying a home? If so, you’re probably wondering: should I buy now or wait? Nobody can make that decision for you, but here’s some information that can help you decide.

What’s Next for Home Prices?

Each quarter, Fannie Mae and Pulsenomics publish the results of the Home Price Expectations Survey (HPES). It asks more than 100 experts—economists, real estate professionals, and investment and market strategists—what they think will happen with home prices.

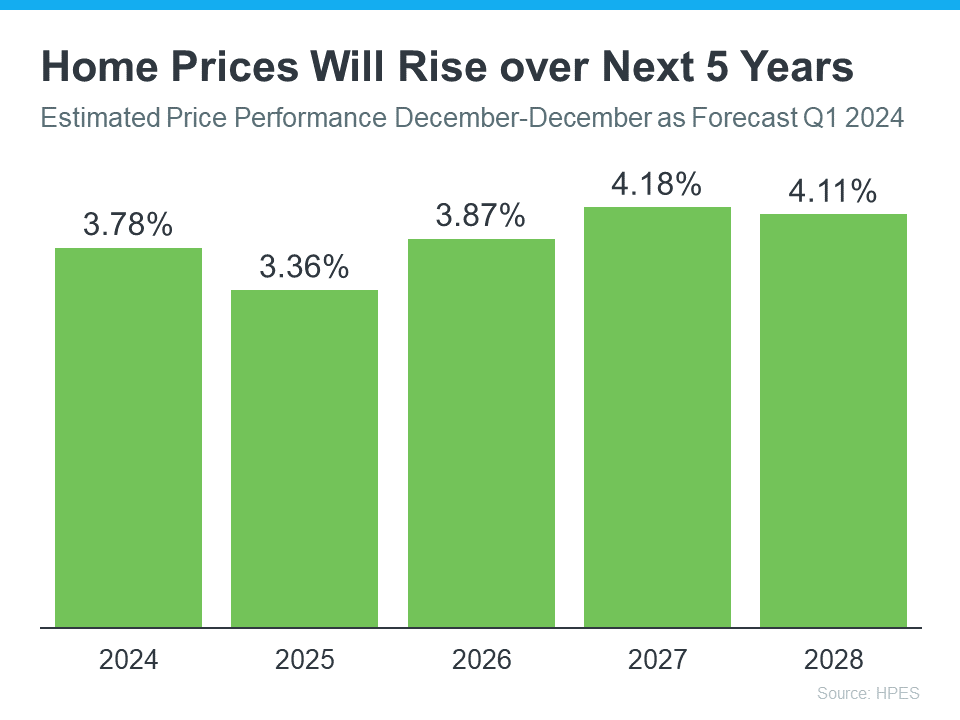

In the latest survey, those experts say home prices are going to keep going up for the next five years (see graph below):

Here’s what all the green on this chart should tell you. They’re not expecting any price declines. Instead, they’re saying we’ll see a 3-4% rise each year.

And even though home prices aren’t expected to climb by as much in 2025 as they are 2024, keep in mind these increases can really add up over time. It works like this. If these experts are right and your home’s value goes up by 3.78% this year, it’s set to grow another 3.36% next year. And another 3.87% the year after that.

What Does This Mean for You?

Knowing that prices are forecasted to keep going up should make you feel good about buying a home. That’s because it means your home is an asset that’s projected to grow in value in the years ahead.

If you’re not convinced yet, maybe these numbers will get your attention. They show how a typical home’s value could change over the next few years using expert projections from the HPES. Check out the graph below:

In this example, imagine you bought a home for $400,000 at the start of this year. Based on these projections, you could end up gaining over $83,000 in household wealth over the next five years as your home grows in value.

Of course, you could also wait – but if you do, buying a home is just going to end up costing you more.

Bottom Line

If you’re thinking it’s time to get your own place, and you’re ready and able to do so, buying now might make sense. Your home is expected to keep getting more valuable as prices go up. Let’s team up to start looking for your next home today.