Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Buying Beats Renting in 22 Major U.S. Cities

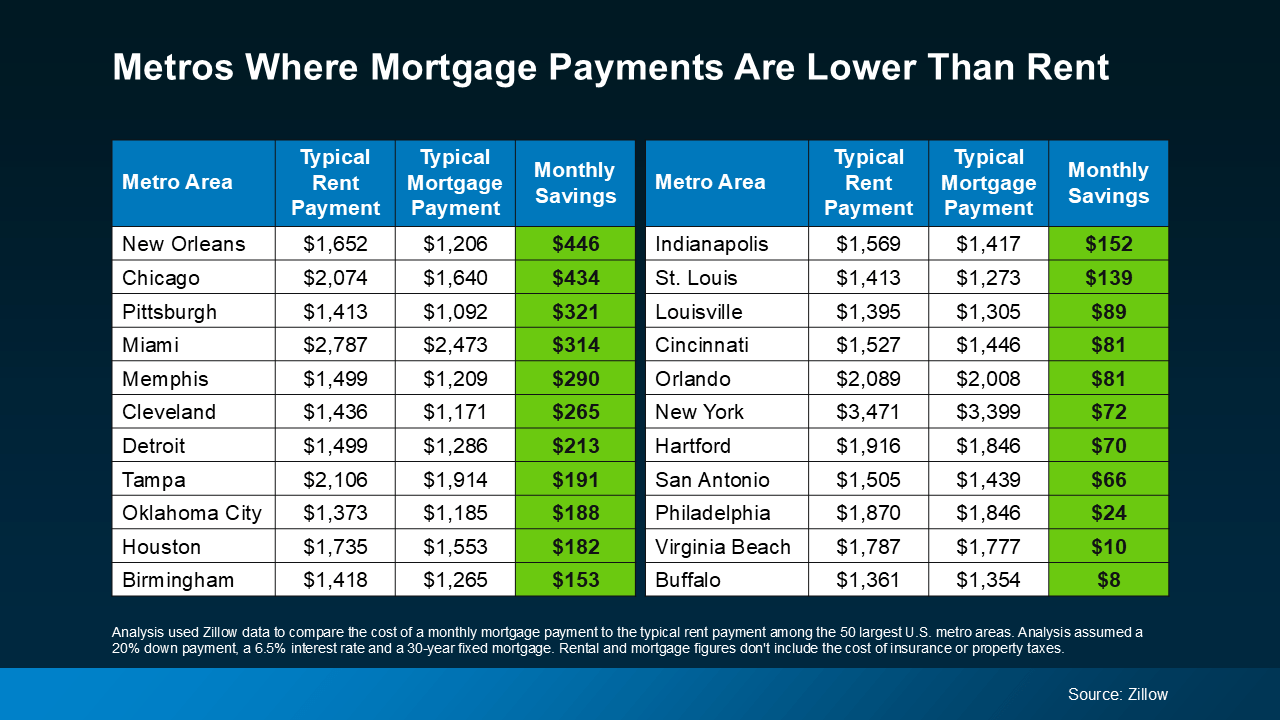

That’s right—according to a recent study from Zillow, in 22 of the 50 largest metro areas, monthly mortgage payments are now lower than rent payments (see chart below):

As mortgage rates have eased off their recent peak, home prices have moderated, and inventory has ticked up, affordability has improved significantly. When you add all of that up, it’s getting less expensive to buy a home than to rent one in many parts of the country.

As mortgage rates have eased off their recent peak, home prices have moderated, and inventory has ticked up, affordability has improved significantly. When you add all of that up, it’s getting less expensive to buy a home than to rent one in many parts of the country.

This is a big deal if you’ve been renting for a while now. But if you don’t see your city on this list, don’t sweat it. Things are moving fast, and your area might be joining these top metros soon.

You see, talking with a local real estate agent about what’s happening in your market before this happens in your ideal neighborhood could really change the game for you. It’s all about being informed by a true expert, and understanding what was out of reach before might actually be getting more affordable than you think.

Now, while this study compares monthly rent to principal and interest on a mortgage payment (not the whole monthly payment), let’s think through this. As Zillow notes, what you can’t ignore when you buy a home are things like taxes, insurance, utilities, and maintenance that should also be factored into your budget and your monthly payment.

But remember – renters pay extra fees too, like renters’ insurance, utilities, parking, and more. And while doing the math may feel like a drag, this equation could be a much more exciting one to work through today.

So, grab your calculator and your agent because the big takeaway is this: it may be time to determine if you’re in a spot to afford what you couldn’t just a few months ago.

As Orphe Divounguy, Senior Economist at Zillow, says:

“… for those who can make it work, homeownership may come with lower monthly costs and the ability to build long-term wealth in the form of home equity — something you lose out on as a renter. With mortgage rates dropping, it’s a great time to see how your affordability has changed and if it makes more sense to buy than rent.”

Whether you live in one of these budget-friendly metros where the scales have already tipped in your favor, or any town in-between, it’s time to connect with a local real estate agent to get the conversation started.

With mortgage rates coming down and more homes hitting the market, you’ll want to be ready to jump back into your search – before everyone else does.

Bottom Line

If you’re tired of renting and ready to find out what it takes to purchase a home in our area now that the landscape may be shifting, let’s do the math together to see if buying a home makes sense for you now or sometime soon.

Should You Sell Now? The Lifestyle Factors That Could Tip the Scale

Should You Sell Now? The Lifestyle Factors That Could Tip the Scale

Are you on the fence about whether to sell your house now or hold off? It’s a common dilemma, but here’s a key point to consider: your lifestyle might be the biggest factor in your decision. While financial aspects are important, sometimes the personal motivations for moving are reason enough to make the leap sooner rather than later.

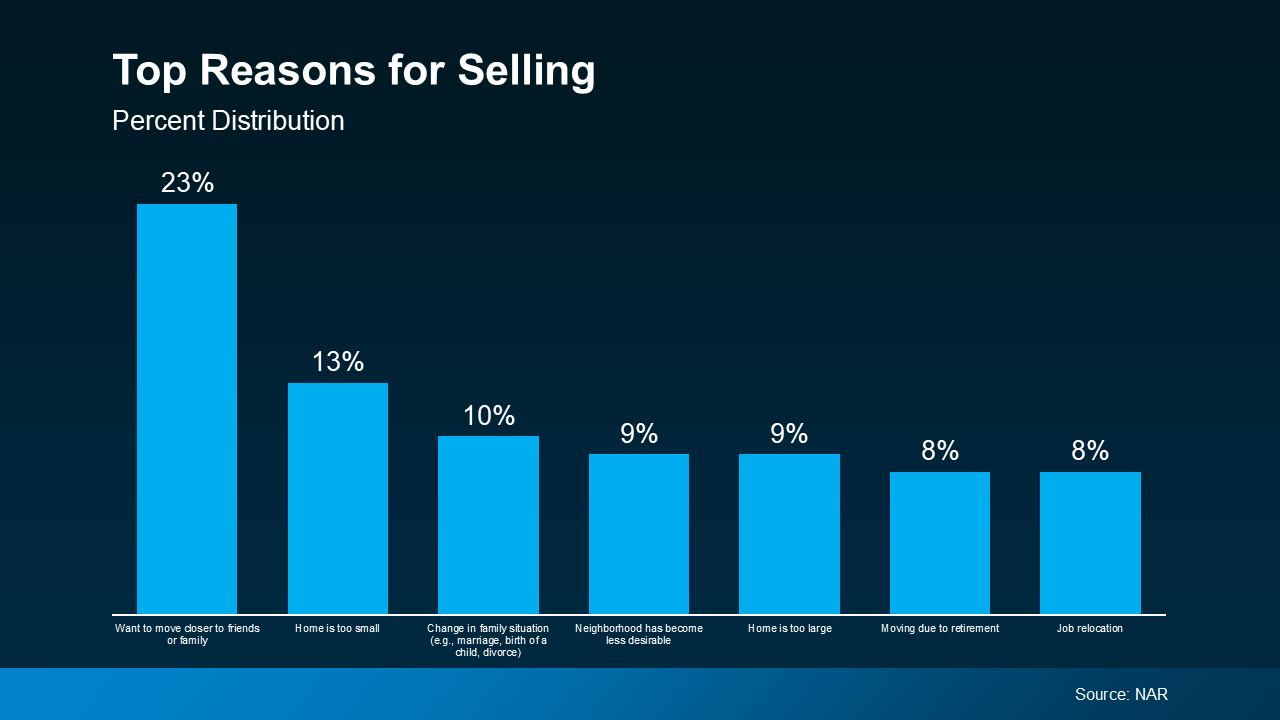

An annual report from the National Association of Realtors (NAR) offers insight into why homeowners like you chose to sell. All of the top reasons are related to life changes. As the graph below highlights:

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

If you, like the homeowners in this report, find yourself needing features, space, or amenities your current home just can’t provide, it may be time to consider talking to a real estate agent about selling your house. Your needs matter. That agent will walk you through your options and what you can expect from today’s market, so you can make a confident decision based on what matters most to you and your loved ones.

Your agent will also be able to help you understand how much equity you have and how it can make moving to meet your changing needs that much easier. As Danielle Hale, Chief Economist at Realtor.com, explains:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

Bottom Line

Your lifestyle needs may be enough to motivate you to make a change. If you want help weighing the pros and cons of selling your house, let’s have a conversation.

Homeownership: The Heart of the American Dream

Everyone’s vision for the future is personal and unique. But for many, common goals include success, freedom, and prosperity — values closely tied to having your own home and the iconic feeling of achieving the American Dream.

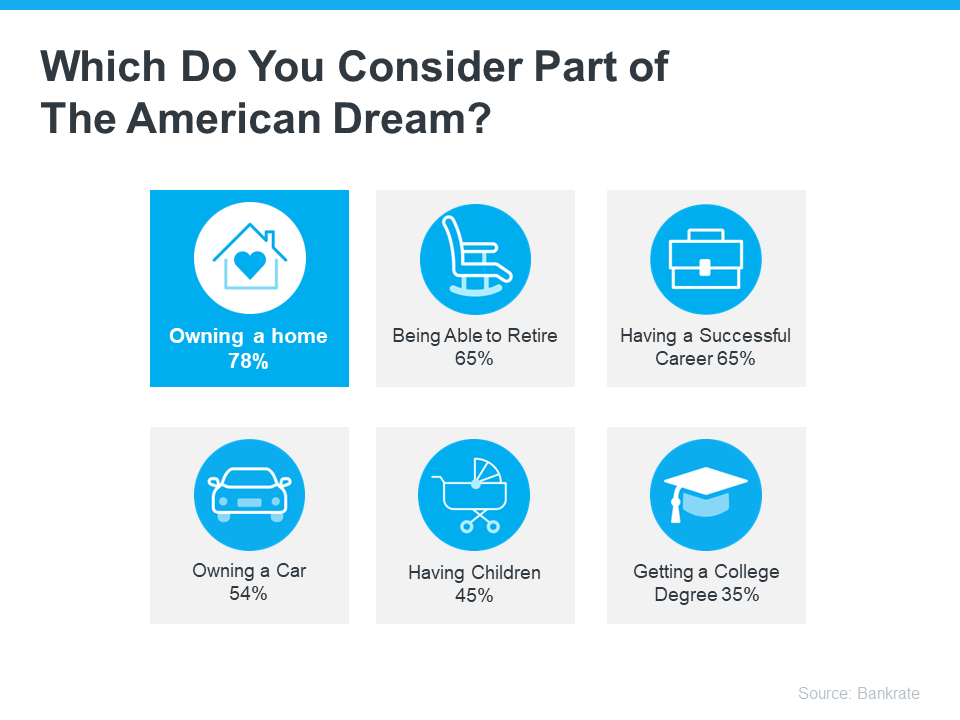

A recent survey by Bankrate reveals exactly that: homeownership is still a part of the American Dream. The results show, at 78%, that owning a home tops the list, surpassing other significant milestones such as retirement, having a successful career, and more (see below):

So, why is buying a home important to so many today? One reason is the financial and physical security it provides. Many people see homeownership as a way to reduce stress because owning a home with a fixed-rate mortgage stabilizes what is likely their largest monthly expense.

Another factor is the potential for building wealth. That’s because, over time, homeowners gain equity as they pay down their mortgage and as home prices appreciate, leading to longer-term financial stability.

But what about the responsibilities that come with owning and maintaining a home? According to a survey by Entrata, only 23% of renters feel homeownership is too much work, indicating the majority are open to the commitments and obligations that come with being a homeowner.

What Does This Mean for You?

While buying a home today might seem daunting due to higher mortgage rates and rising home prices, the long-term benefits can make it worthwhile. If you’re considering homeownership, remember that it’s more than just a financial investment — it’s a step toward securing your future.

Bottom Line

Owning a home is a significant and powerful decision that represents a big part of the American Dream. If you’re ready to take this step, let’s connect so you have someone who can guide you through the process and help you make your homeownership goals a reality.

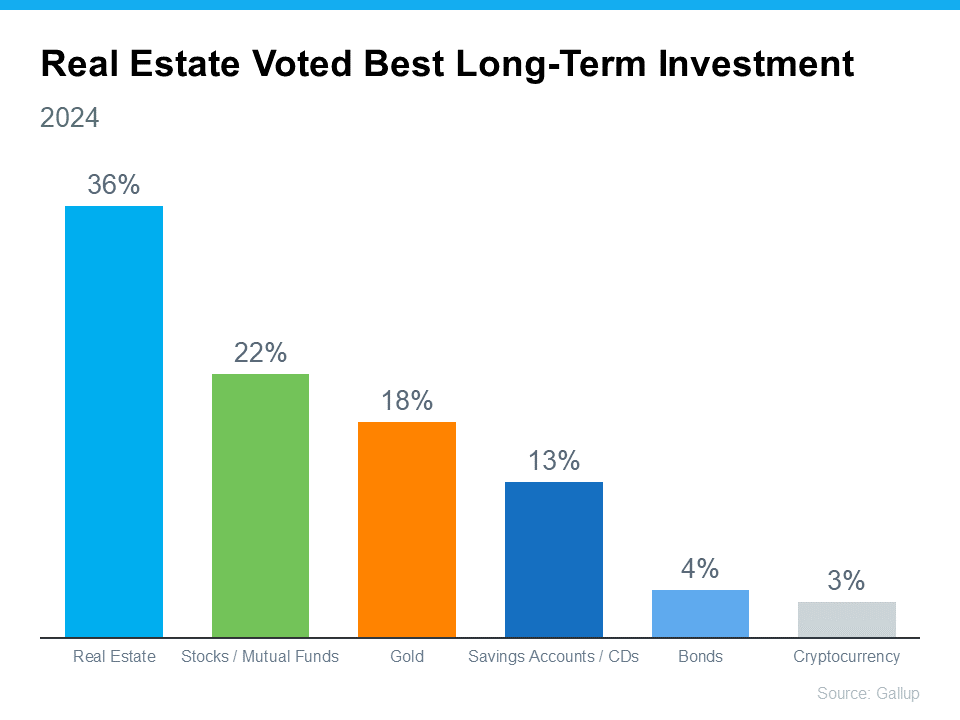

Real Estate Still Holds the Title of Best Long-Term Investment

With all the headlines circulating about home prices and mortgage rates, you may be asking yourself if it still makes sense to buy a home right now, or if it’s better to keep renting. Here’s some information that could help put your mind at ease by showing that investing in a home is still a powerful decision.

According to the experts at Gallup, real estate has been crowned the top long-term investment for a whopping 12 years in a row. It has consistently beat out other investment types like gold, stocks, and bonds. Just take a look at the graph below – it speaks volumes:

But why does real estate continue to reign supreme as a top-notch long-term investment? It’s because, even today, buying a home can be your golden ticket to building wealth over time.

Unlike other investments that can feel a bit like riding a rollercoaster with all the ups and downs and ongoing risk factors, real estate follows a more predictable and positive pattern.

History shows home values usually rise. And while prices may vary by market, that means as time goes by, your house is likely to appreciate in value. And that helps you grow your net worth in a big way. As an article from Realtor.com explains:

“Homeownership has long been tied to building wealth—and for good reason. Instead of throwing rent money out the window each month, owning a home allows you to build home equity. And over time, equity can turn your mortgage debt into a sizeable asset.”

So, if you’re on the fence about whether to rent or buy, remember that real estate was consistently voted the best long-term investment for a reason. And if you want to get in on that action, it may make sense to go ahead and buy (if you’re ready and able).

Bottom Line

When it comes to building wealth that stands the test of time, real estate is the name of the game. If you’re ready to start on your own journey toward homeownership, let’s connect today.

Your Equity Could Make a Move Possible

Many homeowners looking to sell feel like they’re stuck between a rock and a hard place right now. Today’s mortgage rates are higher than the one they currently have on their home, and that’s making it harder to want to sell and make a move. Maybe you’re in the same boat.

But what if there was a way to offset these higher borrowing costs? There is. And the money you need probably already exists in your current home in the form of equity.

What Is Equity?

Think of equity as a simple math equation. Freddie Mac explains:

“. . . your home’s equity is the difference between how much your home is worth and how much you owe on your mortgage.”

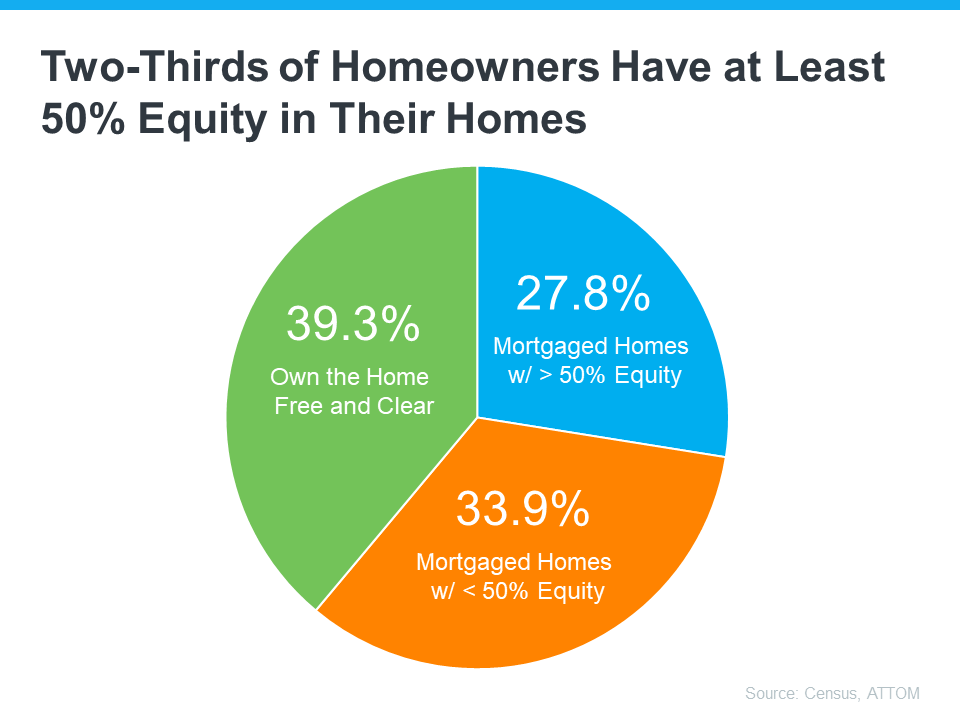

Your equity grows as you pay down your loan over time and as home prices climb. And thanks to the rapid home price appreciation we saw in recent years, you probably have a whole lot more of it than you realize.

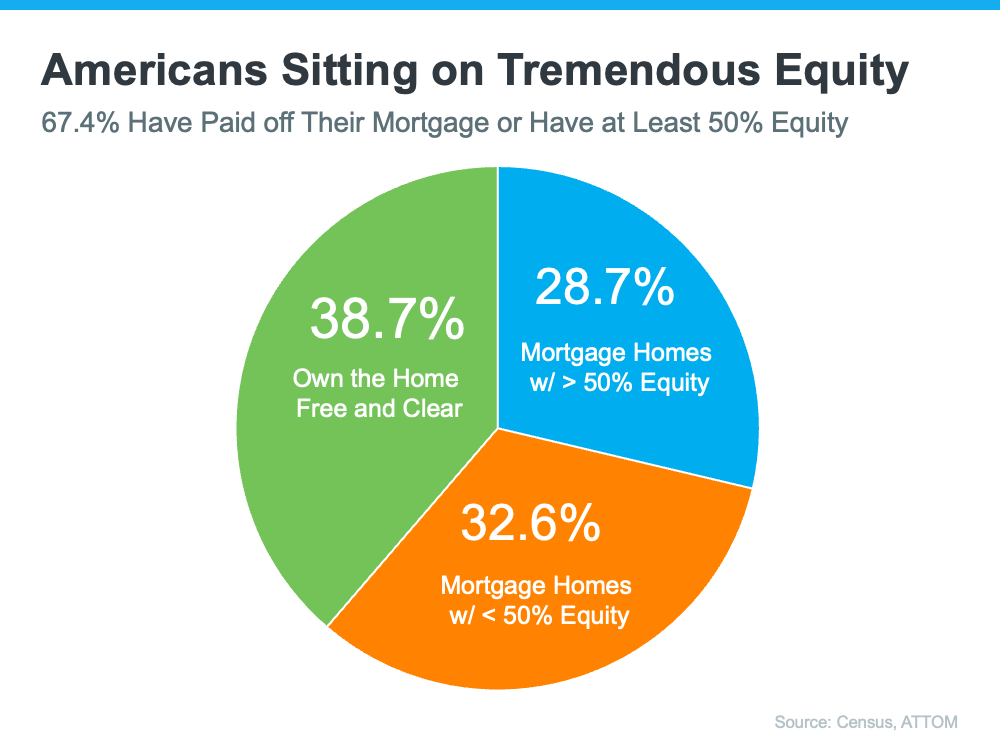

The latest from the Census and ATTOM shows more than two out of three homeowners have either completely paid off their mortgages (shown in green in the chart below) or have at least 50% equity (shown in blue in the chart below):

That means the majority of homeowners have a game-changing amount of equity right now.

How Your Equity Can Help Fuel Your Move

After you sell your house, that equity can help you move without worrying as much about today’s mortgage rates. As Danielle Hale, Chief Economist for Realtor.com says:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

To give you some examples, here are a few ways you can use equity to buy your next home:

- Be an all-cash buyer: If you’ve been living in your current home for a long time, you might have enough equity to buy your next home without having to take out a loan. If that’s the case, you won’t need to borrow any money or worry about mortgage rates.

- Make a larger down payment: Your equity could also be used toward your next down payment. It might even be enough to let you put a larger amount down, so you won’t have to borrow as much at today’s rates.

The First Step: Determine How Much Equity You Have in Your Home

Want to find out how much equity you have? To do that, you’ll need two things:

- The current mortgage balance on your home

- The current value of your home

You can probably find the mortgage balance on your monthly mortgage statement. To understand the current market value of your house, you can pay hundreds of dollars for an appraisal, or you can contact a local real estate agent who will be able to present to you, at no charge, a professional equity assessment report (PEAR).

Once you’ve connected with a trusted local agent and run the numbers, you’re one step closer to making a move you may not have thought was realistic – all thanks to your equity.

Bottom Line

If you want to find out how much equity you have and talk more about how it can make your next move possible, let’s connect.

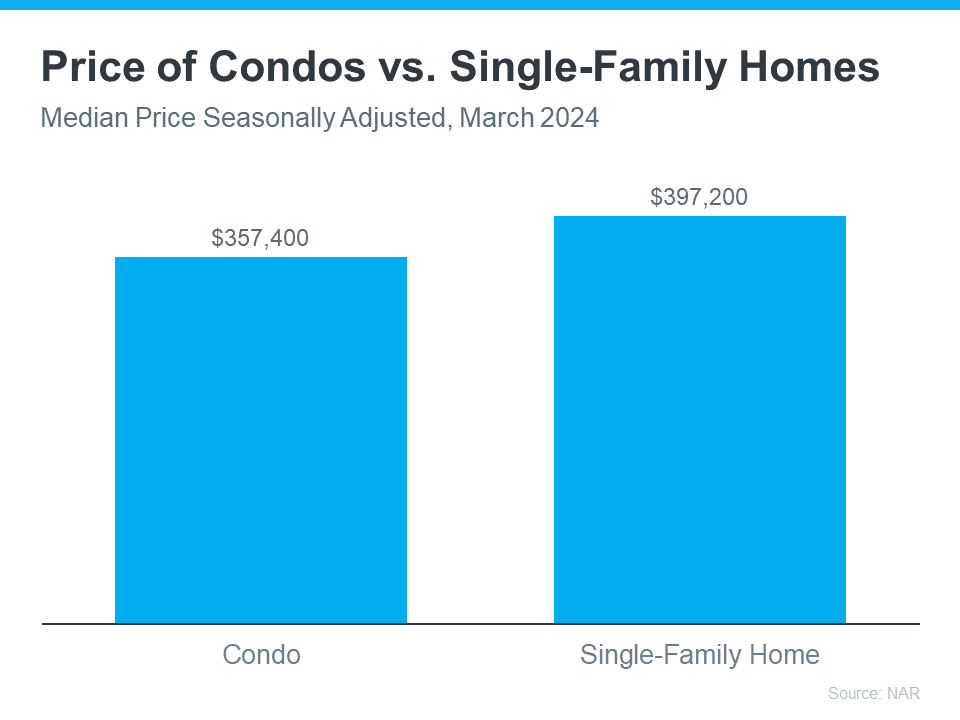

Why a Condo May Be a Great Option for Your First Home

Having a hard time finding a first home that’s right for you and your wallet? Well, here’s a tip – think about condominiums, or condos for short.

Having a hard time finding a first home that’s right for you and your wallet? Well, here’s a tip – think about condominiums, or condos for short.

They’re usually smaller than single-family homes, but that’s exactly why they can be easier on your budget. According to the latest data from the National Association of Realtors (NAR), condos are typically less expensive than single-family homes (see graph below):

So, if you’re comfortable with a smaller space and want to buy your first home this year, adding condos to your search might be easier on your wallet.

Besides giving you more options for your home search and maybe fitting your budget better, living in a condo has a bunch of other perks, too. According to Rocket Mortgage:

“From community living to walkable urban areas, condos are great options for first-time home buyers and people looking to enjoy homeownership without extensive upkeep.”

Let’s dive into a few of the draws of condos for first-time buyers from Bankrate:

- They require less maintenance. Condos are great if you want to own your place but don’t want to mow the lawn, shovel snow, or fix the roof. Your real estate agent can help explain any associated fees and details for the condos you’re interested in.

- They allow you to start building equity. When you buy a condo, you build equity and your net worth as you make your mortgage payments and as your condo’s value goes up over time.

- They often come with added amenities. Your condo might come with access to amenities like a pool, dog park, or parking. And the best part? You don’t have to take care of any of them.

- They provide you with a sense of community. Buying a condo means you’ll be living close to other people, which is nice if you enjoy having neighbors around and making friends. Many condo communities hold fun events like barbecues and parties during holidays for everyone to enjoy.

Remember, your first home doesn’t have to be the one you stay in forever. The important thing is to get your foot in the door as a homeowner so you can start to gain home equity. Later on, that equity can help you buy another place if you need something different.

Ultimately, owning and living in a condo is a lifestyle choice. And if it’s one that appeals to you, they could provide the added options you need in today’s market.

Bottom Line

It might be a good idea to think about condos in your home search. If you’re ready to see what’s out there, let’s get in touch today.

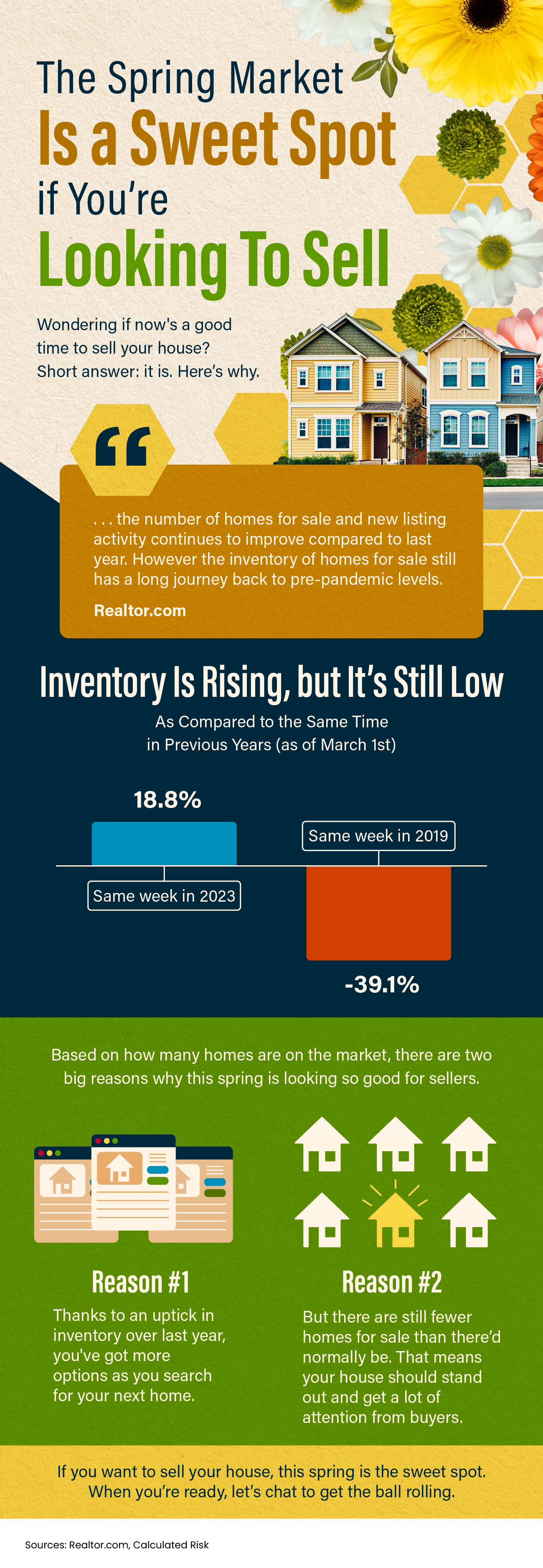

The Spring Market Is a Sweet Spot if You’re Looking To Sell

Some Highlights

- Wondering if now’s a good time to sell your house? Based on how many homes are on the market, there are two big reasons why this spring is looking so good for sellers.

- Thanks to an uptick in inventory over last year, you’ve got more options for your next home. But there are still fewer homes for sale than there’d normally be, meaning your house should stand out and get a lot of attention from buyers.

- If you want to sell your house, this spring is the sweet spot. When you’re ready, let’s chat to get the ball rolling.

The Benefits of Downsizing When You Retire

If you’re taking a look at your expenses as you retire, saving money where you can has a lot of appeal. One long-standing, popular way to do that is by downsizing to a smaller home.

When you think about cutting down on your spending, odds are you think of frequent purchases, like groceries and other goods. But when you downsize your house, you often end up downsizing the bills that come with it, like your mortgage payment, energy costs, and maintenance requirements. Realtor.com shares:

“A smaller home typically means lower bills and less upkeep. Then there’s the potential windfall that comes from selling your larger home and buying something smaller.”

That windfall is thanks to your home equity. If you’ve been in your house for a while, odds are you’ve built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Daniel Hunt, CFA at Morgan Stanley, explains:

“Home equity can be a significant source of wealth for retirees, often representing a large portion of their net worth. . . . Retirement planning can be complex, but your home equity shouldn’t be overlooked.”

And when you’re ready to use that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

What This Means for You

If you’re thinking about downsizing, ask yourself these questions:

- Do the original reasons I bought my current house still stand, or have my needs changed since then?

- Do I really need and want the space I have right now, or could somewhere smaller be a better fit?

- What are my housing expenses right now, and how much do I want to try to save by downsizing?

Then, meet with a real estate agent to get an answer to this one: What are my options in the market right now? A local real estate agent can walk you through how much equity you have in your house and how it positions you to win when you downsize.

Bottom Line

Want to save money in retirement? Consider downsizing – it could really help you out. When you’re ready, let’s connect about your goals in the housing market this year.

The Benefits of Downsizing When You Retire

If you’re taking a look at your expenses as you retire, saving money where you can has a lot of appeal. One long-standing, popular way to do that is by downsizing to a smaller home.

When you think about cutting down on your spending, odds are you think of frequent purchases, like groceries and other goods. But when you downsize your house, you often end up downsizing the bills that come with it, like your mortgage payment, energy costs, and maintenance requirements. Realtor.com shares:

“A smaller home typically means lower bills and less upkeep. Then there’s the potential windfall that comes from selling your larger home and buying something smaller.”

That windfall is thanks to your home equity. If you’ve been in your house for a while, odds are you’ve built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Daniel Hunt, CFA at Morgan Stanley, explains:

“Home equity can be a significant source of wealth for retirees, often representing a large portion of their net worth. . . . Retirement planning can be complex, but your home equity shouldn’t be overlooked.”

And when you’re ready to use that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

What This Means for You

If you’re thinking about downsizing, ask yourself these questions:

- Do the original reasons I bought my current house still stand, or have my needs changed since then?

- Do I really need and want the space I have right now, or could somewhere smaller be a better fit?

- What are my housing expenses right now, and how much do I want to try to save by downsizing?

Then, meet with a real estate agent to get an answer to this one: What are my options in the market right now? A local real estate agent can walk you through how much equity you have in your house and how it positions you to win when you downsize.

Bottom Line

Want to save money in retirement? Consider downsizing – it could really help you out. When you’re ready, let’s connect about your goals in the housing market this year.

Home Equity Can Be a Game Changer When You Sell

Are you on the fence about selling your house? While affordability is improving this year, it’s still tight. And that may be on your mind. But understanding your home equity could be the key to making your decision easier. An article from Bankrate explains:

“Home equity is the difference between your home’s value and the amount you still owe on your mortgage. It represents the paid-off portion of your home.

You’ll start off with a certain level of equity when you make your down payment to buy the home, then continue to build equity as you pay down your mortgage. You’ll also build equity over time as your home’s value increases.”

Think of equity as a simple math equation. It’s the value of your home now minus what you owe on your mortgage. And guess what? Recently, your equity has probably grown more than you think.

In the past few years, home prices skyrocketed, which means your home’s value – and your equity – likely shot up, too. So, you may have more equity than you realize.

How To Make the Most of Your Home Equity Right Now

If you’re thinking about moving, the equity you have in your home could be a big help. According to CoreLogic:

“. . . the average U.S. homeowner with a mortgage still has more than $300,000 in equity . . .”

Clearly, homeowners have a lot of equity right now. And the latest data from the Census and ATTOM shows over two-thirds of homeowners have either completely paid off their mortgages (shown in green in the chart below) or have at least 50% equity (shown in blue in the chart below):

That means roughly 70% have a tremendous amount of equity right now.

After you sell your house, you can use your equity to help you buy your next home. Here’s how:

- Be an all-cash buyer: If you’ve been living in your current home for a long time, you might have enough equity to buy your next home without having to take out a loan. If that’s the case, you won’t need to borrow any money or worry about mortgage rates. Investopedia states:

“You may want to pay cash for your home if you’re shopping in a competitive housing market, or if you’d like to save money on mortgage interest. It could help you close a deal and beat out other buyers.”

- Make a larger down payment: Your equity could also be used toward your next down payment. It might even be enough to let you put a larger amount down, so you won’t have to borrow as much money. The Mortgage Reports explains:

“Borrowers who put down more money typically receive better interest rates from lenders. This is due to the fact that a larger down payment lowers the lender’s risk because the borrower has more equity in the home from the beginning.”

The Easy Way To Find Out How Much Equity You Have

To find out how much equity you have in your home, ask a real estate agent you trust for a Professional Equity Assessment Report (PEAR).

Bottom Line

Planning a move? Your home equity can really help you out. Let’s connect to see how much equity you have and how it can help with your next home.