Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What Happens to Housing when There’s a Recession?

Since the 2008 housing bubble burst, the word recession strikes a stronger emotional chord than it ever did before. And while there’s some debate around whether we’re officially in a recession right now, the good news is experts say a recession today would likely be mild and the economy would rebound quickly. As the 2022 CEO Outlook from KPMG says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

To add to that sentiment, housing is typically one of the first sectors to rebound during a slowdown. As Ali Wolf, Chief Economist at Zonda, explains:

“Housing is traditionally one of the first sectors to slow as the economy shifts but is also one of the first to rebound.”

Part of that rebound is tied to what has historically happened to mortgage rates during recessions. Here’s a look back at rates during previous economic slowdowns to help put your mind at ease.

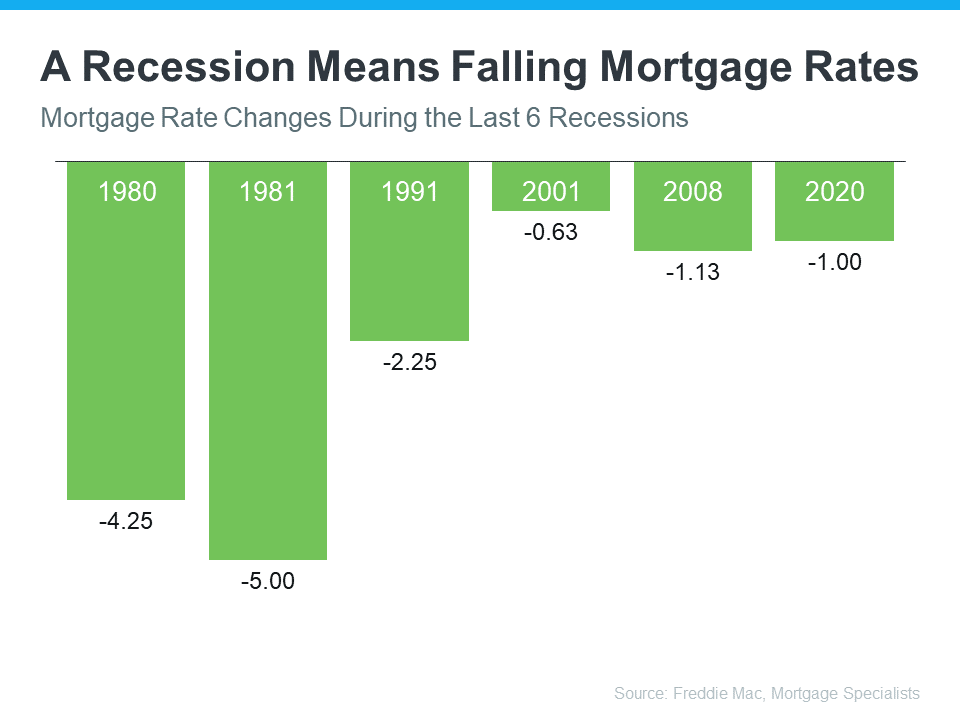

Mortgage Rates Typically Fall During Recessions

Historical data helps paint the picture of how a recession could impact the cost of financing a home. Looking at recessions in this country going all the way back to 1980, the graph below shows each time the economy slowed down mortgage rates decreased.

Fortune explains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

While history doesn’t always repeat itself, we can learn from and find comfort in the trends of what’s happened in the past. If you’re thinking about buying or selling a home, you can make the best decision by working with a trusted real estate professional. That way you have expert advice on what a recession could mean for the housing market.

Bottom Line

History shows you don’t need to fear the word recession when it comes to the housing market. If you have questions about what’s happening today, let’s connect so you have expert advice and insights you can trust.

Pre-Approval Is a Critical First Step on Your Homebuying Journey

If you’re planning to buy a home this year, one of the first steps on your journey is getting pre-approved. Especially in today’s market when mortgage rates are higher than they were just a few months ago, getting a mortgage pre-approval can be a game changer. Here’s why.

What Is Pre-Approval?

To better understand why pre-approval is key, it’s important to know what pre-approval is. The Mortgage Reports explains it like this:

“When you’re ready to take the leap into homeownership, your first step is mortgage preapproval. . . . A mortgage preapproval is when a lender determines you’re qualified for a home loan. Your preapproval letter shows the maximum loan amount you’re approved for (your home buying budget), as well as the specific interest rate and loan term you can expect.”

As part of the pre-approval process, a lender will look at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand your true price range and how much money you can borrow. That can make it easier when you set out to search for homes because you’ll know your overall numbers. And with mortgage rates rising and impacting affordability, a solid understanding of your numbers is even more important.

Pre-Approval Can Signal You’re a Serious Buyer

Another added benefit is that pre-approval lets the seller know you’re qualified to buy their house. A recent article from realtor.com notes:

“. . . getting pre-approved can actually improve your chances of falling into the sellers’ good graces, and you’ll want to get it done as early as you possibly can in the home-buying process.”

Even though bidding wars are easing this year as the market shifts, preapproval is still an important part of making a strong offer. It can help a seller feel more confident because it shows you’re serious about their home and that you’re a qualified buyer.

Bottom Line

Getting pre-approved for a mortgage is critical. It helps you better understand what you can borrow and shows sellers you’re serious about purchasing their home. Connect with a local real estate professional and a trusted lender so you have the tools you need to succeed as a homebuyer in today’s market.

Must-Have Tools for Homeowners

When you own your home, things are going to break and, unless you want to spend your money on visits from a neighborhood handyman, you’re going to need to fix them yourself. Luckily, you don’t need an arsenal of tools to handle most home maintenance fixes. These five tools will cover most of your basic projects.

- Cordless drill. A cordless drill is a must-have for installing cabinets, drawer pulls, hinges, picture frames, shelves and hooks, and more. Whether it’s for do-it-yourself projects or repairs, you’ll use your cordless drill just about every month.

- Drain cleaners. Shower and bathroom sink drains are susceptible to clogs because of the daily buildup of hair and whisker clippings. You can use chemical clog removers like Drano, but they’re expensive and the lingering chemical scent is unpleasant. Instead, buy some plastic drain cleaners that can reach into the drain to pull out the clog of hair and gunk. You can purchase them on Amazon or at a local hardware store for a low price.

- Shop-vac. No matter how careful you are, spills and accidents will happen and there are some tasks that just can’t be handled with paper towels or a standard vacuum, like pet messes or broken glass.

- Loppers. Even the minimum amount of care for your landscaping will require some loppers to remove damaged branches, vines, thick weeds, and any other unruly plants in your yard.

- Flashlight. You’re going to want something a little more powerful than your iPhone flashlight when you’re in the crawlspace!

Eye-Catching Ways to Decorate with Plants

Using plants as décor is a great way to add a little color and a natural, bright feel to any room. There are endless types of plants to choose from and various ways to display each one, but here are a few of our favorite combinations.

- Geometric pots. Find geometric pots or planters of various sizes and plant small succulents of different styles and colors in each one. Then group a few pots together on a windowsill or shelf or use them individually to adorn a side table or center of the dining room table.

- Long, hanging plants. Purchase a larger, draping plant-like eucalyptus, fern, or ivy and hang it from the ceiling using a macramé plant hanger or place it on a high shelf or ladder. These plants are perfect for the corner of your living room or room with a large, plain wall that is in need of a little pop of color.

- Plant corner. Have a large corner in the dining or living room and need ideas on how to fill it? Consider turning it into a small plant sanctuary. Select plants of all different sizes, heights, colors, and styles and purchase either matching pots or a mix of designs. Consider the use of a stool or small table to create additional levels and strategically place each one in the corner.

- Air plants. Air plants are universal and can be included in DIY wall art, hung from the ceiling or on the wall inside geometric metal prisms, or placed inside beautiful glass terrariums alongside other plants and colorful rocks or sand.

3 Questions You May Be Asking About Selling Your House Today

![3 Questions You May Be Asking About Selling Your House Today [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/10/20151852/3-questions-you-may-be-asking-about-selling-your-house-today-MEM-1046x2637.png)

Some Highlights

- If you’re planning to sell your house this year, you likely have questions about what the shift in the housing market means for your home sale.

- You might be wondering: Should I wait to sell? Are buyers still out there? And can I afford to buy my next home?

- Let’s connect so you can get answers to these questions and learn about the opportunities you still have in today’s housing market.

What’s Ahead for Home Prices?

As the housing market cools in response to the dramatic rise in mortgage rates, home price appreciation is cooling as well. And if you’re following along with headlines in the media, you’re probably seeing a wide range of opinions calling for everything from falling home prices to ongoing appreciation. But what’s true? What’s most likely to happen moving forward?

While opinions differ, the most likely outcome is we’ll fall somewhere in the middle of slight appreciation and slight depreciation. Here’s a look at the latest expert projections so you have the best information possible today.

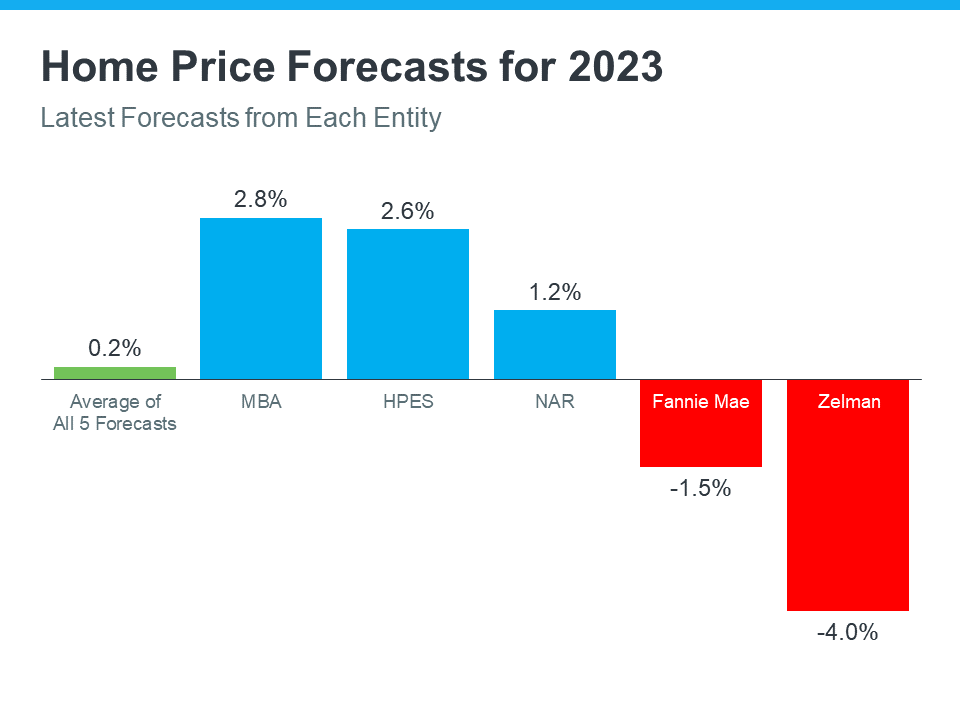

What the Experts Are Saying About Home Prices Next Year

The graph below shows the most up-to-date forecasts from five experts in the housing industry. These are the experts that have most recently updated their projections based on current market trends:

As the graph shows, the three blue bars represent experts calling for ongoing home price appreciation, just at a more moderate rate than recent years. The red bars on the graph are experts calling for home price depreciation.

While there isn’t a clear consensus, if you take the average (shown in green) of all five of these forecasts, the most likely outcome is, nationally, home price appreciation will be fairly flat next year.

What Does This Mean?

Basically, experts are divided on what’s ahead for 2023. Home prices will likely depreciate slightly in some markets and will continue to gain ground in others. It all depends on the conditions in your local market, like how overheated that market was in recent years, current inventory levels, buyer demand, and more.

The good news is home prices are expected to return to more normal levels of appreciation rather quickly. The latest forecast from Wells Fargo shows that, while they feel prices will fall in 2023, they think prices will recover and net positive in 2024. That forecast calls for 3.1% appreciation in 2024, which is a number much more in line with the long-term average of 4% annual appreciation.

And the Home Price Expectation Survey (HPES) from Pulsenomics, a poll of over one hundred industry experts, also calls for ongoing appreciation of roughly 2.6 to 4% from 2024-2026. This goes to show, even if prices decline slightly next year, it’s not expected to be a lasting trend.

As Jason Lewris, Co-Founder and Chief Data Officer for Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

Don’t let fear or uncertainty change your plans. If you’re unsure about where prices are headed or how to make sense of what’s going on in today’s housing market, reach out to a local real estate professional for the guidance you need each step of the way.

Bottom Line

The housing market is shifting, and it’s a confusing place right now. Let’s connect so you have a trusted real estate professional to help you make confident and informed decisions about what’s happening in our market.

Hidden Fees to Be Aware of When Purchasing a Home

Purchasing a home is arguably one of the biggest financial decisions you will make in your lifetime. As you start your hunt, don’t forget there will be other costs associated with your purchase then the price of the home. Here are 5 fees to keep in mind as you begin to budget.

- Home inspection. This is a crucial step in the home buying process. The findings that come from the inspection can help you negotiate price and repairs. Generally, you can expect to pay between $300 to $500 depending on the home and the location.

- Title services. Title services encompass the transfer of the title from the seller and a thorough search of the property’s records to ensure to no one will pop up with a claim to the property. Additionally, you may need to buy title insurance which will protect the lender or your investment in the home.

- Appraisal fee. Before getting a loan, you will likely be required to get an appraisal of the home to determine its estimated value. This will be conducted by a third-party company and the cost can land anywhere between $300 and $1,000, depending on the size of the home.

- HOA fees. Many communities have a homeowners’ association that enforces monthly fees. This money is used for general maintenance and updates to areas like pools, parks, and more. Typical HOA fees are around $200 per month.

- Taxes. The taxes each buyer pays at the closing table differ, but it is not uncommon for it to be up to two months’ worth of county and city property taxes. Additionally, there may be taxes for the transfer of the home title.

How to Get Ready for Retirement

For most people, retirement feels like a long way off. But, if you don’t start preparing as early as possible, you may find yourself in a place of financial insecurity when the time does come. To avoid this, consider implementing the following tips.

- Calculate your target savings. In general, it’s recommended that you save between 10 to 15 percent of your income for retirement. However, you can always use an online savings calculator to determine the amount you need to save for your specific needs and goals.

- Contribute to your employer’s retirement savings plan. Does your job offer a 401(k), traditional IRA, or Roth IRA? Sign up and start saving as soon as they allow you to. It’s recommended to set up automatic paycheck deductions and, once the money is in your retirement fund, don’t touch it.

- Take advantage of employee benefits. Many employers offer matching which generally requires you contribute a certain percentage of each paycheck and your company will then contribute a matching amount with funds of their own. They might also offer health savings or flexible savings account. By contributing to these accounts, you reduce your amount of taxable income, allowing you to save more money.

- Pay off your debts. Start by paying off any high-interest credit card debt first. Then look at other debts, such as student loans and car payments, and make a plan for paying those off incrementally.

- Reduce daily spending. Although this feels like a no-brainer, spending your money thoughtfully now can make a big impact later. Seek out areas of your life where you can

Should You Still Buy a Home with the Latest News About Inflation?

While the Federal Reserve is working hard to bring down inflation, the latest data shows the inflation rate is still high, remaining around 8%. This news impacted the stock market and added fuel to the fire for conversations about a recession.

You’re likely feeling the impact in your day-to-day life as you watch the cost of goods and services climb. The pinch it’s creating on your wallet and the looming economic uncertainty may leave you wondering: “should I still buy a home right now?” If that question is top of mind for you, here’s what you need to know.

Homeownership Is Historically a Great Hedge Against Inflation

In an inflationary economy, prices rise across the board. Historically, homeownership is a great hedge against those rising costs because you can lock in what’s likely your largest monthly payment (your mortgage) for the duration of your loan. That helps stabilize some of your monthly expenses. James Royal, Senior Wealth Management Reporter at Bankrate, explains:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

And with rents being as high as they are, the ability to stabilize your monthly payments and protect yourself from future rent hikes may be even more important. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains what happened to rents in the latest inflation report:

“Inflation refuses to budge. In September, consumer prices rose by 8.2%. Rents rose by 7.2%, the highest pace in 40 years.”

When you rent, your monthly payment is determined by your lease, which typically renews on an annual basis. With inflation high, your landlord may be more likely to increase your payments to offset the impact of inflation. That may be part of the reason why a survey from realtor.com shows 72% of landlords said they plan to raise the rent on one or more of their properties in the next year.

Becoming a homeowner, if you’re ready and able to do so, can provide lasting stability and a reliable shelter in times of economic uncertainty.

Bottom Line

The best hedge against inflation is a fixed housing cost. If you’re ready to learn more and start your journey to homeownership, let’s connect.

The Latest on Supply and Demand in Housing

Over the past two years, the substantial imbalance of low housing supply and high buyer demand pushed home sales and buyer competition to new heights. But this year, things are shifting as supply and demand reach an inflection point.

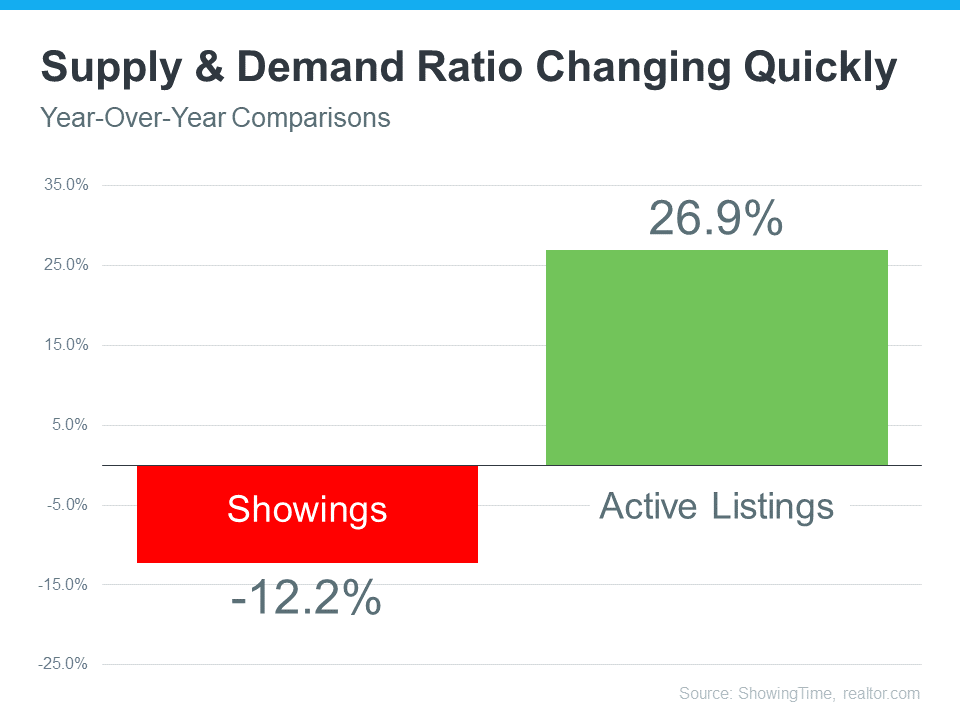

The graph below helps tell the story of just how different things are today.

This year, buyer demand has eased as higher mortgage rates and mounting economic uncertainty moderated the market. This slowdown in demand is clear when you look at the red bar on the graph. It uses the latest data from ShowingTime to illustrate how showings (an indicator of buyer demand) have softened by just over 12% compared to the same time last year.

Now for a look at how housing supply has changed, turn to the green bar. It uses data from realtor.com to show active listings are up nearly 27% compared to last year. That’s because the moderation of demand allowed housing inventory to increase in 2022.

What Does This Inflection Point Mean for Buyers?

If you’re thinking of buying a home, you’ll have less competition and more options than you would have had last year. Enjoy having more homes to choose from in your home search and lean on a trusted real estate professional to understand how the increase in supply has also increased your negotiation power. That professional can talk you through the opportunities and challenges buyers face in today’s shifting market. You may be surprised to find they’re different than they were a year ago.

What Does This Inflection Point Mean for Sellers?

If you’re looking to sell your house, know that inventory is still low overall. That means, if you work with an agent to price your house based on current market value, it will still sell despite the inventory gains and moderating buyer demand this year. That’s because there are still buyers out there who want to move, and your house may be exactly what they’re looking for.

Bottom Line

If you’re thinking of buying or selling a home, the best place to turn to for information on today’s supply and demand is a trusted real estate professional. Let’s connect so you know what’s happening in our local market and what that means for you.