Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What’s Behind Today’s Mortgage Rate Volatility?

If you’ve been keeping an eye on mortgage rates lately, you might feel like you’re on a roller coaster ride. One day rates are up; the next they dip down a bit. So, what’s driving this constant change? Let’s dive into just a few of the major reasons why we’re seeing so much volatility, and what it means for you.

The Market’s Reaction to the Election

A significant factor causing fluctuations in mortgage rates is the general reaction to the political landscape. Election seasons often bring uncertainty to financial markets, and this one is no different. Markets tend to respond not only to who won, but also to the economic policies they are expected to implement. And when it comes to what’s been happening with mortgage rates over the past couple of weeks, as the National Association of Home Builders (NAHB) says:

“. . . the primary reason interest rates have been on the rise pertains to the uncertainty surrounding the presidential election. Although the election is now complete, there continue to be growing concerns over budget deficits.”

In the short term, this anticipation has caused a slight uptick in mortgage rates as the markets adjust and react. Additionally, factors like international tensions, supply chain disruptions, and trade policies can drive investor sentiment, causing them to seek safer assets like bonds, which can indirectly impact mortgage rates. Essentially, the more global or domestic uncertainty, the greater the chance that mortgage rates may shift.

The Economy and the Federal Reserve

Inflation and unemployment are two other big drivers of mortgage rates. The Federal Reserve (the Fed) has been working to bring inflation under control, and has been closely monitoring the economy as they do. And as long as inflation continues to moderate and the job market shows signs of maximum employment, the Fed will continue its plans to cut the Federal Funds Rate.

Although the Fed doesn’t set mortgage rates, their decisions do have an impact, and typically a cut leads to a mortgage rates response. And in their November 6-7th meeting, the Fed had the data they needed to make another cut to the Federal Funds Rate. And while that decision was expected and much of the mortgage rate movement happened prior to that meeting, there was a slight dip in rates.

What To Expect in the Coming Months

As we look ahead, mortgage rates will respond to changes in the Fed’s policies and other economic indicators. The markets will likely remain in a wait-and-see mode, reacting to each new development. And, with the transition of a new administration comes an element of unpredictability. A recent article from The Mortgage Reports explains:

“Today’s economic indicators come with mixed pressures on mortgage rates and we’re likely to be in for a good amount of volatility as markets adjust and respond to the election . . .”

The best way to navigate this landscape is to have a team of real estate experts by your side. Professionals will help you understand what’s happening and can provide you with the guidance you need to make informed housing market decisions along the way.

Bottom Line

The takeaway? Today’s mortgage rate volatility is going to continue to be driven by economic factors and political changes.

Now is the time to lean on experienced professionals. A trusted real estate agent and mortgage lender can help you navigate through it. And with the right guidance, you can make informed decisions.

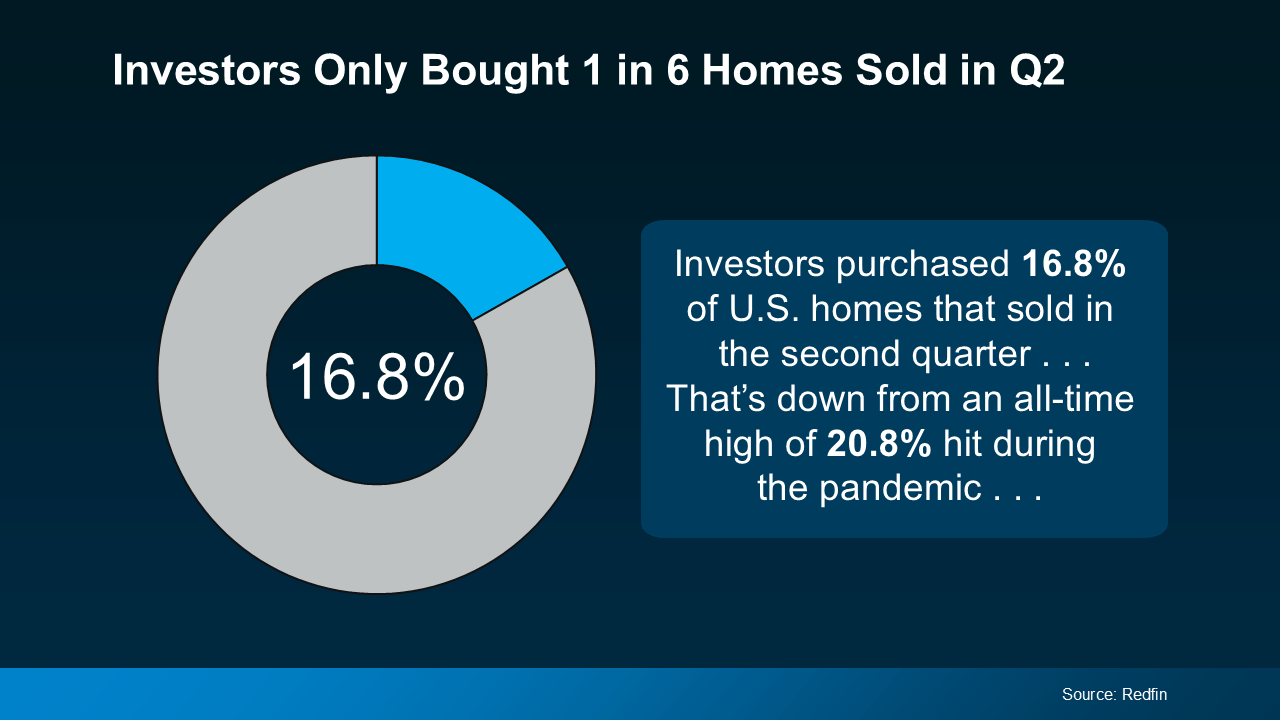

Is Wall Street Really Buying All the Homes?

Let’s be real – buying a home right now is tough. You’re scrolling through listings, rushing to open houses, and maybe even losing out to more competitive offers. Somewhere along the way, you might’ve heard the reason it’s so hard to find a home is because big Wall Street investors are swooping in and snatching up everything in sight.

But here’s the thing: that’s mostly a myth. While investors are part of the market, according to Redfin, they’re a relatively small part:

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.

So, before you get discouraged, let’s take a look at what’s really going on. You might be surprised to learn that Wall Street isn’t the competition you may think it is.

Most Investors Are Small Mom-and-Pops

Most investors aren’t the mega corporations you’ve probably heard about. In fact, many are your neighbors. A recent report from CoreLogic shows most investors are small, mom-and-pop types who own fewer than 10 properties. They aren’t massive companies with endless resources. Picture your neighbor who has another home they’re renting out or a vacation getaway.

Only about 1% of the market is owned by large, mega investors with thousands of properties. The majority are still owned by individuals and smaller investors – not the Wall Street giants.

Investor Purchases Are Declining

Not only are most investors small, but overall investor purchases have been on the decline. As the same report from CoreLogic says:

“Investors made 80,000 purchases in June 2024, compared with 112,000 in June 2023, and a nearly 50% percent drop from the high of 149,000 purchases in June 2021 . . .”

And what does this mean going forward? CoreLogic goes on to point out this downward trend is expected to continue into 2025.

So, if it seems like competition with investors is pushing you out of the market, it might help to know that investor activity is actually slowing down.

Bottom Line

The idea that Wall Street is buying up all the homes is largely a myth. Most investors are small ones, and the share of homes purchased by investors is declining – so you can take this one off your worry list.

If you have questions about the housing market, let’s talk.

Don’t Let These Two Concerns Hold You Back from Selling Your House

If you’re debating whether or not you want to sell right now, it might be because you’ve got some unanswered questions, like if moving really makes sense in today’s market. Maybe you’re wondering if it’s even a good idea to move right now. Or you’re stressed because you think you won’t find a house you like.

To put your mind at ease, here’s how to tackle these two concerns head-on.

Is It Even a Good Idea To Move Right Now?

If you own a home already, you may have been holding off because you don’t want to sell and take on a higher mortgage rate on your next house. But your move may be a lot more feasible than you think, and that’s because of your equity.

Equity is the current market value of your home minus what you still owe on your loan. And thanks to the rapid appreciation we saw over the past few years, your equity has gotten a big boost. Just how much are we talking about? See for yourself. As Dr. Selma Hepp, Chief Economist at CoreLogic, explains:

“Persistent home price growth has continued to fuel home equity gains for existing homeowners who now average about $315,000 in equity and almost $129,000 more than at the onset of the pandemic.”

Here’s why this can be such a game-changer when you sell. You can use that equity to put down a larger amount on your next home, which means financing less at today’s mortgage rate. And in some cases, you may even be able to buy your next home in cash, avoiding mortgage rates altogether.

The bottom line? Your equity could be the key to making your next move possible.

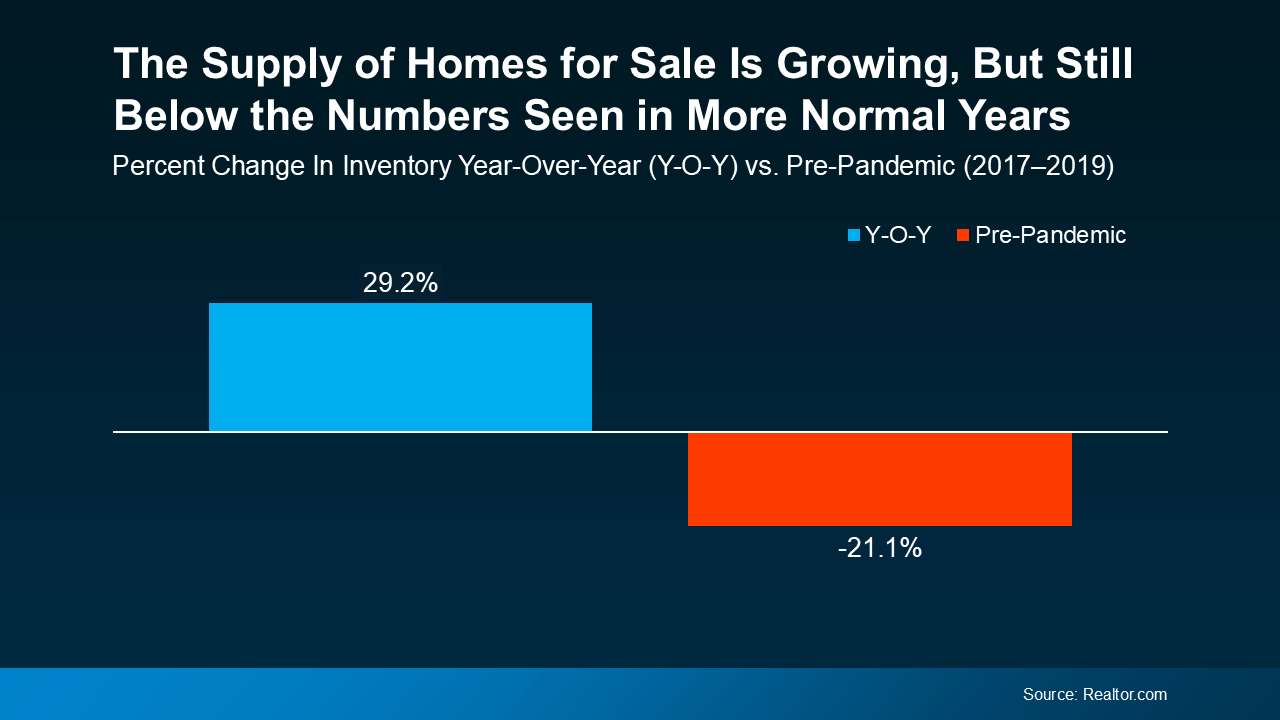

Will I Be Able To Find a Home I Like?

If this is on your mind, it’s probably because you remember just how low the supply of homes for sale got over the past few years. It felt nearly impossible to find a home to buy because there were so few available.

But finding a home in today’s market isn’t as challenging. That’s because the number of homes for sale is growing, giving you more options to choose from. Data from Realtor.com shows just how much inventory has increased – it’s up almost 30% year-over-year (see graph below):

And even though inventory is still below pre-pandemic levels, this is the highest it’s been in quite a while. That means you have more options for your move, but your house should still stand out to buyers at the same time. That’s a sweet spot for you.

And even though inventory is still below pre-pandemic levels, this is the highest it’s been in quite a while. That means you have more options for your move, but your house should still stand out to buyers at the same time. That’s a sweet spot for you.

It’s important to note, though, that this balance varies by local market. Some places may have more homes for sale than others, so working with a local real estate agent is the best way to see what inventory trends look like in your area.

Bottom Line

If you’re thinking about selling, hopefully these concerns haven’t kept you up at night. With this information, you should realize you don’t have to let the what-if’s delay your move anymore.

Let’s connect so you have the data and the local perspective you need to move forward.

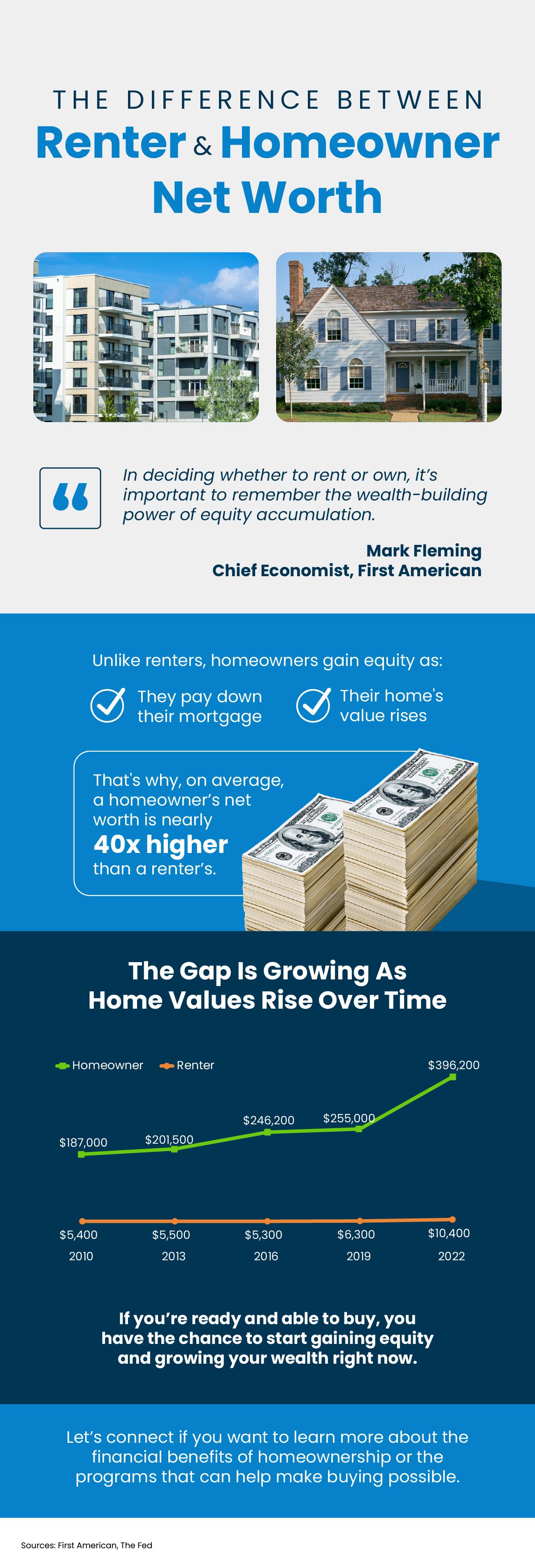

The Big Difference Between Renter and Homeowner Net Worth

Some Highlights

- If you’re torn between renting or buying, don’t forget to factor in the wealth-building power of homeownership.

- Unlike renters, homeowners gain equity as they pay their mortgage and as home values rise. That’s why, on average, a homeowner’s net worth is nearly 40x higher than a renter’s.

- Let’s connect if you want to learn more about the financial benefits of homeownership or the programs that can help make buying possible.

Should You Sell Your House or Rent It Out?

When you’re ready to move, figuring out what to do with your house is a big decision. And today, more homeowners are considering renting their home instead of selling it.

Recent data from Zillow shows about two-thirds (66%) of sellers thought about renting their home before listing, with nearly a third (28%) taking that possibility seriously. Compared to 2021, when fewer than half (47%) of homeowners considered renting before selling, it’s clear this trend is on the rise.

So, should you sell your house and use the money toward your next home or keep it as a rental to build long-term wealth? Let’s walk through some important questions to help you determine the right path for your financial and lifestyle goals.

Is Your House a Good Fit for Renting?

Before you decide what to do, it’s important to think about if it would make a good rental in the first place. For instance, if you’re moving far away, managing ongoing maintenance could become a major hassle. Other factors to consider are if your neighborhood is ideal for rentals and if your house needs significant repairs before it’s ready for tenants.

If any of these situations sound familiar, selling might be a more practical choice.

Are You Ready for the Realities of Being a Landlord?

Managing a rental property involves more than collecting monthly rent. It’s a commitment that can be time-consuming and challenging.

For example, you may get maintenance calls at all hours of the day or discover damage that needs to be repaired before a new tenant moves in. There’s also the risk of tenants missing payments or breaking their lease, which can add unexpected stress and financial strain. As Redfin notes:

“Landlords have to fix things like broken pipes, defunct HVAC systems, and structural damage, among other essential repairs. If you don’t have a few thousand dollars on hand to take care of these repairs, you could end up in a bind.”

Do You Understand the Costs?

If you’re considering renting primarily for passive income, remember, there are additional costs you should anticipate. As an article from Bankrate explains:

Mortgage and Property Taxes: You still need to pay these expenses, even if the rent doesn’t cover all of it.

Insurance: Landlord insurance typically costs about 25% more than regular home insurance, and it’s necessary to cover damages and injuries.

Maintenance and Repairs: Plan to spend at least 1% of the home’s value annually, more if the house is older.

Finding a Tenant: This involves advertising costs and potentially paying for background checks.

Vacancies: If the property sits empty between tenants, you’ll lose rental income and have to cover the cost of the mortgage until you find a new tenant.

Management and HOA Fees: A property manager can ease the burden, but typically charges about 10% of the rent. HOA fees are an additional cost too, if applicable.

Bottom Line

To sum it all up, selling or renting out your home is a personal decision. Let’s connect so you have a pro on your side to help you feel supported and informed as you make your decision.

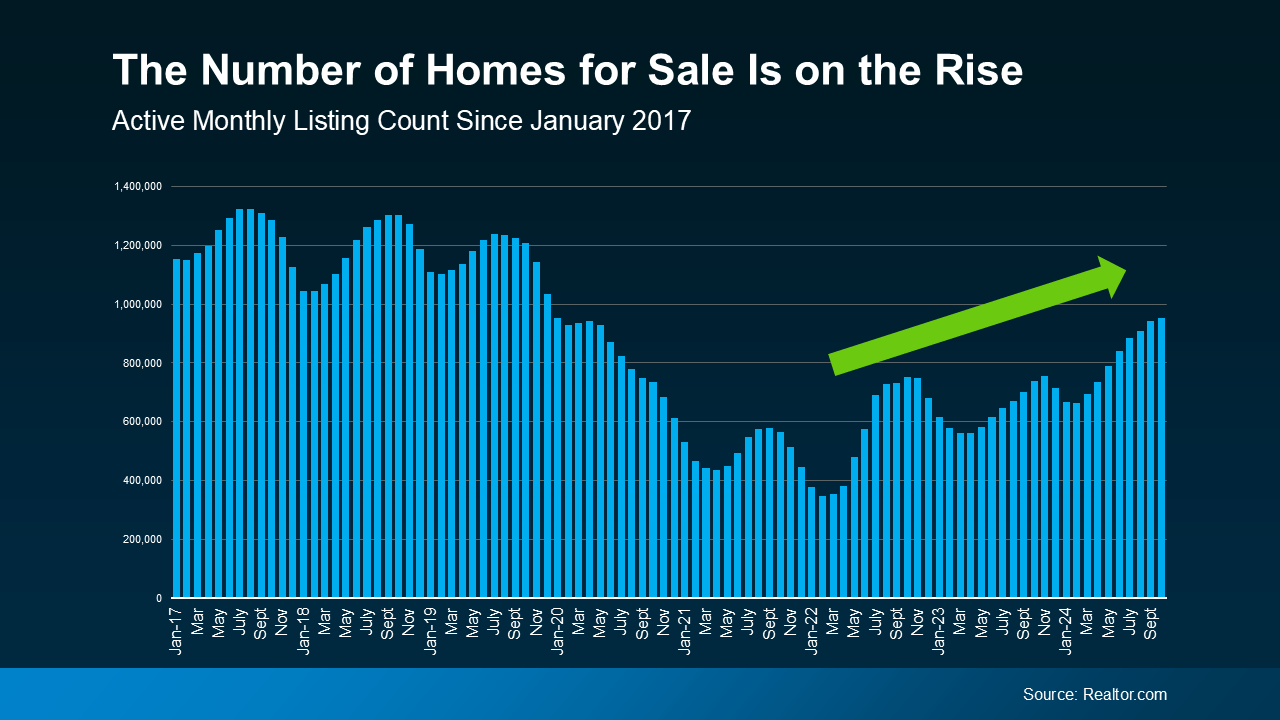

More Homes, Slower Price Growth – What It Means for You as a Buyer

There are more homes on the market right now than there have been in years – and that could be a game changer for you if you’re ready to buy. Let’s look at two reasons why.

You Have More Options To Choose From

An article from Realtor.com helps explain just how much the number of homes for sale has gone up this year:

“There were 29.2% more homes actively for sale on a typical day in October compared with the same time in 2023, marking the twelfth consecutive month of annual inventory growth and the highest count since December 2019.”

And while the number of homes on the market still isn’t quite back to where it was in the years leading up to the pandemic, this is definitely an improvement (see graph below):

With more homes available for sale now, you have more options to choose from. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, explains:

With more homes available for sale now, you have more options to choose from. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, explains:

“Though still lower than pre-pandemic, burgeoning home supply means buyers have more options . . .”

That means you have a better chance of finding a house that meets your needs. It also means the buying process doesn’t have to feel quite as rushed, because more options on the market means you’ll likely face less competition from other buyers.

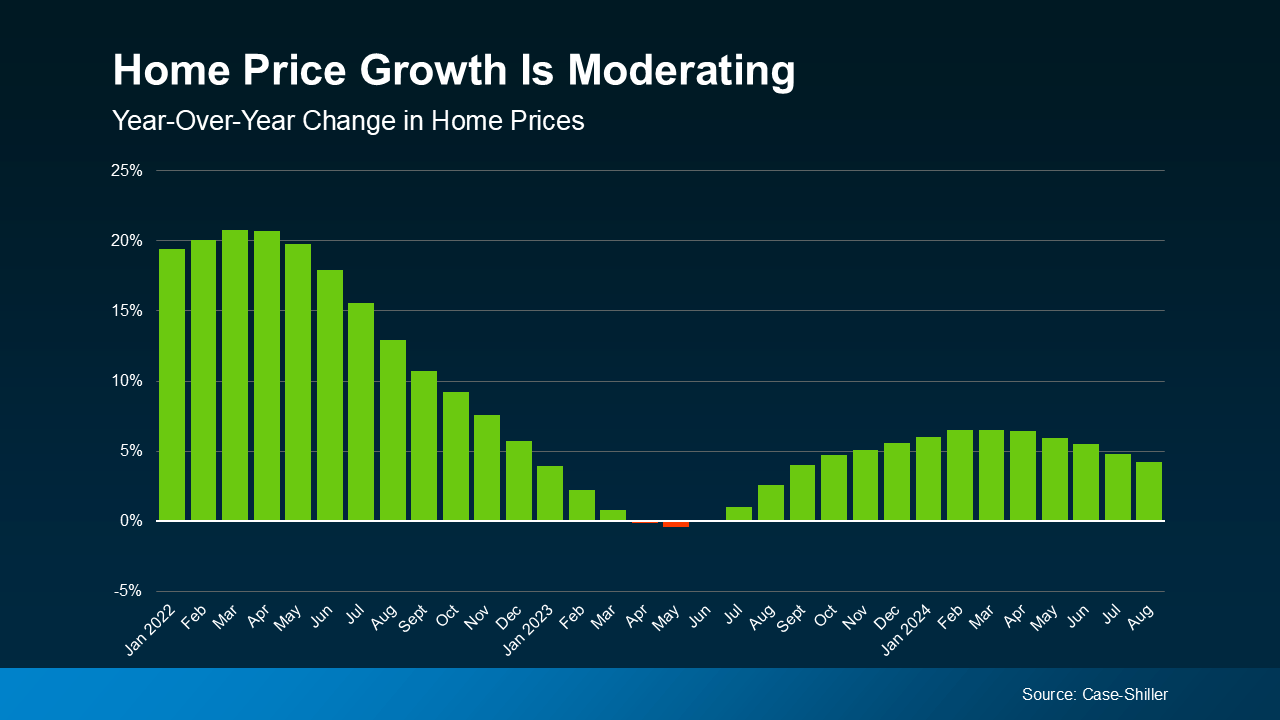

Home Price Growth Is Slowing

When there aren’t many homes for sale, buyers have to compete more fiercely for the ones that are available. That’s what happened a few years ago, and it’s what drove prices up so quickly.

But now, the increasing number of homes on the market is causing home price growth to slow down (see graph below):

In certain markets, the number of available homes has not only bounced back to normal, but has even surpassed pre-pandemic levels. In those areas, home price growth has slowed or stalled completely. As Lance Lambert, Co-Founder of ResiClub, explains:

In certain markets, the number of available homes has not only bounced back to normal, but has even surpassed pre-pandemic levels. In those areas, home price growth has slowed or stalled completely. As Lance Lambert, Co-Founder of ResiClub, explains:

“Generally speaking, housing markets where active inventory has returned to pre-pandemic 2019 levels have seen home price growth soften or even decline outright from their 2022 peak.”

Slower or stalled price growth could give you a better chance of finding something within your budget. As Dr. Anju Vajja, Deputy Director at the Federal Housing Finance Agency (FHFA), says:

“For the third consecutive month U.S. house prices showed little movement . . . relatively flat house prices may improve housing affordability.”

But remember, inventory levels and home prices are going to vary by market.

So, having a real estate agent who knows the local area can be a big advantage. They can help you understand the trends in your community, which can make a real difference in finding a home that fits your needs and budget.

Bottom Line

More housing options – and the slower home price growth they bring – can help you find and buy a home that works for your lifestyle and budget. So don’t hesitate to reach out if you want to talk about the growing number of choices you have right now.

What’s Motivating Homeowners To Move Right Now

Over the past few years, some homeowners have decided to delay their move because they don’t want to sell and take on a higher mortgage rate on their next home. Maybe you’re thinking the same thing. And honestly, that’s no surprise. It’s a very common roadblock and is one of the biggest factors that’s kept the number of homes on the market so low for so long.

But a growing number of homeowners are deciding they just can’t wait any longer. Often, it’s because of personal or lifestyle change. As Redfin explains:

“Some homeowners are opting to bite the bullet and give up their low rate in order to move. Many are selling because a major life event like a job change, or divorce . . .”

If you’re weighing the decision to move, take a look at some of the top reasons others are choosing to sell. You might find those are reason enough for you to move now, too.

It’s Time for a Change

A new job in a different city, a desire to be closer to family, or simply wanting a change of scenery can all spark the need to sell.

Let’s say you’ve landed a great job offer that requires relocating, listing your current home quickly may be the next logical step.

There’s Just Not Enough Space in Your Current House

Sometimes, your current home just doesn’t fit your lifestyle anymore. A growing family, the need for a home office, or more room for entertaining can all drive the decision to upgrade to a larger space.

As an example, if you live in a condo and have a baby on the way, selling might be the next best move so you can find a larger home that suits your needs.

Retirement or Wanting To Downsize

On the flip side, some homeowners are ready to downsize. This could be due to children moving out, retirement, or simply wanting less to maintain.

If you’re newly retired and dreaming of a simpler lifestyle, downsizing to a smaller home could free up both time and resources to enjoy this new chapter of life.

Changes in Relationship Status

Big changes like divorce, separation, or marriage often lead to a need for new living arrangements.

If you just went through a divorce, selling the house you once shared may allow both of you to move forward and find a living situation that works better for you now.

Health and Mobility Needs

Health concerns, especially those that affect mobility, can also drive the decision to sell. A home that once worked well might no longer suit your needs.

If this sounds like your experience right now, selling your current home to move into a more accessible space, or even using the proceeds for assisted living, could significantly improve your quality of life.

Bottom Line

Selling your home isn’t just about market conditions or mortgage rates—it’s also about making the best decision for your lifestyle and future. As Bankrate says:

“Deciding whether it’s the right time to sell your home is a very personal choice. There are numerous important questions to consider, both financial and lifestyle-based . . . Your future plans and goals should be a significant part of the equation.”

If a major life change has you thinking about moving, now might still be the right time to sell. Let’s connect so you have an expert to help you navigate the process.

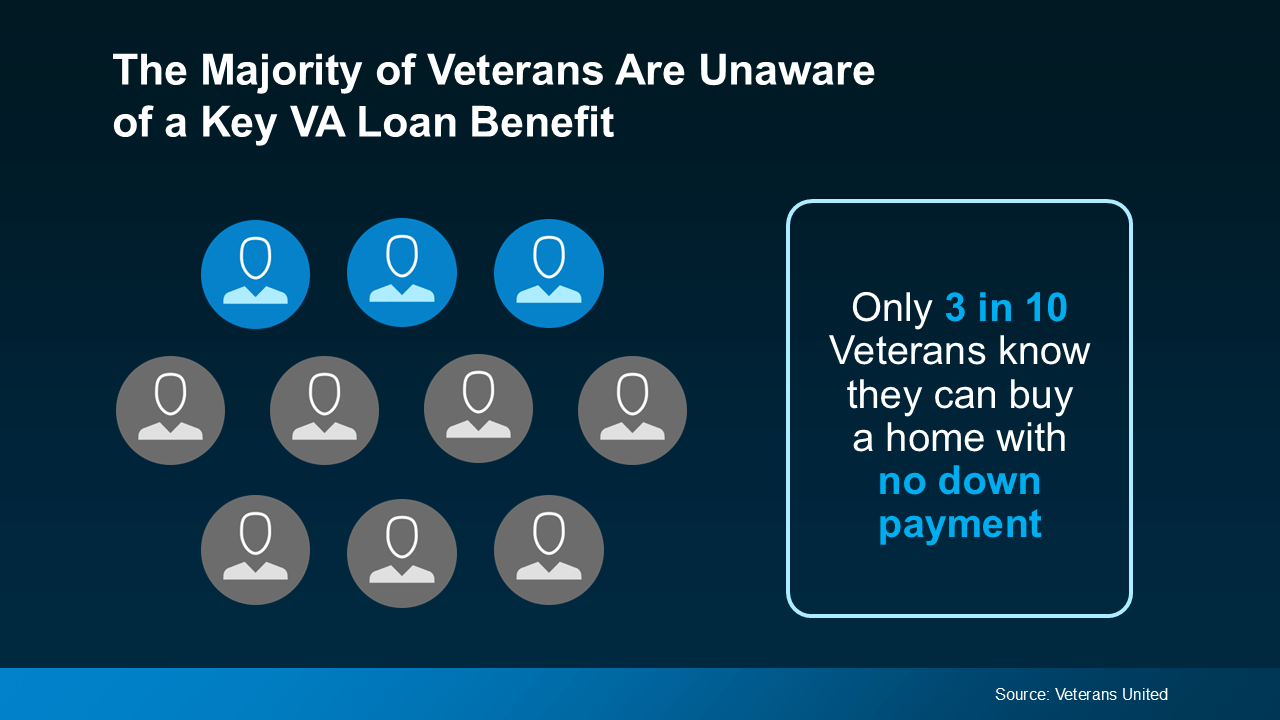

The Majority of Veterans Are Unaware of a Key VA Loan Benefit

For over 79 years, Veterans Affairs (VA) home loans have helped countless Veterans achieve the dream of homeownership. But according to Veterans United, only 3 in 10 Veterans realize they may be able to buy a home without needing a down payment (see visual below):

That’s why it’s so important for Veterans – and anyone who cares about a Veteran – to be aware of this valuable program. Knowing about the resources available can make the path to homeownership easier and keep life-changing plans from being put on hold. As Veterans United explains:

That’s why it’s so important for Veterans – and anyone who cares about a Veteran – to be aware of this valuable program. Knowing about the resources available can make the path to homeownership easier and keep life-changing plans from being put on hold. As Veterans United explains:

“The ability to buy with 0% down is the signature advantage of this nearly 80-year-old benefit program. Eligible Veterans can buy as much house as they can afford, all without the need to spend years saving for a down payment.”

The Advantages of VA Home Loans

VA home loans are designed to make homeownership a reality for those who have served our country. These loans come with the following benefits according to the Department of Veterans Affairs:

- Options for No Down Payment: One of the biggest perks is that many Veterans can buy a home with no down payment at all, making it simpler to get started on your homebuying journey.

- Limited Closing Costs: With VA loans, there are limits on the types of closing costs Veterans have to pay. This helps keep more money in your pocket when you’re ready to finalize the sale.

- No Private Mortgage Insurance (PMI): Unlike many other loan types, VA loans don’t require PMI, even with lower down payments. This means lower monthly payments, which adds up to big savings over time.

Your team of expert real estate professionals, including a local agent and a trusted lender, are the best resource to understand all the options and advantages available to help you achieve your homebuying goals.

Bottom Line

Owning a home is a key part of the American Dream, and VA home loans are a powerful benefit for those who’ve served our country. Let’s connect to make sure you have everything you need to make confident decisions in the housing market.

Why You Need an Agent To Set the Right Asking Price

Some Highlights

- The #1 task sellers struggle with is setting the right asking price for their house.

- Without an agent’s help, you may set a price that turns away buyers and takes a long time to sell.

- To make sure your house is priced right, let’s connect. Because, if the price isn’t compelling, it’s not selling.

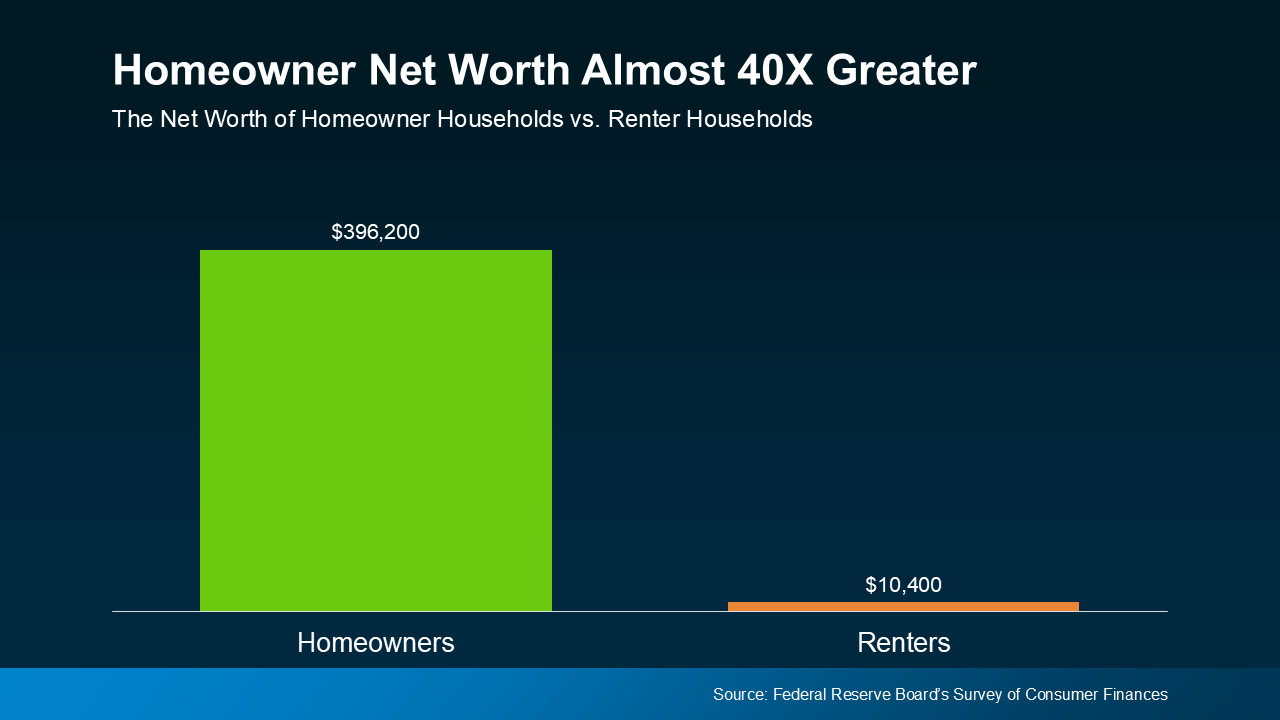

Renting vs. Buying: The Net Worth Gap You Need To See

Trying to decide between renting or buying a home? One key factor that could help you choose is just how much homeownership can grow your net worth.

Every three years, the Federal Reserve Board shares a report called the Survey of Consumer Finances (SCF). It shows how much wealth homeowners and renters have – and the difference is significant.

On average, a homeowner’s net worth is nearly 40 times higher than a renter’s. Check out the graph below to see the difference for yourself:

Why Homeowner Wealth Is So High

Why Homeowner Wealth Is So High

Why Homeowner Wealth Is So High

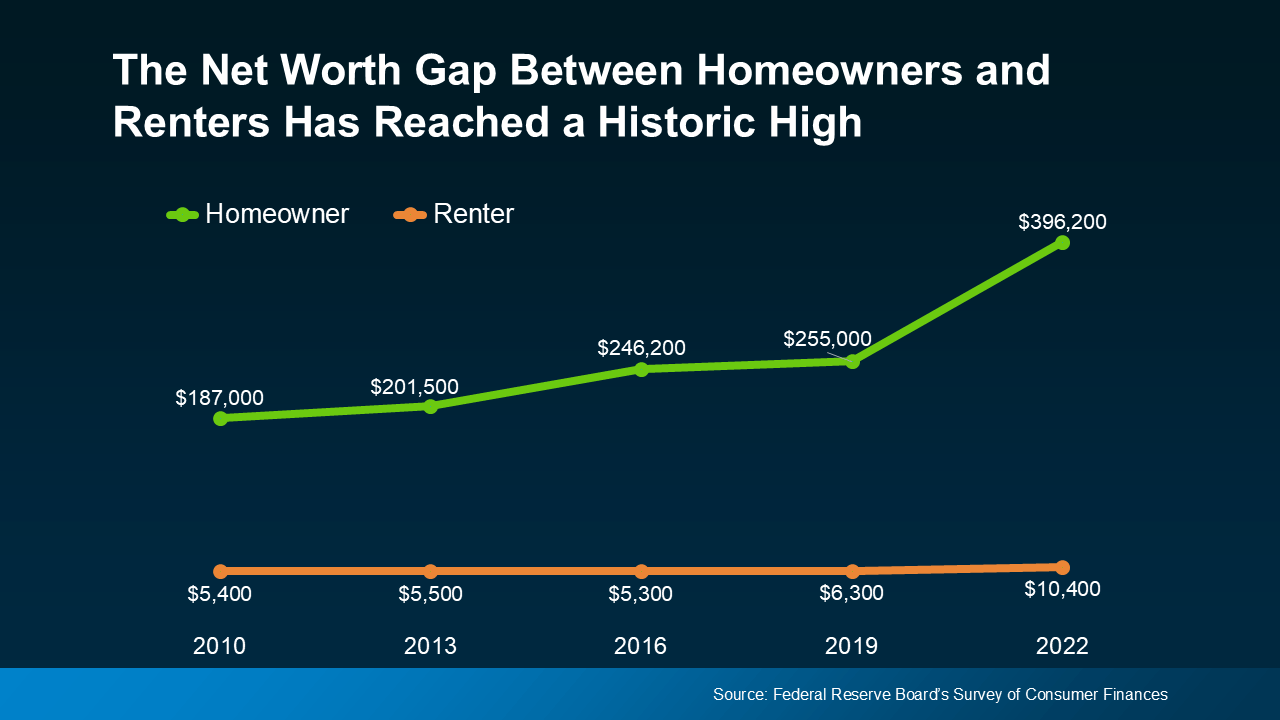

Why Homeowner Wealth Is So HighIn the previous version of that report, the average homeowner’s net worth was about $255,000, while the average renter’s was just $6,300. That’s still a big gap. But in the most recent update, the spread got even bigger as homeowner wealth grew even more (see graph below):

As the SCF report says:

As the SCF report says:

“. . . the 2019-2022 growth in median net worth was the largest three-year increase over the history of the modern SCF, more than double the next-largest one on record.”

One big reason why homeowner wealth shot up is home equity.

Equity is the difference between your home’s value and what you owe on your mortgage. You gain equity by paying down your mortgage and when your home’s value goes up.

Over the past few years, home prices have gone up a lot. That’s because there weren’t enough available homes for all the people who wanted one. This supply-demand imbalance pushed home prices up – and that translated into faster equity gains and even more net worth for homeowners.

If you’re still torn between whether to rent or buy, here’s what you should know. While inventory has grown this year, in most places, there’s still not enough to go around. That’s why expert forecasts show prices are expected to go up again next year nationally. It’ll just be at a more moderate pace.

While that’s not the sky-high appreciation we saw during the pandemic, it still means potential equity gains for you if you buy now. As Ksenia Potapov, Economist at First American, explains:

“Despite the risk of volatility in the housing market, homeownership remains an important driver of wealth accumulation and the largest source of total wealth among most households.”

But prices and inventory are going to vary by area. So, lean on a local real estate agent. They’ll be able to give you the local trends and speak to the other financial and lifestyle benefits that come with owning a home. That crucial information will help you decide the best move for you right now. As Bankrate explains:

“Deciding between renting and buying a home isn’t just about cost — the decision also involves long-term financial strategies and personal circumstances. If you’re on the fence about which is right for you, it may be helpful to speak with a local real estate agent who knows your market well. An experienced agent can help you weigh your options and make a more informed decision.”

Bottom Line

If you’re not sure if you should rent or buy, keep in mind that if you can make the numbers work, owning a home can really grow your wealth over time.

And if homeownership feels out of reach, let’s connect so we can explore programs that may make buying possible.