Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Thinking About Buying a Home? Ask Yourself These Questions

If you’re thinking of buying a home this year, you’re probably paying closer attention than normal to the housing market. And you’re getting your information from a variety of channels: the news, social media, your real estate agent, conversations with friends and loved ones, the list goes on and on. Most likely, home prices and mortgage rates are coming up a lot.

Here are the top two questions you need to ask yourself as you make your decision, including the data that helps cut through the noise.

1. Where Do I Think Home Prices Are Heading?

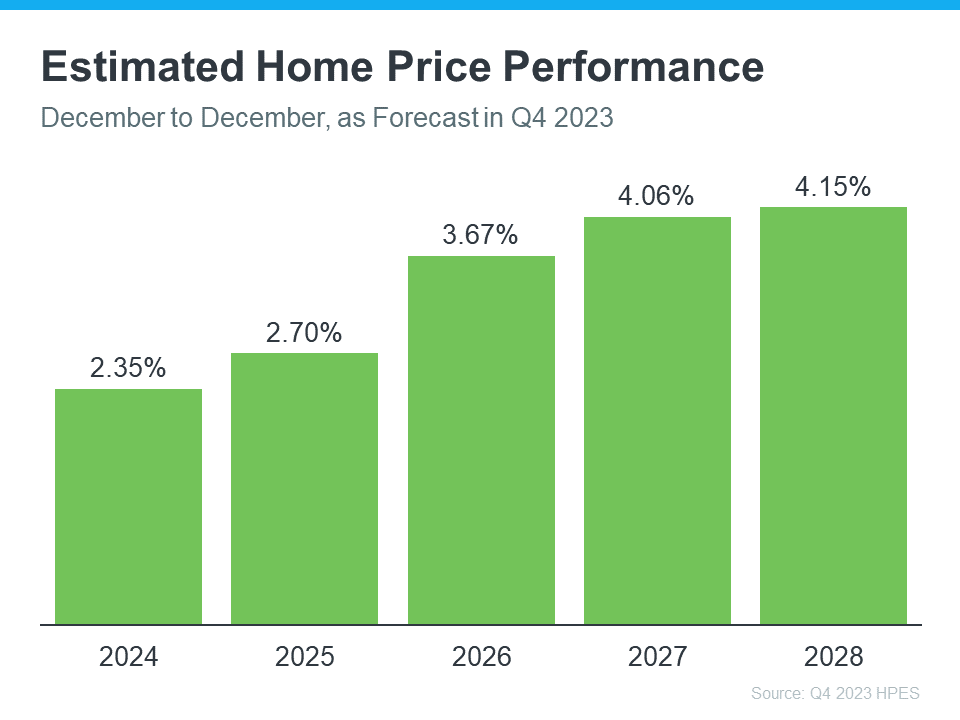

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

According to the most recent release, the experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

So, why does this matter to you? While the percent of appreciation may not be as high as it was in recent years, what’s important to focus on is that this survey says we’ll see prices rise, not fall, for at least the next 5 years.

And home prices rising, even at a more moderate pace, is good news not just for the market, but for you too. It means, by buying now, your home will likely grow in value, and you should gain home equity in the years ahead. But, if you wait, based on these forecasts, the home will only cost you more later on.

2. Where Do I Think Mortgage Rates Are Heading?

Over the past year, mortgage rates spiked up in response to economic uncertainty, inflation, and more. But there’s an encouraging sign for the market and mortgage rates. Inflation is moderating, and here’s why this is such a big deal if you’re looking to buy a home.

When inflation cools, mortgage rates generally fall in response. That’s exactly what we’ve seen in recent weeks. And, now that the Federal Reserve has signaled they’re pausing their Federal Funds Rate increases and may even cut rates in 2024, experts are even more confident we’ll see mortgage rates come down.

Danielle Hale, Chief Economist at Realtor.com, explains:

“. . . mortgage rates will continue to ease in 2024 as inflation improves and Fed rate cuts get closer. . . . a key factor in starting to provide affordability relief to homebuyers.”

As an article from the National Association of Realtors (NAR) says:

“Mortgage rates likely have peaked and are now falling from their recent high of nearly 8%. . . . This likely will improve housing affordability and entice more home buyers to return to the market . . .”

No one can say with absolute certainty where mortgage rates will go from here. But the recent decline and the latest decision from the Federal Reserve to stop their rate increases, signals there’s hope on the horizon. While we may see some volatility here and there, affordability should improve as rates continue to ease.

Bottom Line

If you’re thinking about buying a home, you need to know what’s expected with home prices and mortgage rates. While no one can say for certain where they’ll go, making sure you have the latest information can help you make an informed decision. Let’s connect so you can stay up to date on what’s happening and why this is such good news for you.

Invest in Yourself by Owning a Home

Are you wondering if it makes sense to buy a home right now? While today’s mortgage rates might seem a bit intimidating, here are two compelling reasons why it still may be a good time to become a homeowner.

Home Values Appreciate over Time

There’s been a lot of confusion around what’s happened with home prices over the past two years. While they did dip ever so slightly in late 2022, this year they’ve been appreciating at a more normal pace, which is good news for the housing market. And while looking at price movement over just a year or two can make you worry prices are usually this unpredictable, history shows in the long run, home values rise (see graph below):

Using data from the Federal Reserve for the past 60 years, you can see the overall trend is home prices have climbed quite steadily. Sure, there was an exception around the housing crash of 2008 that caused prices to break the usual trend for a time, but overall, home values have been consistently on the rise.

Increasing home values is one great reason why buying may make more sense than renting. As prices rise, and as you pay down your mortgage, you build equity. Over time, that growing equity gives your net worth a boost.

Rent Keeps Going Up Through the Years

Another reason you may want to consider buying a home instead of renting is the never-ending rent hike. If you’ve ever felt the pinch of rent increasing year after year, you’re not alone. That’s because, rents have climbed steadily over the past six decades (see graph below):

By buying a home, you can lock in your monthly housing costs and bid farewell to those pesky rent hikes. That stability is a game-changer.

In the end, it all boils down to this: your housing payments are an investment, and you’ve got a choice to make. Do you want to invest in yourself or your landlord?

By becoming a homeowner, you’re investing in your own future. When you rent, that’s money you never get back.

When you factor in home values consistently rising, plus the opportunity to get relief from never-ending rent hikes, homeownership can be a path to financial security. As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), states:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line

When it comes down to it, buying a home offers more benefits than renting, even when mortgage rates are high. If you want to avoid increasing rents and take advantage of long-term home price appreciation, let’s connect to go over your options.

Understanding the Benefits of Owning Your First Home

Are you considering buying your first home? If so, it can be helpful to know what led other people to make that decision. According to a recent survey of first-time homebuyers by PulteGroup:

“When asked why they purchased their first home recently, the answer was simple: because they wanted to. Either the desire to stop renting or recognition that homeownership is a smart financial investment was the main motivator for 72% of respondents.”

While that survey looked specifically at first-time homebuyers buying newly built homes, the same sentiment is true for just about anyone buying their first home. Here’s a bit more information to help you think about those two benefits of homeownership to see if they’re a key factor for you too.

When You Buy a Home, You Have More Stability than When You Rent

You might want to stop renting because rents keep going up. If you’re a renter, that means there’s a chance your payment will increase each time you sign a new rental agreement or renew your current one.

On the other hand, when you buy your home with a fixed-rate mortgage, your monthly housing payment is predictable over the length of that loan. This stability can give you a peace of mind that renting just can’t provide. Jeff Ostrowski, real estate journalist, breaks it down:

“With a fixed-rate mortgage, your monthly principal and interest payment is set for as long as you keep the loan. Sign a rental lease, however, and you could see your rent rise the following year, the year after that and so on.”

When You Buy a Home, You Grow Your Wealth as Home Values Climb

Beyond that, owning a home can also be a great long-term investment. While renting may be the more affordable option right now, it doesn’t provide an avenue for you to grow your wealth over time. Mark Fleming, Chief Economist at First American, explains that’s an important distinction to consider:

“Given current dynamics, more young households may choose to rent in the near term as the cost to own, excluding house price appreciation, has unequivocally increased. Yet, accounting for house price appreciation in that cost of homeownership, whether to rent or buy will depend on where, and if, a home is likely to cost more or less in the near future.”

Basically, renting doesn’t allow you to build equity. In contrast, homeownership can help you grow your net worth as your home’s value appreciates. That’s a significant perk you can’t get if you keep renting.

When you take that into account, it may make better financial sense to buy. Most experts project home prices will continue to appreciate over the next few years at a pace that’s more normal for the market. That means when you buy a home, not only are you investing in a place to live, but you’re also investing in your financial future.

Bottom Line

If you’re ready, it can be a smart move to buy your first home instead of renting. Let’s connect so you can stabilize your housing payment and start building wealth for your future.

Unpacking the Long-Term Benefits of Homeownership

If you’re thinking about buying a home soon, higher mortgage rates, rising home prices, and ongoing affordability concerns may make you wonder if it still makes sense to buy a home right now. While those market factors are important, there’s more to consider. You should think about the long-term benefits of homeownership too.

Think about this: if you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. Why is that? The reason is tied to how home values grow with time and how, by extension, that grows your own wealth. That may be why, in a recent Fannie Mae survey, 76% of respondents say they believe buying a home is a safe investment.

Here’s a look at how just the home price appreciation piece can really add up over the years.

Home Price Growth over Time

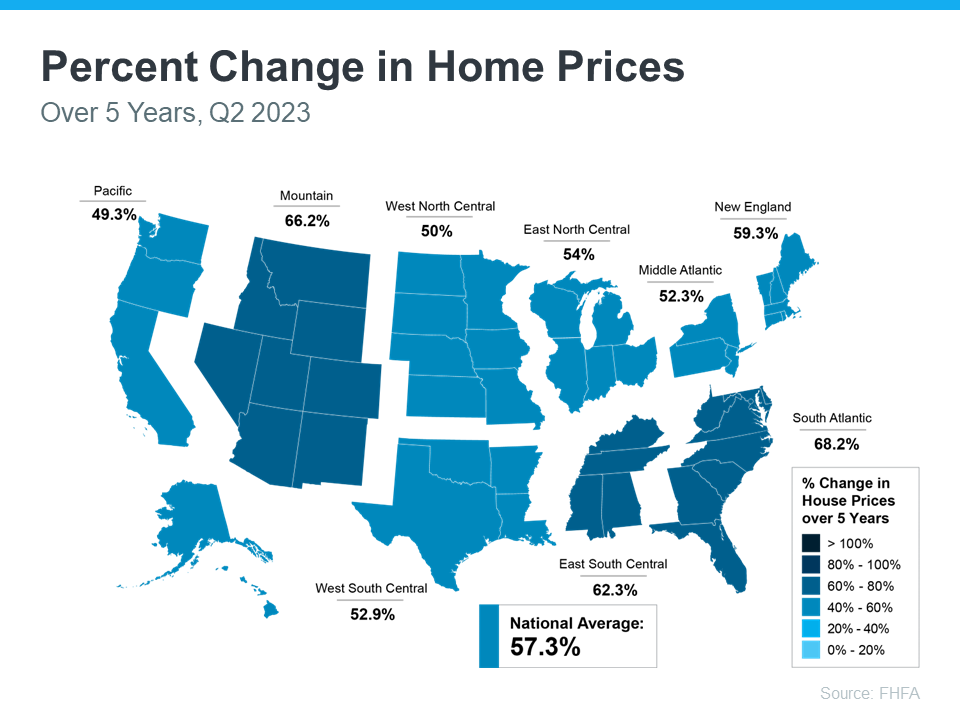

The map below uses data from the Federal Housing Finance Agency (FHFA) to show just how noteworthy price gains have been over the last five years. And, since home prices vary by area, the map is broken out regionally to help convey larger market trends:

If you look at the percent change in home prices, you can see home prices grew on average by just over 57% nationwide over a five-year period.

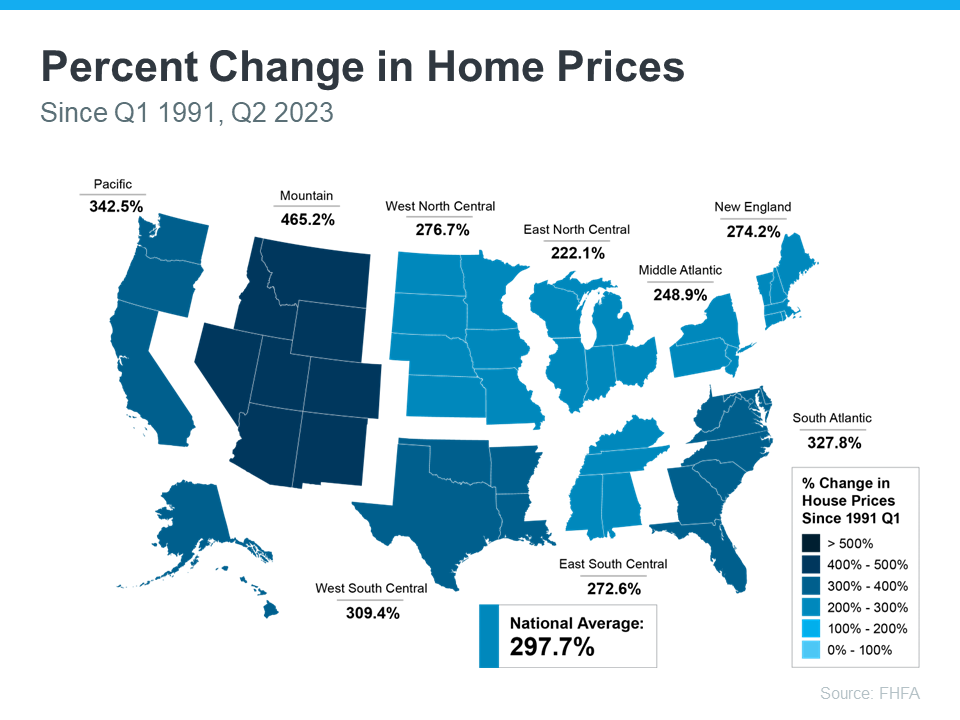

Some regions are slightly above or below that average, but overall, home prices gained solid ground in a short time. And if you expand that time frame even more, the benefit of homeownership and the drastic gains homeowners made over the years become even clearer (see map below):

The second map shows, nationwide, home prices appreciated by an average of over 297% over a roughly 30-year span.

This nationwide average tells you the typical homeowner who bought a house 30 years ago saw their home almost triple in value over that time. That’s a key factor in why so many homeowners who bought their homes years ago are still happy with their decision.

And while you may have heard talk throughout the year that home prices would crash, it hasn’t happened. In fact, experts project home prices will continue to rise for years to come.

Bottom Line

If you’re wondering if it still makes sense to buy a home today, it’s important to focus on the long-term advantages that come with homeownership. When you’re ready to start your homebuying journey, let’s chat.