Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

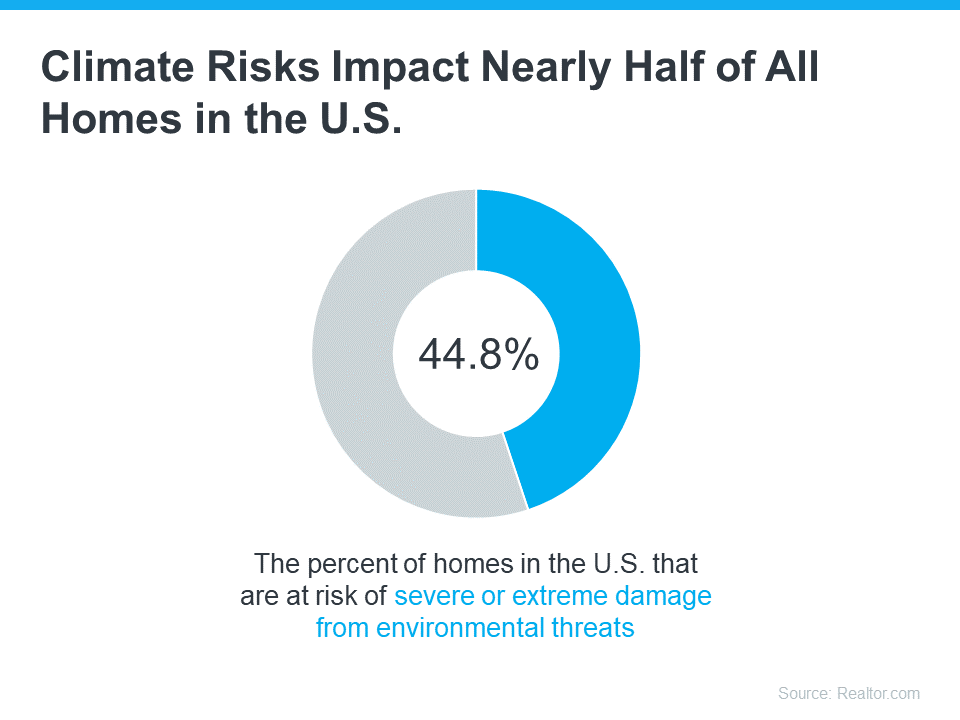

How Do Climate Risks Affect Your Next Home?

Climate change is impacting where people buy homes. As the experts at the National Association of Realtors (NAR) explain:

“Sixty-three percent of people who have moved since the pandemic began say they believe climate change is—or will be—an issue in the place they currently live.”

If you’re planning to move, climate change is something you might want to consider, no matter where you are. A recent study from Realtor.com helps put the growing impact climate change is having on real estate into perspective (see below):

So, how can you be sure your investment is safe from the elements?

For starters, work with a local real estate agent to understand the likelihood of your future home being exposed to hazards like wind, floods, and wildfires. Your agent will know the area and be able to tell you about the risks you’ll most likely face.

Beyond that, there are two important factors to think about: the quality of the home you want to buy and the insurance you’ll need to protect it.

A Home Built to Last

If you’re planning to be in your home for many years, you want to know it’s going to last. One way to think ahead is to work with your real estate agent to ensure the home you buy can withstand environmental hazards. They’re up to date on the most common building and remodeling techniques—like a secondary water barrier on the roof or noncombustible, fire-resistant exterior walls—used to protect homes from the effects of climate change.

And if the home you’re interested in doesn’t have the features you’re looking for, they can help you determine what you may be able to negotiate in the contract or what work it might require in the future.

Insurance To Protect It

Once you’re confident the home you’re looking at is well built, the next step is finding out what it’s going to take to insure it. As Selma Hepp, Chief Economist at CoreLogic, says:

“. . . homeowners are going to become increasingly more aware of risks of living in some areas as it becomes prohibitively expensive or very difficult to obtain hazard insurance.”

In areas where climate risks are having a bigger impact, the right home insurance can make a big difference. And the price of that insurance is an important factor when thinking about your budget and the true cost of buying and protecting your home. Get an insurance quote early in the process because you may want to compare multiple quotes and it can take several weeks to get them.

While this may feel like a lot to consider, don’t worry. An agent can help. Your real estate agent will be your go-to resource on the homebuying process, what to look for and consider, and how climate change may affect your next home. With the right planning and an agent’s expert advice, you can make this happen. Homeownership is worth it. And with a great agent by your side, you can make sure the home you find is the right fit.

Bottom Line

Climate change is an important factor to think about when buying a home. After all, your home is a huge investment, and you want to be ready for anything that might affect it. Let’s chat so you can find the perfect home.

How VA Loans Can Help You Buy a Home

For over 80 years, Veterans Affairs (VA) home loans have helped millions of veterans buy their own homes. If you or someone you know has served in the military, it’s important to learn about this program and its benefits.

Here are some key things to know about VA loans before buying a home.

Top Benefits of VA Home Loans

VA home loans make it easier for veterans to buy a home, and they’re a great perk for those who qualify. According to the Department of Veteran Affairs, some benefits include:

- Options for No Down Payment: Qualified borrowers can often purchase a home with no down payment. That’s a huge weight lifted when you’re trying to save for a home. The Associated Press says:

“. . . about 90% of VA loans are used to purchase a home with no money down.”

- Don’t Require Private Mortgage Insurance (PMI): Many other loans with down payments under 20% require PMI. VA loans do not, which means veterans can save on their monthly housing costs.

- Limited Closing Costs: There are limits on the types of closing costs you pay when you qualify for a VA home loan. So, more money stays in your pocket when it’s time to seal the deal.

An article from Veterans United sums up how remarkable this loan can be:

“For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.”

Bottom Line

Owning a home is the American Dream. Veterans give a lot to protect our country, and one way to honor them is by making sure they know about VA home loans.

Your Agent Is the Key To Pricing Your House Right

The asking price for your house can impact your bottom line and how quickly it sells. Both under- and overpricing have drawbacks. So to find the right price for your house, lean on your agent for their expertise. Don’t pick just any price for your listing. Trust your real estate professional to help you find the perfect price for your house.

Questions You May Have About Selling Your House

There’s no denying mortgage rates are having a big impact on today’s housing market. And that may leave you with some questions about whether it still makes sense to sell your house and make a move.

Here are three of the top questions you may be asking – and the data that helps answer them.

1. Should I Wait To Sell?

If you’re thinking about waiting to sell until after mortgage rates come down, here’s what you need to know. So are a ton of other people.

And while mortgage rates are still forecasted to come down later this year, if you wait for that to happen, you may be dealing with a lot more competition as other buyers and sellers jump back in too. As Bright MLS says:

“Even a modest drop in rates will bring both more buyers and more sellers into the market.”

That means if you wait it out, you’ll have to deal with things like prices rising faster and more multiple-offer scenarios when you buy your next home.

2. Are Buyers Still Out There?

But that doesn’t mean no one is moving right now. While some people are holding off, there are still plenty of buyers active today. And here’s the data to prove it.

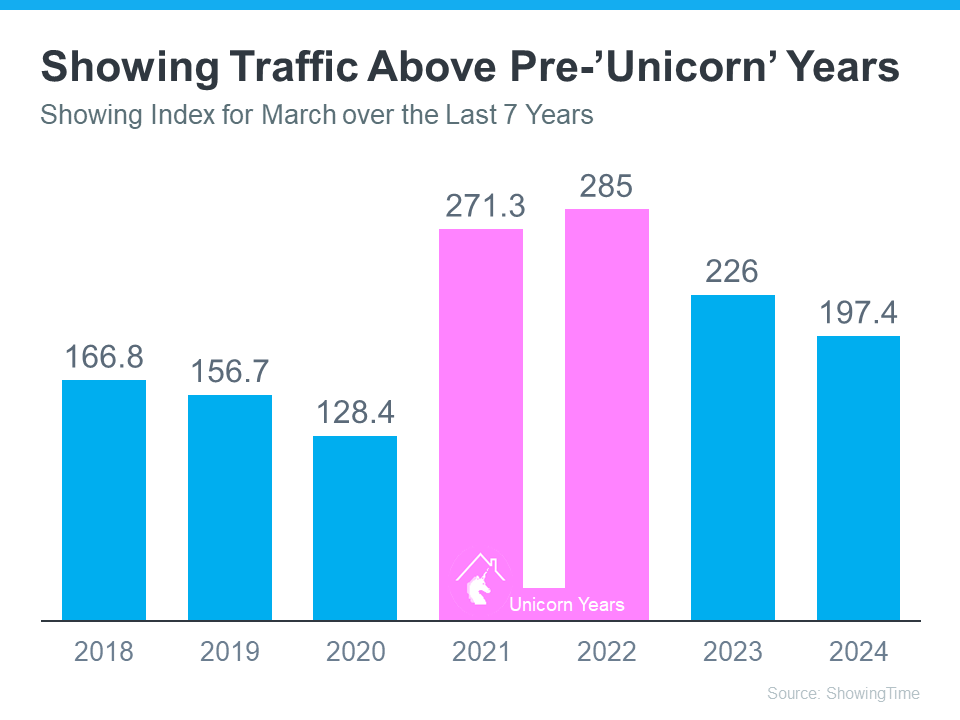

The ShowingTime Showing Index is a measure of how frequently buyers are touring homes. The graph below uses that index to show buyer activity for March (the latest data available) over the past seven years:

You can see demand has dipped some since the ‘unicorn’ years (shown in pink). That’s in response to a lot of market factors, like higher mortgage rates, rising prices, and limited inventory. But, to really understand today’s demand, you have to compare where we are now with the last normal years in the market (2018-2019) – not the abnormal ‘unicorn’ years.

When you focus on just the blue bars, you can get an idea of how 2024 stacks up. And that gives you a whole new perspective.

Nationally, demand is still high compared to the last normal years in the housing market (2018-2019). And that means there’s still a market for your house to sell.

3. Can I Afford To Buy My Next Home?

And if you’re worried about how you’ll afford your next move with today’s rates and prices, consider this: you probably have more equity in your current home than you realize.

Homeowners have gained record amounts of equity over the past few years. And that equity can make a big difference when you buy your next home. You may even have enough to be an all-cash buyer and avoid taking out a mortgage altogether. As Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), says:

“ . . . those who have earned housing equity through home price appreciation are the current winners in today’s housing market. One-third of recent home buyers did not finance their home purchase last month—the highest share in a decade. For these buyers, interest rates may be less influential in their purchase decisions.”

Bottom Line

If you’ve had these three questions on your mind and they’ve been holding you back from selling, hopefully, it helps to have this information now. A recent survey from Realtor.com shows more than 85% of potential sellers have been considering selling for over a year. That means there are a number of sellers like you who are on the fence.

But that same survey also talked to sellers who recently decided to take the plunge and list. And 79% of those recent sellers wish they’d sold sooner.

If you want to talk more about any of these questions or need more information, let’s connect.

How Many Homes Are Investors Actually Buying?

Are big investors really buying up all the homes today?

If you’re trying to find a house to buy, this may be something you’re wondering about. Maybe you’ve read about it or seen reels on social media saying investors buying all the homes is making it even harder to find what the average buyer is looking for. But spoiler alert – there’s a lot of misinformation out there. To clear things up, here’s the scoop on what’s really happening. A lot of the big investor activity is actually in the rearview mirror already.

The Wall Street Journal (WSJ) explains:

“Investors of all sizes spent billions of dollars buying homes during the pandemic. At the 2022 peak, they bought more than one in every four single-family homes sold, though more recently their activity has slowed as interest rates rose and supply became tighter.”

The key here is investor activity has slowed significantly, and even during the peak of investor buying, 3 out of every 4 single-family homes purchased were by regular, everyday buyers – not investors. And of the investors who bought over the past few years, most weren’t the big investors you may be hearing about. The vast majority were small mom-and-pop investors – people like your neighbors who own only a couple of homes, maybe even just their main residence and a vacation home.

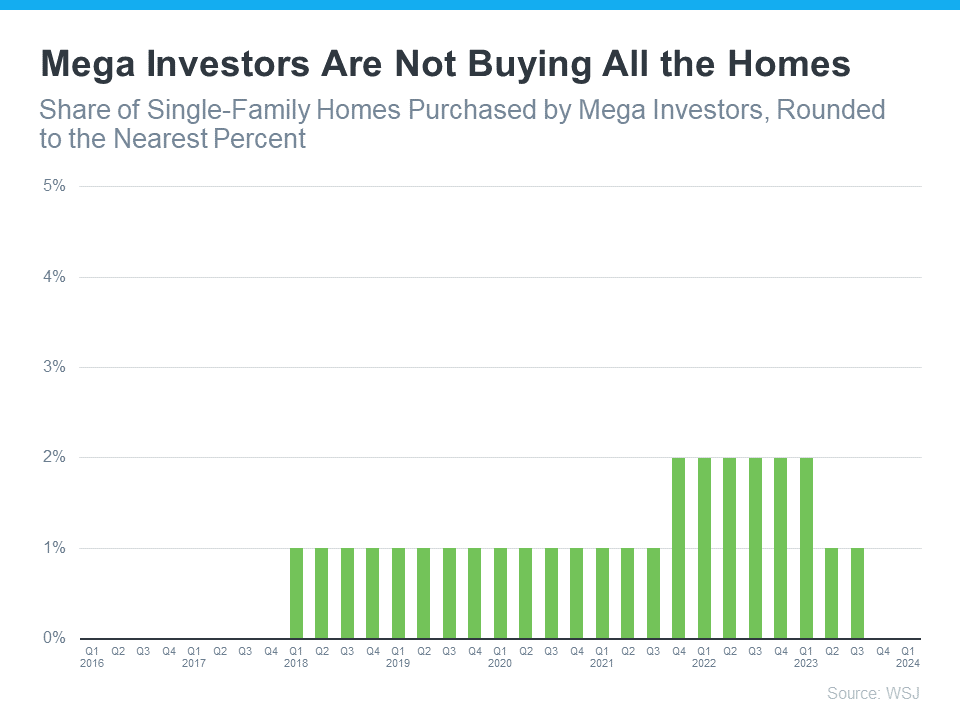

But let’s focus on the giant, mega-investor firms since that’s what is being talked about so frequently on social media right now. Mega investors are those who own 1,000+ properties. You may be surprised to see that, according to the Wall Street Journal, they don’t buy all that many homes (see graph below):

This graph tells us two things. First, institutional investors were never buying a large percentage of available homes. During the peak in 2022, they bought about 2% of available single-family homes. Second, that percentage has gotten even smaller recently (so small the number rounds down to 0%).

In an effort to understand why that percentage is trending down, private lender RCN Capital asked investors about the challenges they’re facing. Here’s what Jeffrey Tesch, CEO of RCN Capital, found out:

“Investors are already facing many challenges in today’s housing market – rising prices, limited inventory, and higher financing costs.”

Understanding these challenges is important because they show big, mega investors aren’t taking over the housing market.

So, don’t fall for everything you hear. They aren’t snatching up all the homes and making it impossible for regular people to buy.

Bottom Line

Big investors aren’t buying all the homes out there. If you’ve got questions about what you’re hearing about the housing market, let’s chat. I can help you understand what’s really going on.

Worried About Home Maintenance Costs? Consider This

If one of the main reasons you’re hesitant to buy a home is because you’re worried about the upkeep, here’s some information you may find interesting on both new home construction and existing homes (a home that’s been lived in by a previous owner).

Newly Built Homes Need Less Upfront Maintenance

If you can afford it, you may find a newly built home could help ease your worries about maintenance costs. Think about it, if everything in the house is brand new, it won’t have the wear and tear you may see in an existing home – and that means it’s less likely to need repairs. As LendingTree says:

“Since the systems, appliances, roof and foundation are new, you’re less likely to pay for major or minor repairs within the first few years of homeownership. That can make a big difference for first-time homebuyers who are adjusting to owning rather than renting.”

Plus, many builders also have warranties on their homes that would cover some of the more major expenses that could pop up. As First American explains:

“The new systems in your home, like plumbing, electrical, and HVAC, are typically covered for one to two years by your builder’s warranty. When something happens to these systems, you contact the builder or their warranty company.”

Existing Homes Can Still Have Great Perks

But it’s worth mentioning, that it’s not just newly built homes that can have warranties. It’s an option for existing homes too.

Your agent may be able to help you negotiate with the seller to add one as a concession on your contract. But you should know that not all sellers will be willing to do that. If they won’t, you could purchase one yourself, if you’d like to. An article from Forbes explains:

“During a real estate transaction, a home warranty policy can be purchased by the buyer or the seller.”

And there are benefits for both parties when it comes to a home warranty. According to MarketWatch:

“A buyer’s home warranty benefits both buyers and sellers, as it helps the seller close the deal while providing the future homeowner with peace of mind that they’ll be covered if a system or appliance breaks down . . . Sometimes, a seller will pay for the first year of the home buyer’s warranty to sweeten the deal, but it depends on the real estate market.”

If you’re interested in a home warranty for peace of mind, lean on your agent. They’ll negotiate on your behalf to see if a seller would be willing to cover one for you. Just remember, the likelihood of a seller throwing one in depends on conditions in your local market.

So, Should I Buy New or Existing?

While the need for less upfront maintenance is a great perk for new construction, there are some things a newly built home can’t provide that an existing home can.

For example, existing homes have a lot of character and charm that’s difficult to reproduce. The quirks that come with an older home may make it feel more homey. And, existing homes usually have more developed landscaping and a well-established sense of community. So, it can feel more inviting than something that’s a blank slate, like new construction often is. Not to mention, if you go with new construction, you may have to wait for the home to finish being built based on where it is in the process. It all depends on what’s most important to you.

Bottom Line

Whether you choose a newly built or an existing home, you may be able to ease some of your concerns over maintenance with a home warranty. To weigh your options and go over what’s the top priority for you, talk to the professionals.

What’s Next for Home Prices and Mortgage Rates?

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.

If you’re thinking of making a move this year, there are two housing market factors that are probably on your mind: home prices and mortgage rates. You’re wondering what’s going to happen next. And if it’s worth it to move now, or better to wait it out.

The only thing you can really do is make the best decision you can based on the latest information available. So, here’s what experts are saying about both prices and rates.

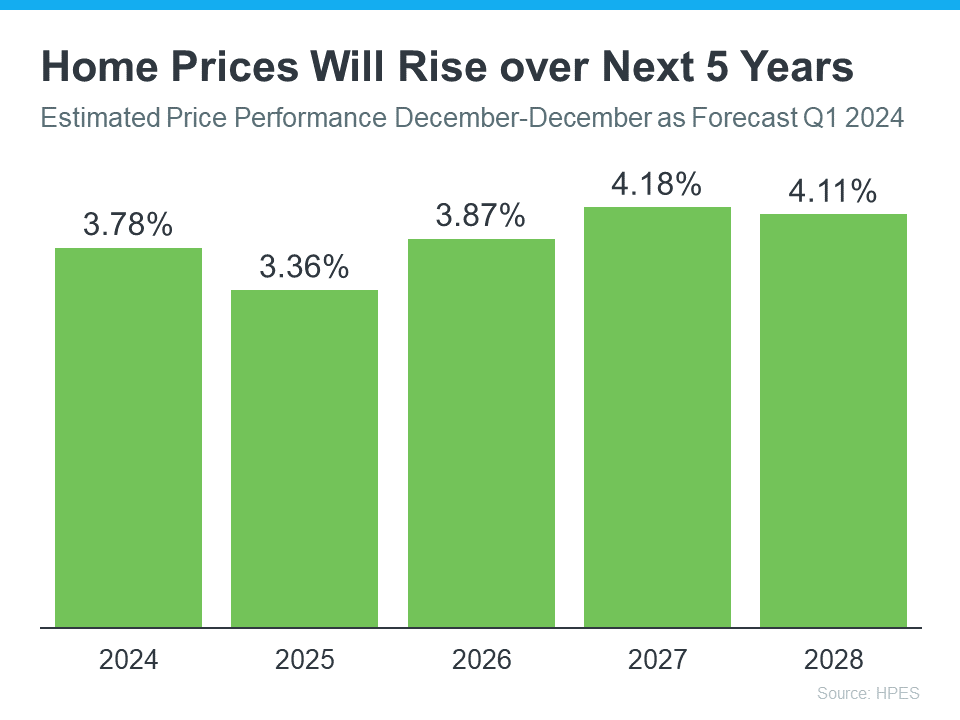

1. What’s Next for Home Prices?

One reliable place you can turn to for information on home price forecasts is the Home Price Expectations Survey from Fannie Mae – a survey of over one hundred economists, real estate experts, and investment and market strategists.

According to the most recent release, experts are projecting home prices will continue to rise at least through 2028 (see the graph below):

While the percent of appreciation varies year-to-year, this survey says we’ll see prices rise (not fall) for at least the next 5 years, and at a much more normal pace.

What does that mean for your move? If you buy now, your home will likely grow in value and you should gain equity in the years ahead. But, based on these forecasts, if you wait and prices continue to climb, the price of a home will only be higher later on.

2. When Will Mortgage Rates Come Down?

This is the million-dollar question in the industry. And there’s no easy way to answer it. That’s because there are a number of factors that are contributing to the volatile mortgage rate environment we’re in. Odeta Kushi, Deputy Chief Economist at First American, explains:

“Every month brings a new set of inflation and labor data that can influence the direction of mortgage rates. Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.”

What happens next will depend on where each of those factors goes from here. Experts are optimistic rates should still come down later this year, but acknowledge changing economic indicators will continue to have an impact. As a CNET article says:

“Though mortgage rates could still go down later in the year, housing market predictions change regularly in response to economic data, geopolitical events and more.”

So, if you’re ready, willing, and able to afford a home right now, partner with a trusted real estate advisor to weigh your options and decide what’s right for you.

Bottom Line

Let’s connect to make sure you have the latest information available on home prices and mortgage rate expectations. Together we’ll go over what the experts are saying so you can make an informed decision on your move.

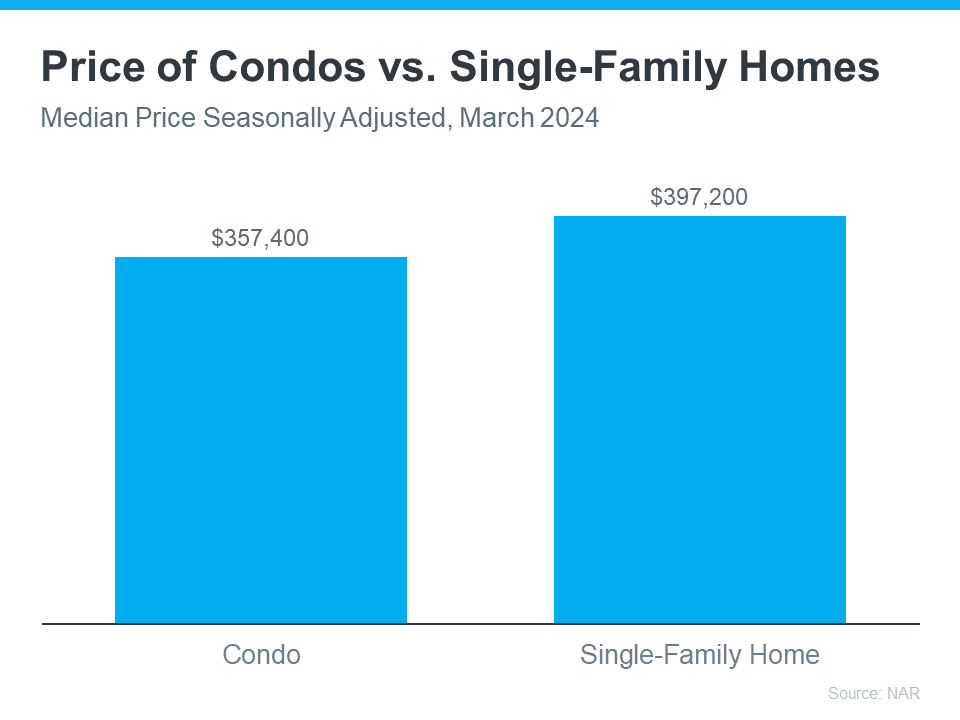

Why a Condo May Be a Great Option for Your First Home

Having a hard time finding a first home that’s right for you and your wallet? Well, here’s a tip – think about condominiums, or condos for short.

Having a hard time finding a first home that’s right for you and your wallet? Well, here’s a tip – think about condominiums, or condos for short.

They’re usually smaller than single-family homes, but that’s exactly why they can be easier on your budget. According to the latest data from the National Association of Realtors (NAR), condos are typically less expensive than single-family homes (see graph below):

So, if you’re comfortable with a smaller space and want to buy your first home this year, adding condos to your search might be easier on your wallet.

Besides giving you more options for your home search and maybe fitting your budget better, living in a condo has a bunch of other perks, too. According to Rocket Mortgage:

“From community living to walkable urban areas, condos are great options for first-time home buyers and people looking to enjoy homeownership without extensive upkeep.”

Let’s dive into a few of the draws of condos for first-time buyers from Bankrate:

- They require less maintenance. Condos are great if you want to own your place but don’t want to mow the lawn, shovel snow, or fix the roof. Your real estate agent can help explain any associated fees and details for the condos you’re interested in.

- They allow you to start building equity. When you buy a condo, you build equity and your net worth as you make your mortgage payments and as your condo’s value goes up over time.

- They often come with added amenities. Your condo might come with access to amenities like a pool, dog park, or parking. And the best part? You don’t have to take care of any of them.

- They provide you with a sense of community. Buying a condo means you’ll be living close to other people, which is nice if you enjoy having neighbors around and making friends. Many condo communities hold fun events like barbecues and parties during holidays for everyone to enjoy.

Remember, your first home doesn’t have to be the one you stay in forever. The important thing is to get your foot in the door as a homeowner so you can start to gain home equity. Later on, that equity can help you buy another place if you need something different.

Ultimately, owning and living in a condo is a lifestyle choice. And if it’s one that appeals to you, they could provide the added options you need in today’s market.

Bottom Line

It might be a good idea to think about condos in your home search. If you’re ready to see what’s out there, let’s get in touch today.

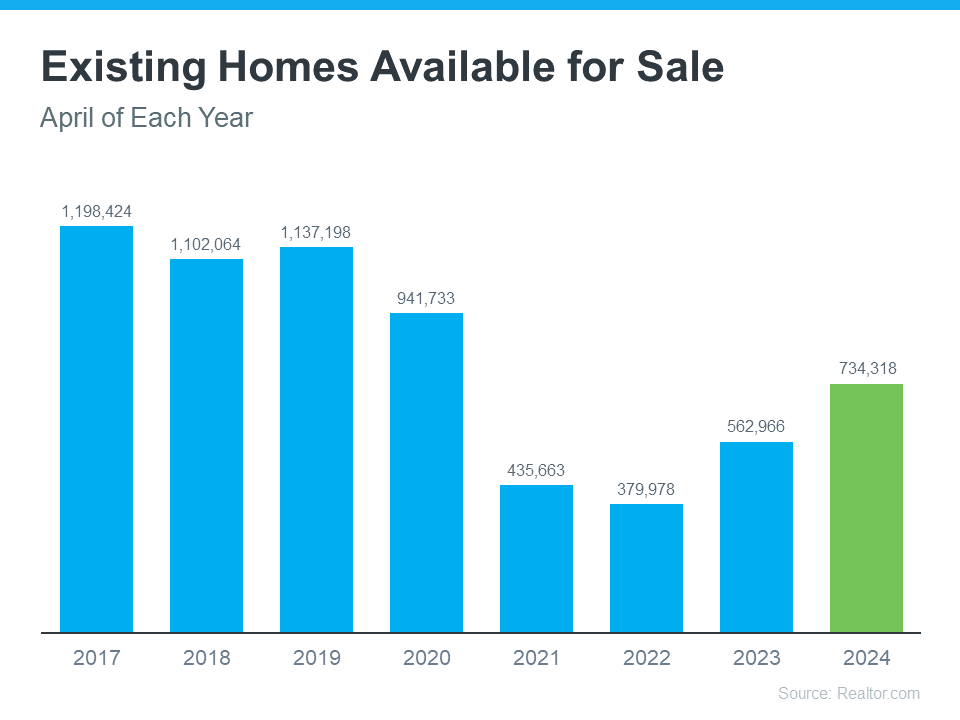

The Number of Homes for Sale Is Increasing

There’s no denying the last couple of years have been tough for anyone trying to buy a home because there haven’t been enough houses to go around. But things are starting to look up.

There are more homes up for grabs this year. The graph below uses the latest data from Realtor.com to show in April 2024 there were more homes for sale than there were over the last few years (2021-2023):

As Realtor.com explains:

“There were 30.4% more homes actively for sale on a typical day in April compared with the same time in 2023, marking the sixth consecutive month of annual inventory growth.”

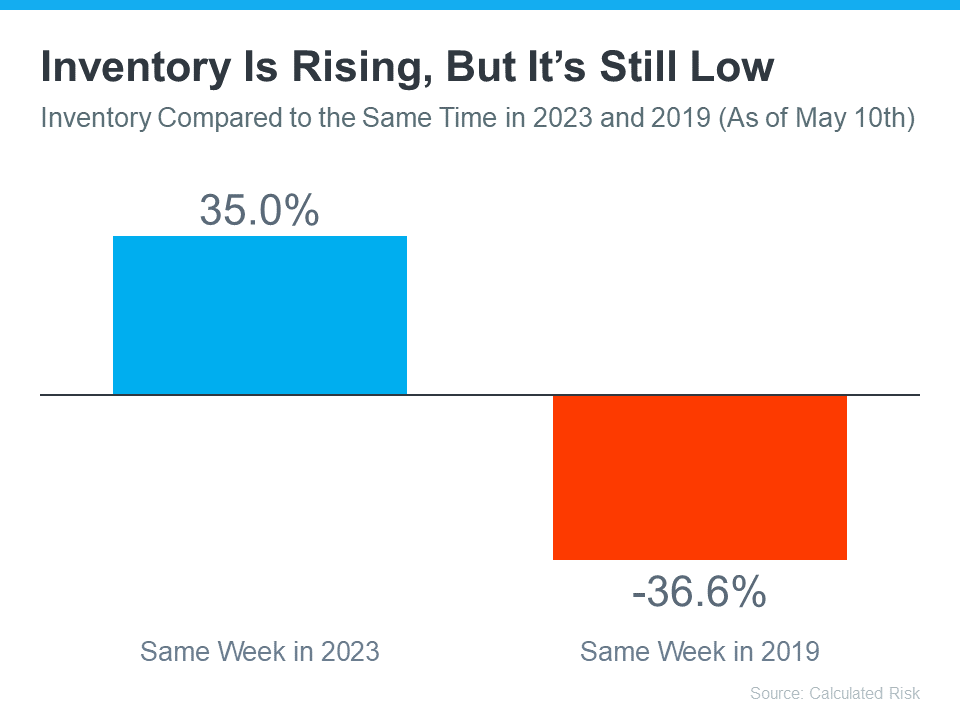

But does this growing inventory make house hunting easier? Yes and no.

Using the latest weekly data from Calculated Risk, the graph below shows, that even with the growth lately, there are still way fewer homes for sale than there were in the last normal year in the housing market:

What Does This Mean for You?

If you’ve been looking to buy but put your plans on hold because you just couldn’t find what you were searching for, you might see more options now than you did over the past few years – but don’t expect a huge selection.

To check out your growing options, it’s a good idea to work with a local real estate agent you trust. Real estate is all about location. And an agent can help you get the scoop on the homes available in the area you’re interested in. Bankrate explains:

“In today’s homebuying market, it’s more important than ever to find a real estate agent who really knows your local area — down to your specific neighborhood — and can help you successfully navigate its unique quirks.”

Bottom Line

Let’s team up so you have someone who can keep you in the loop on everything that might impact your move, like how many homes are up for sale right now.

Thinking of Selling? You Want an Agent with These Skills

Selling your house is a big decision. Your home is one of the biggest investments you’ve probably ever made, and it’s a place where you’ve created countless memories. That combo means there’s going to be a lot of emotions involved. You want someone who understands your perspective, knows what it feels like, and is an expert at helping homeowners just like you navigate the process of selling a home.

That’s where a good listing agent, also known as a seller’s agent, comes in. Here are just a few skills you’ll want your agent to have.

The Ability To Turn Something Complex into Something Simple

Some agents are going to use big, fancy real estate terms to try and impress you. But you shouldn’t have to know all the industry jargon in order to understand what they’re saying. If anything, it’s an agent’s job to keep it simple, so you don’t get overwhelmed or confused.

A great agent is going to be someone who is very good at explaining what’s happening in the housing market in a way that’s easy to understand. But they’ll take it one step further than that. They’ll explain what’s going on and, specifically, what that means for you. That way you’re always in the loop and it’s a lot easier to feel confident when you’re making a big decision. As Business Insider explains:

“Maybe you have a better rapport with one of the agents you’re considering, or you just feel like they’re easier to approach. You’re going to be working closely with this person, so it’s important to choose an agent you’re comfortable with.”

A Data-Based Approach on How To Price Your House

While it may be tempting to pick the agent who suggests the highest asking price for your house, that strategy may cost you. It’s easy to get caught up in the excitement when you see a bigger number, but overpricing your house can have consequences. It could mean your house will sit on the market longer because the higher price is actually turning away buyers.

Instead, partner with an agent who’s going to have an open conversation about how they recommend you should price your house. They won’t throw out a number just to win your listing. A great agent will back up their number with solid data, explain their pricing strategy, and make sure you’re both on the same page. As NerdWallet explains:

“An agent who recommends the highest price isn’t always the best choice. Choose an agent who backs up the recommendation with market knowledge.”

A Fair, but Objective Negotiator

The home-selling process can be emotional, especially if you’ve been in your house for a long time. But that sentimental tie can make it harder to be objective during negotiations. That’s where a trusted professional can really make a difference.

They’re skilled negotiators who know how to stay calm under pressure. You can count on them to handle the back-and-forth and have your best interests at heart throughout the process. Not to mention, they’ll be able to rely on their market expertise and what they’re seeing work in other transactions to offer the best advice possible. As Rocket Mortgage explains:

“Whether this is your first or third time selling a house, listing agents work to help make the home selling process smoother and less stressful. These real estate professionals know the ins and outs of the industry and can help you secure the best deal.”

Bottom Line

Whether you’re a first-time seller or you’ve been through this before, a great listing agent is the key to your success. Let’s connect so you have a skilled local expert by your side to guide you through every step of the process.