Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Long Will It Take To Sell My House?

You want your house to sell fast. And you may be wondering how long the whole process is going to take. One way to get your answer? Work with a local real estate agent.

They have the expertise to tell you how quickly homes are selling in your area and what’s impacting timelines for other sellers. That way you have realistic expectations and can work together to come up with a plan that’s based on today’s market.

Here’s a high-level overview of just one of the factors a great agent will walk you through – the supply of homes for sale and how that impacts your process.

The Growing Supply of Homes for Sale

Over the past few months, the number of homes for sale has increased. This is good news when you move because it means you’ll have more options as you search for your next home. But it also means buyers have more to choose from, so if your house doesn’t stand out – it may take a bit longer to sell.

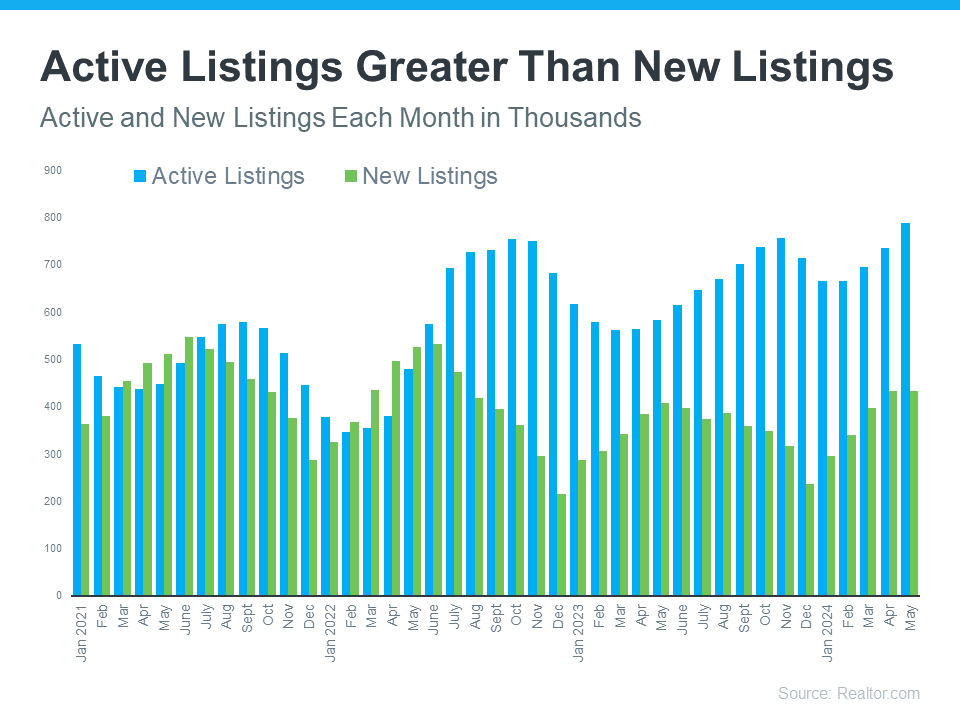

Available inventory is made up of new listings (homes that were just put up for sale) and active listings (homes that were already on the market but haven’t sold yet). And if you look at data from Realtor.com you can see a good portion of the recent growth is from active listings that are sticking around (see the blue bars in the graph below):

How It’s Impacting Listings Today

Think of the homes on the market like loaves of bread for sale in a bakery. When a fresh batch of bread is put out, everyone wants the newest and hottest one. But if a loaf sits there too long, it starts to get stale, and fewer people want to buy it.

The same goes for homes. New listings are the freshest and most sought-after. But if a home isn’t priced correctly, doesn’t show well, or it doesn’t have an effective sales or marketing strategy behind it, it can sit on the market and become less appealing to buyers over time.

An Agent Will Help Your House Stand Out and Sell Quickly

Timing is important to you. You want to get this done, fast. By leaning on a pro, they’ll make sure your listing is fresh and doesn’t stick around long enough to go stale. As the National Association of Realtors (NAR) explains:

“Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home.”

Your agent will factor the recent inventory growth into their plan and create a customized selling strategy for your house. The supply of homes for sale can vary a lot by area. So they’ll do things like share their valuable insights into what’s happening with supply in your market, help you price your home correctly, and create a marketing plan that gets your home noticed.

Don’t let your listing get stale—reach out to a real estate agent today to make sure your listing is fresh and appeals to buyers from the start. It makes a big difference.

Bottom Line

If you want your house to sell fast, you need to work with a pro. Let’s connect so you’ve got someone who understands the current market trends and how to build a strategy around those factors, so your house is set up to sell quickly.

Housing Market Forecast: What’s Ahead for the 2nd Half of 2024

As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home sales.

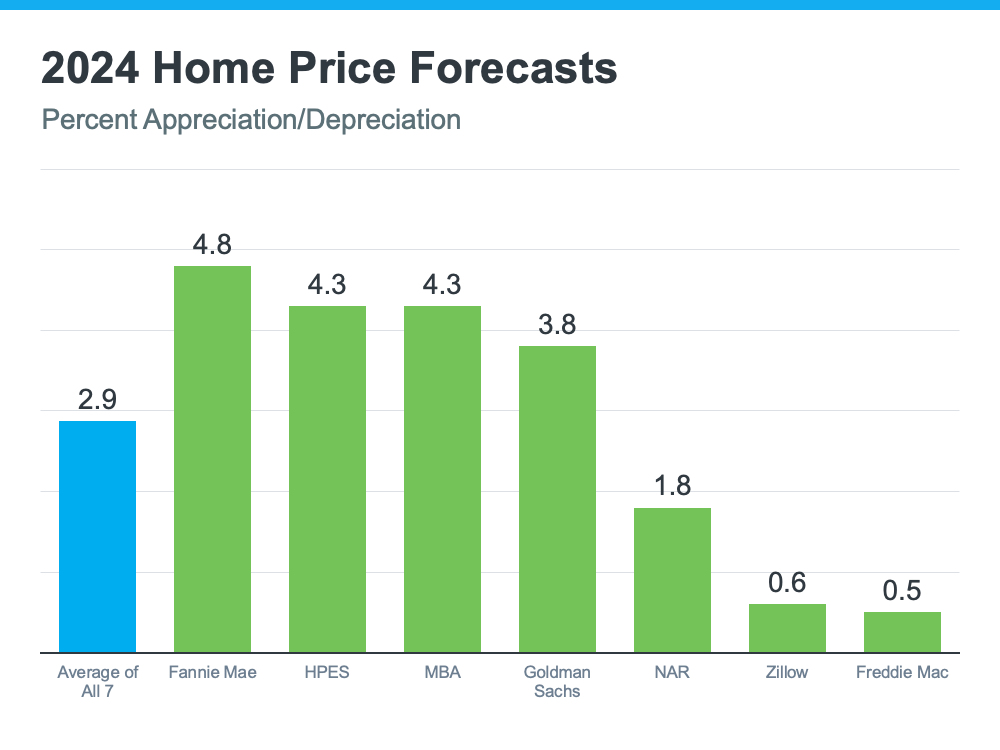

Home Prices Are Expected To Climb Moderately

Home prices are forecasted to rise at a more normal pace. The graph below shows the latest forecasts from seven of the most trusted sources in the industry:

The reason for continued appreciation? The supply of homes for sale. Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), explains:

“One thing that seems to be pretty solid is that home prices are going to continue to go up, and the reason is that we don’t have housing inventory.”

While inventory is up compared to the last couple of years, it’s still low overall. And because there still aren’t enough homes to go around, that’ll keep upward pressure on prices.

If you’re thinking of buying, the good news is you won’t have to deal with prices skyrocketing like they did during the pandemic. Just remember, prices aren’t expected to drop. They’ll continue climbing, just at a slower pace.

So, getting into the market sooner rather than later could still save you money in the long run. Plus, you can feel confident experts say your home will grow in value after you buy it.

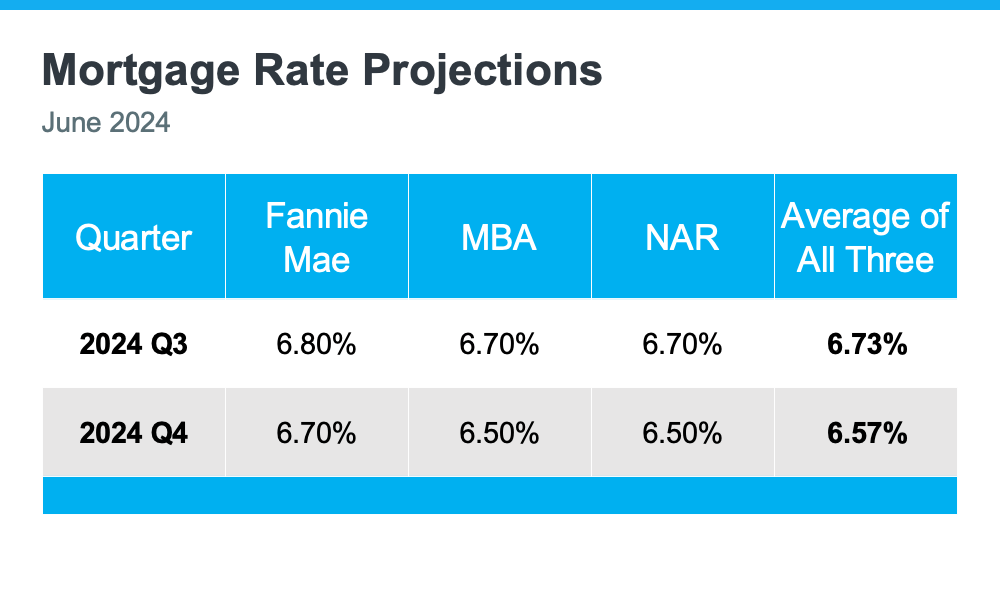

Mortgage Rates Are Forecast To Come Down Slightly

One of the best pieces of news for both buyers and sellers is that mortgage rates are expected to come down a bit, according to Fannie Mae, the Mortgage Bankers Association (MBA), and NAR (see chart below):

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

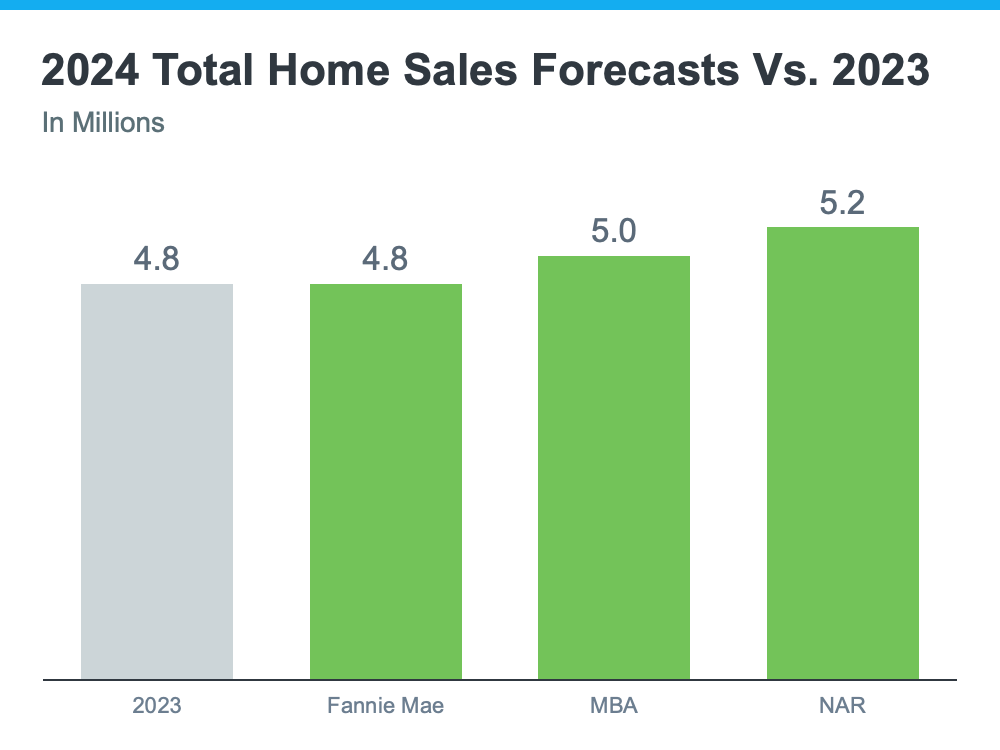

Home Sales Are Projected To Hold Steady

For 2024, the number of home sales will be about the same as last year and may even rise slightly. The graph below compares the 2024 home sales forecasts from Fannie Mae, MBA, and NAR to the 4.8 million homes that sold last year:

The average of the three forecasts is about 5 million sales in 2024 – a small increase from 2023. Lawrence Yun, Chief Economist at NAR, explains why:

“Job gains, steady mortgage rates and the release of inventory from pent-up home sellers will lead to more sales.”

With more inventory available and mortgage rates expected to go down, a few more homes are expected to be sold this year compared to last year. This means more people will be able to move. Let’s work together to make sure you’re one of them.

Bottom Line

If you have any questions or need help navigating the market, reach out.

The Downsides of Selling Your House Without an Agent

Considering selling your house without an agent? You should know there are some serious downsides to handling it on your own. You’ll be missing out on marketing tools that draw in more buyers, pricing and market expertise, essential negotiation skills, in-depth knowledge of the fine print in contracts, and so much more. Don’t take all of this responsibility on. Instead, DM me so you have someone with the knowledge and experience you’ll need on your side.

Why a Vacation Home Is the Ultimate Summer Upgrade

Summer is officially here and that means it’s the perfect time to start planning where you want to vacation and unwind this season. If you’re excited about getting away and having some fun in the sun, it might make sense to consider if owning your own vacation home is right for you.

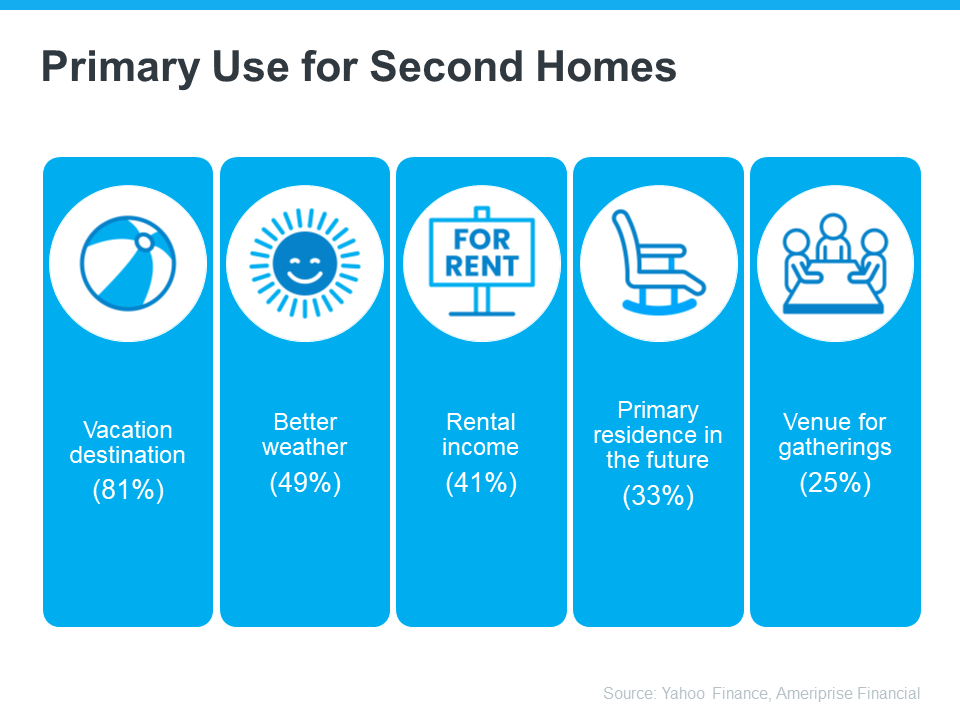

An Ameriprise Financial survey sheds light on why people buy a second, or vacation, home (see below):

- Vacation destination or a place to get away from the stresses of everyday life (81%) – Having a second home to use as a vacation spot can be a special place where you go to relax and take a break from your daily routines and stressors. It also means you won’t have to worry about finding somewhere to stay when you go there.

- Better weather (49%) – Buying in a place where there may be nicer weather can be a great escape, especially if it’s cold or rainy where you usually live. It lets you enjoy sunny days and warm temperatures, even when it’s not so nice back home.

- Rental income (41%) – You can rent it out to other people when you’re not using it, which can help you make some extra money.

- Primary residence in the future (33%) – You can eventually move into the home full-time during retirement. That means you can enjoy vacations there now and have a getaway ready for your future.

- Having a venue for gatherings with family and friends (25%) – It would be a special spot where you can have parties, regular family trips, and create fun memories.

Ways To Buy Your Vacation Home

And you don’t have to be wealthy to buy a vacation home. Bankrate shares two tips for how to make this dream more achievable for anyone who’s interested:

- Buy with loved ones or friends: If you’re okay with sharing the vacation home, you can go in on the purchase price together and pool your resources to make it more affordable.

- Put a savings plan in place: This will require patience and persistence but consider adding a vacation home savings plan to your budget and contributing to it monthly.

Finding Your Dream Spot with a Little Help from an Agent

If the idea of basking in the sun at your very own vacation home sounds appealing, you might want to start looking now. Summer’s when everyone’s trying to buy their slice of paradise, so it’s best to start early.

Your first move is to team up with a real estate agent. They know all the ins and outs of the area you want to be in, and which homes you should look at. Plus, they can give you the lowdown on everything you need to know about having a second home and how it can benefit you. The same article from Bankrate says:

“Buying real estate in a new area — or even one you’ve vacationed in for many years — requires expert guidance. That makes it a good idea to work with an experienced local lender who specializes in loans for vacation homes and a local real estate professional. Local lenders and Realtors will understand the required rules and specifics for the area you are buying, and a local Realtor will know what properties are available.”

Bottom Line

If the idea of owning your own vacation home appeals to you, let’s chat.

What You Need To Know About Today’s Down Payment Programs

There’s no denying it’s gotten more challenging to buy a home, especially with today’s mortgage rates and home price appreciation. And that may be one of the big reasons you’re eager to look into grants and assistance programs to see if there’s anything you qualify for that can help. But unfortunately, many homebuyers feel like they don’t know where to start.

A recent Bank of America Institute study asked prospective buyers where they lack confidence in the process and need more information. And this is what topped the list:

53% said they need help understanding homebuying grant programs.

So, here’s some information that can help you close that gap.

What Is Down Payment Assistance?

As the Mortgage Reports explains:

“Down payment assistance (DPA) programs offer loans and grants that can cover part or all of a home buyer’s down payment and closing costs. More than 2,000 of these programs are available nationwide. . . DPA programs vary by location, but many home buyers could be in line for thousands of dollars in down payment assistance if they qualify.”

And here’s some more good news. On top of all of these programs, you probably don’t need to save as much for your down payment as you think. Contrary to what you may have heard, typically you don’t have to put 20% down unless it’s specified by your loan type or lender. So, you likely don’t need to save as much upfront, and there are programs designed to make your down payment more achievable. Sounds like a win-win.

First-Time and Repeat Buyers Are Often Eligible

It’s also worth mentioning, that it’s not just first-time homebuyers that are eligible for many of these programs. That means whether you’re looking to buy your first house or your fifth, there could be an option for you. As Down Payment Resource notes:

“You don’t have to be a first-time buyer. Over 39% of all [homeownership] programs are for repeat homebuyers who have owned a home in the last 3 years.”

Additional Down Payment Resources That Can Help

Here are a few of the down payment assistance programs that are helping many buyers achieve their dream of homeownership, even now:

- Teacher Next Door is designed to help teachers, first responders, health providers, government employees, active-duty military personnel, and Veterans reach their down payment goals.

- Fannie Mae provides down payment assistance to eligible first-time homebuyers living in majority-Latino communities.

- Freddie Mac also has options designed specifically for homebuyers with modest credit scores and limited funds for a down payment.

- The 3By30 program lays out actionable strategies to add 3 million new Black homeowners by 2030. These programs offer valuable resources for potential buyers, making it easier to secure down payments and realize their dream of homeownership.

- For Native Americans, Down Payment Resource highlights 42 U.S. homebuyer assistance programs across 14 states that ease the path to homeownership by providing support with down payments and other associated costs.

If you want more information on any of these, the best place to start is by contacting a trusted real estate professional.

They’ll be able to share more details about what may be available, including any other programs designed to serve specific professions or communities. And even if you don’t qualify for these types of programs, they can help see if there are any other federal, state, and local options available you should look into.

Bottom Line

Affordability is still a challenge, so if you’re looking to buy, you’re going to want to make sure you’re taking advantage of any and all resources available.

The best way to find out what’s out there is to connect with a team of real estate professionals, including a trusted lender and a local agent.

Worried About Mortgage Rates? Control the Controllables

Chances are you’re hearing a lot about mortgage rates right now. You may even see some headlines talking about last week’s Federal Reserve (the Fed) meeting and what it means for rates. But the Fed doesn’t determine mortgage rates, even if the headlines make it sound like they do.

Chances are you’re hearing a lot about mortgage rates right now. You may even see some headlines talking about last week’s Federal Reserve (the Fed) meeting and what it means for rates. But the Fed doesn’t determine mortgage rates, even if the headlines make it sound like they do.

The truth is, mortgage rates are impacted by a lot of factors: geo-political uncertainty, inflation and the economy, and more. And trying to pin down when all those factors will line up enough for rates to come down is tricky.

That’s why it’s generally not worth it to try to time the market. There’s too much at play that you can’t control. The best thing you can do is control the controllables.

And when it comes to rates, here’s what you can influence to make your moving plans a reality.

Your Credit Score

Credit scores can play a big role in your mortgage rate. As an article from CNET explains:

“You can’t control the economic factors influencing interest rates. But you can get the best rate for your situation, and improving your credit score is the right place to start. Lenders look at your credit score to decide whether to approve you for a loan and at what interest rate. A higher credit score can help you secure a lower interest rate, maybe even better than the average.”

That’s why it’s even more important to maintain a good credit score right now. With rates where they are, you want to do what you can to get the best rate possible. If you want to focus on improving your score, your trusted loan officer can give you expert advice to help.

Your Loan Type

There are many types of loans, each offering different terms for qualified buyers. The Consumer Financial Protection Bureau (CFPB) says:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

When working with your team of real estate professionals, make sure you find out what’s available for your situation and which types of loans you may qualify for.

Your Loan Term

Another factor to consider is the term of your loan. Just like with loan types, you have options. Freddie Mac says:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Depending on your situation, the length of your loan can also change your mortgage rate.

Bottom Line

Remember, you can’t control what happens in the broader economy. But you can control the controllables.

Work with a trusted lender to go over the things you can do that’ll make a difference. By being strategic with these factors, you may be able to combat today’s higher rates and lock in the lowest one you can.

Do Elections Impact the Housing Market?

The 2024 Presidential election is just months away. As someone who’s thinking about potentially buying or selling a home, you’re probably curious about what effect, if any, elections have on the housing market.

It’s a great question because buying or selling a home is a major decision, and it’s natural to wonder how such a major event might impact your plans.

Historically, Presidential elections have only had a small, temporary impact on the housing market. Here’s the latest on exactly what’s happened to home sales, prices, and mortgage rates throughout those time periods.

Home Sales

During the month of November, in years when the Presidential election takes place, there’s typically a slight slowdown in home sales. As Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mostly because some people feel uncertain and hesitant about making big decisions during such a pivotal time. However, it’s important to know this slowdown is temporary. Historically, home sales bounce back in December and continue to rise the following year.

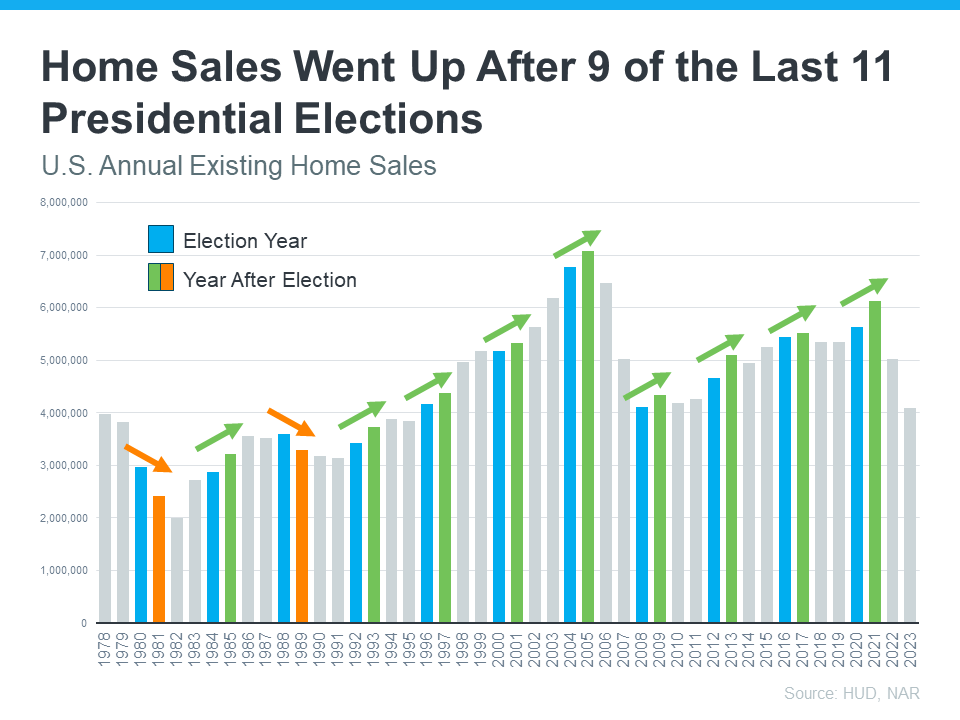

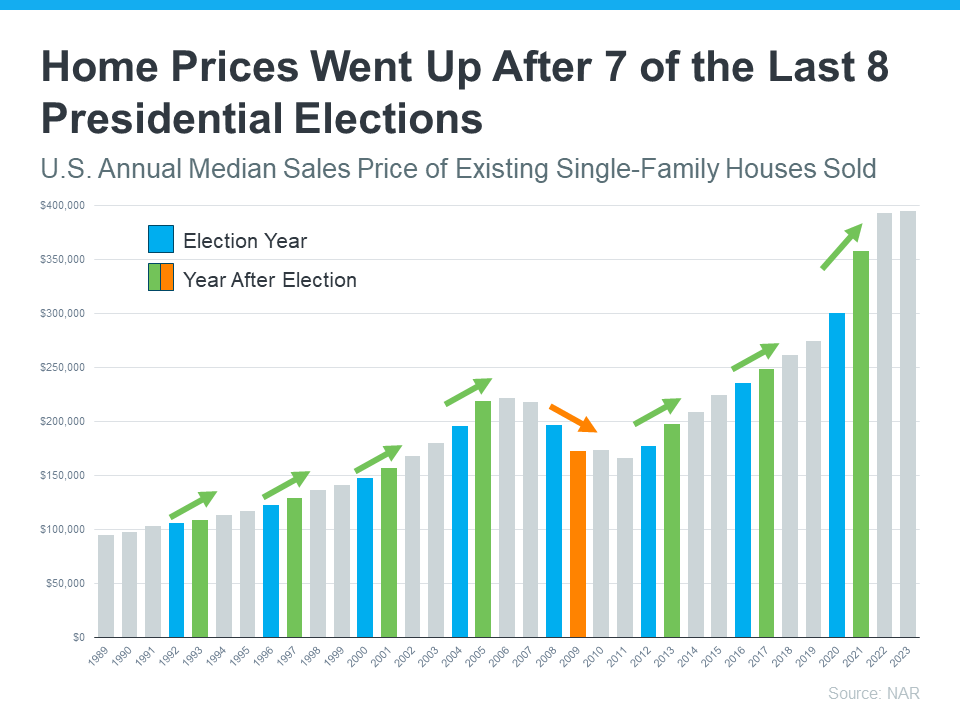

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after nine of the last 11 Presidential elections, home sales went up the next year (see graph below):

The graph shows annual home sales going back to 1978. Each year with a Presidential election is noted in blue. The year immediately after each election is green if existing home sales rose that year. The two orange bars represent the only years when home sales decreased after an election.

Home Prices

What about home prices? Do they drop during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist puts it:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices are pretty resilient. They generally rise year-over-year, regardless of elections. The latest data from NAR shows after seven of the last eight Presidential elections, home prices increased the following year (see graph below):

Just like the previous graph, this shows election years in blue. The only year when prices declined after an election is in orange. That was during the housing market crash, which was far from a typical year. Today’s market is different than it was back then.

All the green bars represent when prices rose the following year. So, if you’re worried about your home losing value because of an election, you can rest easy knowing prices rise after most Presidential elections.

Mortgage Rates

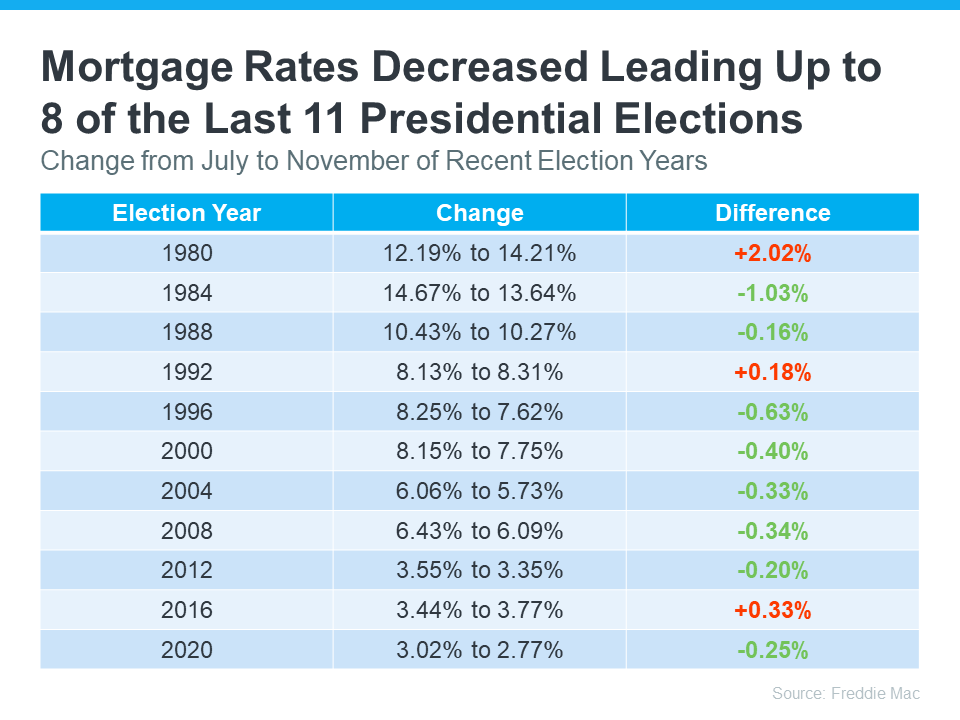

Mortgage rates are important because they affect how much your monthly payment will be when you buy a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in eight of them (see chart below):

Most forecasts expect mortgage rates to ease slightly throughout the remainder of the year. If they’re right, this year will follow the trend of declining rates leading up to most previous elections. And if you’re looking to buy a home in the coming months, this could be good news, as lower rates could mean a lower monthly payment.

What This Means for You

So, what’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually small and temporary. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. For help navigating the market, election year or not, let’s connect.

Real Estate Is Voted Best Investment Again

For twelve years straight, real estate has been voted the best long-term investment in an annual Gallup poll.

So, if you’re debating between renting or buying, remember, that it’s more than just a roof over your head. A home is an asset that usually grows in value over time – and that makes it a powerful investment.

Homebuilders Aren’t Overbuilding, They’re Catching Up

You may have heard that there are more brand-new homes available right now than the norm. Today, about one in three homes on the market are newly built. And if you’re wondering what that means for the housing market and for your own move, here’s what you need to know.

Why This Isn’t Like 2008

People remember what happened to the housing market back in 2008. And one of the factors that contributed to that crash was that there were too many homes for sale. While only part of the oversupply back then came from builders, the lasting impact is that some people still feel uneasy when they hear new home construction has ramped up.

Even though the supply of new homes has grown this year, the data shows there’s no need to worry. Builders aren’t overbuilding, they’re just catching up.

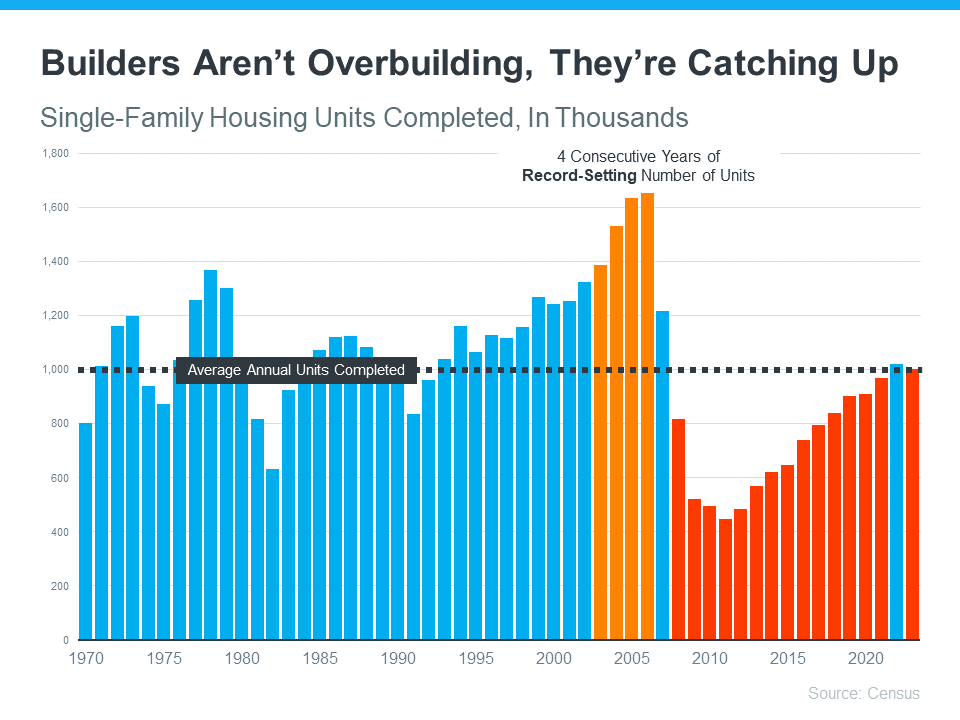

The graph below uses data from the Census to show the number of new houses built over the last 52 years. Following the crash in 2008, there was a long period of underbuilding (shown in red). And it wasn’t until recently that we finally met the long-term average for how many homes are built in a typical year.

This shows, that even with the increase in new builds we’ve seen lately, there won’t suddenly be an oversupply of homes for sale. There’s too much of a gap to make up after over a decade of underbuilding. And if you’re still worried builders are overdoing it, here’s something else that should be reassuring.

New Home Construction May Be at Its Peak for the Year

The latest data from the Census on housing starts (homes where builders just broke ground) and permits (homes where builders can start development soon) shows builders are slowing down their pace right now. Why is that?

They’re responding to still high mortgage rates and how those are impacting buyer demand. Basically, they’re pulling back appropriately in response to what’s happening in the market. As an article from HousingWire explains:

“Even with a massive housing shortage across the nation, homebuilders are completing their pipelines and not seeking as many permits to construct new single-family houses.”

Builders remember what happened when they overbuilt in the crash, and they’re looking to avoid a repeat of that. So, they’re being mindful and pulling back a bit.

You May Have More Options Now Versus Later

If you’re considering a newly built home, here’s how this impacts you. With builders seeking fewer permits and not breaking ground on as many new homes, we may be at the peak of new home construction for the year. This doesn’t mean new home construction is screeching to a stop – just that the pace is slowing down now, and that’ll impact what comes to market later this year. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Given the recent declines in housing starts, home completions will steadily show declines in about six months.”

So, if you’re ready and able to buy now, you may find you’ll have more newly built options to choose from now versus later on. This may be enough reason to kick off your search.

Just be sure to work with a local real estate agent you know and trust throughout the process. An agent will have valuable insight into builder reputations and other key factors specific to your market. And if there isn’t much new construction near you, they’ll be able to point you toward a nearby area where there is.

Bottom Line

While it’s true new home construction is a bigger segment of the market than the norm, that’s not a bad thing. Builders aren’t overbuilding, and they’re responding to market signals to avoid repeating the mistakes that were made in 2008.

If you want to buy now while new home options may be at their peak, let’s connect.

Home Prices Aren’t Declining, But Headlines Might Make You Think They Are

If you’ve seen the news lately about home sellers slashing prices, it’s a great example of how headlines do more to terrify than clarify. Here’s what’s really happening with prices.

The bottom line is home prices are higher than they were a year ago at this time, and they’re expected to keep rising, just at a slower pace.

But a recent article from Redfin notes,

“Price Drops Hit Highest Level in 18 Months As High Rates Dampen Buyer Demand.”

And that might make you think prices are declining.

Now, while it’s true the latest report from Realtor.com also shows 16.6% of homes on the market had price reductions in May, which is up from 12.7% last May, that doesn’t mean overall home prices are falling.

The key is knowing the difference between the asking price and the sold price.

Understanding Asking Price vs. Sold Price

In essence, the asking price, also known as a listing price, is the amount a seller hopes to get for their home when they list it. In reality, sellers can’t just put any price tag on their house and expect it to sell for top dollar. Today’s buyers are savvy customers, and when they aren’t willing to pay a premium for a home because their budgets are strained by higher mortgage rates, sellers need to adjust. And that’s what’s happening right now.

Based on market factors and what offers that seller receives, that asking price can change. If a seller isn’t getting much foot traffic, you may see them revise the price and make an adjustment to reignite interest in the home – and sometimes that’s because they’ve overpriced it from the start. That’s where price reductions come in, and when you see “price drops” in a headline, it sounds like declining home prices.

Mike Simonsen, CEO and Founder of Altos Research, says:

“Not only is the share of homes with price cuts elevated compared to one year ago, but more price cuts are happening each week than last year.”

On the other hand, the final sold price is the amount a buyer actually pays when the transaction is complete.

Here’s the most important thing to note: Actual sold prices are still rising, and they’re expected to continue to do so at least over the next 5 years.

What Does This Mean for Home Prices?

So, while there’s been an increase in price reductions recently, this doesn’t mean overall home values are declining. Instead, it’s a sign that demand is moderating. And, as a result, sellers are adjusting their expectations to align with today’s market reality.

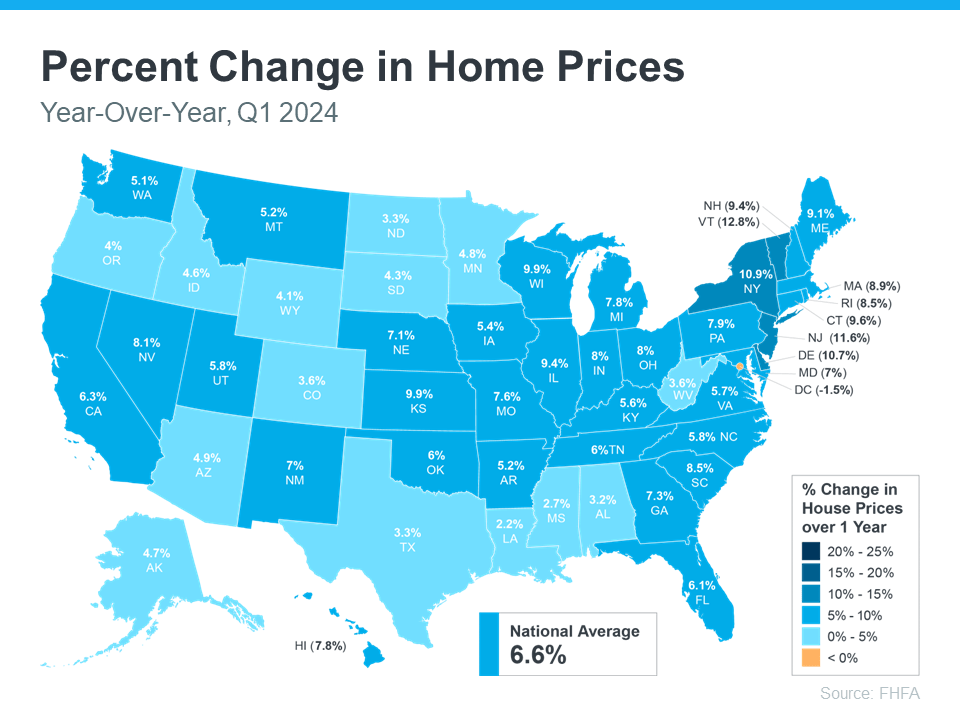

Even with more price reductions, home values are still growing on an annual basis, as they do nearly every year in the housing market. According to the Federal Housing Finance Agency (FHFA), home prices went up 6.6% over the last year (see below):

This map shows how prices rose just about everywhere in the country, indicating the market is not in decline.

So, while seller price reductions are often a leading indicator that prices may moderate in the months ahead, which experts have been saying for a while is expected to happen, they aren’t necessarily reason for alarm. The same article from Redfin also states:

“. . .those metrics suggest sale-price growth could soften in the coming months as persistently high mortgage rates turn off homebuyers. For now, the median-home sale price is up 4.3% year over year to another record high. . .”

And with inventory as tight as it is today, price moderation is much more likely in upcoming months than price declines.

Why This Is Good News for Buyers and Sellers

For buyers, more realistic asking prices mean a better chance of securing a home at a fair price. It also means you can enter the market with more confidence, knowing prices are stabilizing rather than continuing to skyrocket.

For sellers, understanding the need to adjust your asking price can lead to faster sales and fewer price negotiations. Setting a realistic price from the start can attract more serious buyers and lead to smoother transactions.

Bottom Line

While the uptick in price reductions might seem troubling, it’s not a cause for concern. It reflects a market adjusting to new conditions. Home prices are continuing to grow, just at a more moderate pace.